Annual Plan 2018–19

Overview

Section 7A of the Audit Act 1994 requires the Auditor-General to develop an annual plan and present it to Parliament, following consultation with Parliament’s Public Accounts and Estimates Committee.

As such it is a key accountability mechanism for the Auditor-General and his office. It sets out our work program and also gives Parliament, the public sector and the Victorian community the opportunity to assess our goals and understand our audit priorities.

Our three-year planning cycle for performance audits provides us with the opportunity to engage early with our stakeholders, and allows audited agencies to facilitate any necessary preparations for scheduled audits well in advance.

Our forward program also supports our strategic objectives. It is important that we explore our full mandate of economy, efficiency, effectiveness and compliance audits. We have sought to rebalance our performance program in 2018–19, with targeted reviews that focus on efficiency. We have tended to focus on outcome effectiveness in recent years, and in doing so, are not realising the opportunities that present themselves by focusing on cost-effectiveness.

We design our work program to be flexible and responsive. This allows us to direct our efforts towards doing the right audits at the right time, and using our resources to make a difference in the community. Throughout the process of developing this plan, we undertook extensive consultation with an expanded range of stakeholders at multiple stages, and considered all feedback received thoroughly as part of the finalisation of our audit program.

Transmittal letter

The Victorian Auditor-General’s Annual Plan 2018–19 was prepared pursuant to the requirements of section 7A of the Audit Act 1994, and tabled in the Victorian Parliament on 6 June 2018.

Acronyms and abbreviations

| AMAF | Asset Management Accountability Framework |

| AHV | Aboriginal Housing Victoria |

| CCTV | Closed-circuit television |

| CSV | Court Services Victoria |

| DEDJTR | Department of Economic Development, Jobs, Transport and Resources |

| DELWP | Department of Environment, Land, Water and Planning |

| DET | Department of Education and Training |

| DHHS | Department of Health and Human Services |

| DJR | Department of Justice and Regulation |

| DPC | Department of Premier and Cabinet |

| DSAPT | Disability Standards for Accessible Public Transport |

| DTF | Department of Treasury and Finance |

| EPA | Environment Protection Authority |

| EYM | Early Years Management |

| FGRS | Fair Go Rates System |

| HPFV | High-productivity freight vehicles |

| ICT | Information and communications technology |

| IV | Infrastructure Victoria |

| KCM | Kindergarten Cluster Management |

| LGPRF | Local Government Performance Reporting Framework |

| LGV | Local Government Victoria |

| MAV | Municipal Association of Victoria |

| MBS | Medical Benefits Scheme |

| MCH | Maternal and child health |

| MLP | Market-led proposals |

| MTM | Metro Trains Melbourne |

| NDFA | Natural Disaster Financial Assistance |

| NDRRA | Natural Disaster Relief and Recovery Arrangements |

| PAEC | Public Accounts and Estimates Committee |

| PVGF | Provincial Victoria Growth Fund |

| PTV | Public Transport Victoria |

| OPV | Office of Projects Victoria |

| RDV | Regional Development Victoria |

| RGG | Regional Growth Fund |

| RJIF | Regional Jobs and Infrastructure Fund |

| RoPP | Right of private practice |

| RTO | Registered training organisations |

| SCADA | Supervisory control and data acquisition |

| SORA | Sex Offenders Registration Act 2004 |

| TAFE | Technical and further education |

| TCP | Targeted care packages |

| TGA | Therapeutic Goods Administration |

| VAGO | Victorian Auditor-General's Office |

| VCAA | Victorian Curriculum and Assessment Authority |

| VET | Vocational education and training |

| VicTrack | Victorian Rail Track |

| VPDSF | Victorian Protective Data Security Framework |

| VPDSS | Victorian Protective Data Security Standards |

| VPSC | Victorian Public Sector Commission |

| VRGF | Victorian Responsible Gambling Foundation |

| VRQA | Victorian Registration and Qualifications Authority |

Draft performance audit work program 2018–2021

| Central Agencies and Whole of Government | Education | Environment | Health and Human Services | Infrastructure and Transport | Justice and Community Safety | Local Government | |

|---|---|---|---|---|---|---|---|

|

2018–19 |

CenITex: Meeting customer needs for ICT shared services Sharing information to address family violence Security of government buildings Fraud and corruption control —Part 2 |

School compliance with Victoria’s Child Safe Standards TAFE admission and enrolment processes |

Managing onsite domestic wastewater systems Recovering and reprocessing resources from waste Security of infrastructure control systems for water agencies Follow up of 2013–14 performance audit: Oversight and Accountability of Committees of Management |

Managing private medical practice in public hospitals Child and youth mental health Security of patients’ hospital data |

Security and privacy of surveillance technologies in public places Compliance with the Asset Management Accountability Framework Market-led proposals Melbourne Metro Tunnel project—Phase 1: Early works |

Police management of property and exhibits Managing registered sex offenders |

Delivering local government services Local government assets: Asset management and compliance Outcomes of investing in regional Victoria Reporting on local government performance |

|

2019–20 |

Service Victoria: Digital delivery of government services Sexual harassment in the Victorian public sector Fraud and corruption control —Part 3 |

Early Years Management in the Victorian kindergarten system The principal’s role in improving school performance Student literacy in digital technology |

Conserving Victoria’s threatened species Managing clearing of native vegetation Reducing bushfire risk Rehabilitating mine sites |

Efficiency and economy of Victoria’s public hospitals Clinical governance Targeted care packages Victoria’s homelessness response |

Improving safety on Victoria’s roads Managing railway assets across metropolitan Melbourne Passenger access to tram services Planning and managing Victorian infrastructure |

Ravenhall Prison: Rehabilitating and reintegrating prisoners —Part 1 Court data Reducing the harm caused by gambling |

Delivering local government services: Council libraries Supporting communities through developer and infrastructure contributions |

|

2020–21 |

Outcomes for Aboriginal Victorians: Community housing Cyber resilience in the Victorian public sector Fraud and corruption control —Part 4 |

Breaking the Link between disadvantage and student outcomes Enhanced maternal and child health services for vulnerable families Student attendance in Victorian schools |

Minimising stormwater impacts on Port Phillip Bay Effectiveness of water markets Victoria’s renewable energy targets |

Clinical trials in public hospitals Managing drug and alcohol rehabilitation services Managing Support and Safety Hubs Managing sexual and reproductive health |

Improving access to Victoria’s freight network: Bridge strengthening Melbourne Metro Tunnel —Phase 2: Main works Reforming Victoria’s taxi and ride-share services |

Managing and enforcing infringements Reducing the harm caused by alcohol and other drugs on Victorian roads Allocating electronic gaming machine entitlements |

Delivering local government services: Waste management services Implementing Plan Melbourne: 2017–50 Local government assets: Maintaining local roads |

Note: 2–3 follow-up audits yet to be added to each year of the program.

About our annual plan

The Victorian Auditor-General's Office provides independent assurance to Parliament and the Victorian community on the financial integrity and performance of the state.

Under the Audit Act 1994, we are required to prepare and table an annual plan before 30 June each year that describes our proposed work program for the coming financial year.

To provide assurance to the Parliament of Victoria and the Victorian community, the Victorian Auditor-General's Office conducts performance audits and financial audits. Our audits help the Parliament hold government to account and help the public sector to improve its performance.

A performance audit assesses whether agencies are meeting their aims effectively, using their resources economically and efficiently, and complying with relevant legislation. It provides assurance about activities that are performed well or represent better practice, and also identifies opportunities for further improvement.

A financial audit is an audit of the financial statements of an agency. It provides assurance that the financial statements present fairly the financial position, cashflows and results of operations for the year.

Both performance audits and financial audits integrate and support each other. Our financial audits are our early warning systems—intelligence obtained from our regular annual contact with agencies feeds into our performance audit program. In turn, our public reporting on the results of financial audits responds to and is shaped by our annual planning efforts.

The budgeted cost of delivering our proposed program is included in Appendix A.

Performance audits

Our performance audit work program operates on a three-year planning cycle. This provides Parliament, the public sector and the Victorian community with better foresight of our short- to medium-term goals and priorities.

Our annual planning process has three substantive components:

- understanding the environmental context

- deciding potential areas for audit focus

- communicating these plans to relevant stakeholders and incorporating their feedback where appropriate.

Understanding the environmental context

We consult with stakeholders and review publicly available information to inform our understanding of public sector programs and initiatives. We focus on risks, challenges and emerging issues which may influence the achievement of objectives. Our understanding of the environmental context assists us to identify potential areas of audit interest.

Deciding which areas to audit

To maximise our value and accountability to Parliament, the public sector and the community, we focus our limited resources on areas where we can have most impact.

In deciding the areas to audit, we use a rigorous approach to identify and prioritise potential performance audit topics. Our assessment process helps us to develop a work program that balances predictability and responsiveness.

Our forward program also supports our strategic objectives. It is important that we explore our full mandate of economy, efficiency, effectiveness and compliance audits. This will increase our relevance by delivering credible and authoritative reports about the things that matter and that will make a difference.

We have sought to rebalance our performance audit program in 2018–19, with targeted reviews that focus on efficiency. We have tended to focus on outcome effectiveness in recent years and, in doing so, are not realising the opportunities that present themselves by focusing on cost-effectiveness.

To address this, we have added several efficiency audits to the audit program in 2018–19, including:

- Efficiency and economy of Victoria's public hospitals (2019–20)

- Delivering local government services (2018–19, 2019–20 and 2020–21)

- TAFE admission and enrolment processes (2018–19).

We have also introduced a longer-term perspective to our audit program, by taking a thematic approach to a number of audit topic areas. This will allow us to analyse audit results through time to identify what works, assess the adequacy of early planning and work to set up initiatives for success, and use longitudinal, linked datasets to examine causal relationships. Examples of time‑series audits added to the 2018–19 work program include:

- Melbourne Metro Tunnel Project (2018–19 and 2020–21)

- Ravenhall Prison: Rehabilitating and reintegrating prisoners—Part 1 (2019–20).

It is important that we also sufficiently consider matters of good housekeeping and financial regularity that underpin service delivery. Audits in this year's plan that focus on these issues include:

- Fraud and corruption control (2018–19, 2019–20 and 2020–21)

- Police management of property and exhibits (2018–19)

- School compliance with Victoria's Child Safe Standards (2018–19).

Assessment steps

To ensure consistency in the selection process, we assess each potential audit topic against the following factors:

Degree of correlation between the topic idea and statewide/ sector specific issues, number of stakeholders affected, and extent of performance gaps between desired standards and actual results |

Consideration of the topic’s financial materiality, as well as its economic, social and environmental impact |

Relevance of the topic to Parliament, the current government, public sector agencies and community groups |

||

Our ability to provide unique insights and independent perspectives that add value to the audited agency |

Consideration of time-critical developments relevant to the proposed audit as well as our priorities |

Balance of economy, efficiency, effectiveness and compliance audits both across our performance audit mandate, as well as across the various portfolios/ sectors of government |

Consulting on our work program

Once we have considered, assessed and moderated each topic based on its merits, we consult with the Public Accounts and Estimates Committee (PAEC), departments and other proposed agencies. Our consultation is thorough and transparent, and provides the opportunity for considered feedback at multiple stages.

We consult in stages with comprehensive information:

- Stage 1—consultation on proposed 2018–19 and 2019–20 audits (topic synopses) and potential 2020–21 audits

- Stage 2—three-year proposed work program (audit specifications and topic synopses).

We thoroughly analyse all the feedback we receive to refine the focus of our audits, identify issues with proposed time lines and better understand the impact of current or proposed reforms on proposed audits. We refine and incorporate changes based on the feedback provided.

Follow-up audits

As part of our performance audit work program, we are also committed to conducting follow-up audits. Our follow-up audits aim to monitor agencies' progress in implementing actions from previous audits, as well as verifying that actions taken by agencies have effectively addressed our recommendations.

To select audits to follow-up, we undertake a comprehensive follow-up survey to assess agencies' actions on recommendations over a three-year period—for example, the 2018–19 survey will focus on outstanding recommendations for audits tabled in 2014–15, 2015–16 and 2016–17.

The issues identified in the initial audit, as well as the risk and materiality of the subject matter also inform the follow-up audit topics we select.

Finalising our work program

The table inside the front cover sets out the performance audits we intend to undertake over the next three years. This forecast provides us with more opportunities for early engagement with our stakeholders and allows audited agencies to prepare for scheduled audits well in advance.

We conduct our performance audits in accordance with relevant standards issued by the Australian Auditing and Assurance Standards Board. These standards cover planning, conduct, evidence, communication, reporting and other elements of performance audits. Additional information about how we deliver our performance audits can be found in Appendix B.

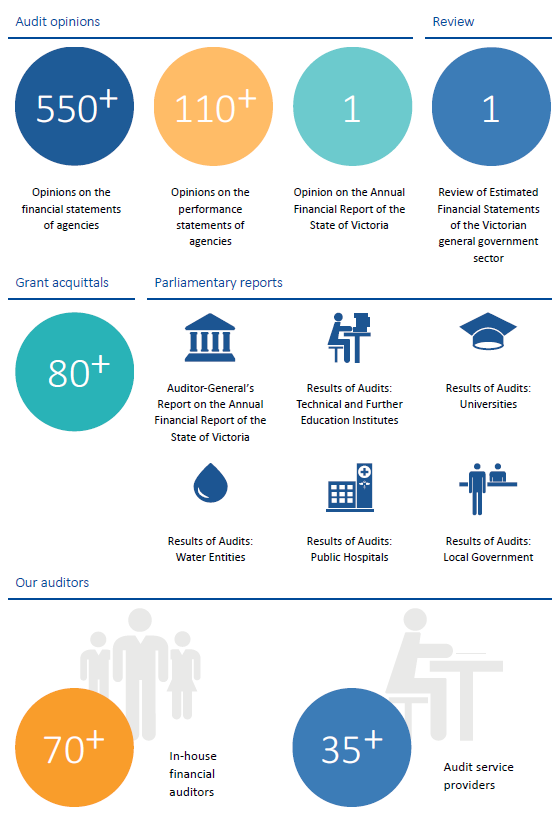

Financial audits

Our financial audit program delivers a range of assurance services for public sector agencies. These include:

- audit opinions on financial reports and performance statements of public sector agencies

- an opinion on the Annual Financial Report of the State of Victoria

- a review report on the estimated financial statements of the State of Victoria

- five reports to Parliament on the results of financial audits

- a report to Parliament on the outcome and findings of our audit of the Annual Financial Report of the State of Victoria.

Public Accounts and Estimates Committee

The Audit Act 1994 requires us to seek comments on our draft annual plan from PAEC. We value PAEC's input and also seek its suggestions on potential areas of public sector activity that may benefit from audit scrutiny.

PAEC has provided useful input into our annual plan, including proposed audits for our future audit program and suggestions to improve the scope of particular upcoming audits.

Our legislation also requires us to publish in the annual plan any changes to the draft plan suggested by PAEC that the Auditor-General does not adopt. We are pleased to report that PAEC had no further suggestions in this planning cycle.

Performance audit work program

This section sets out our proposed performance audit specifications for the next three years. In 2018–19, we plan to deliver 22 performance audits along with one to two follow-up audits.

For each audit listed, we outline the audit specification, which includes our objective for the audit, the issues we intend to examine, and the agencies we expect to include.

Central Agencies and Whole of Government

CenITex: Meeting customer needs for ICT shared services

2018–19

Objective To determine whether CenITex is delivering services that meet customers' expectations and the requirements of its service level agreements.

Issues CenITex provides information and communications technology (ICT) shared services for six of the seven Victorian Government departments and their associated portfolio agencies. CenITex also provides services for the Environment Protection Authority (EPA), Public Transport Victoria (PTV), Taxi Services Commission, VicForests and the Victorian Ombudsman. It is part of the portfolio of the Department of Treasury and Finance (DTF), providing ICT services to support about 34 000 Victorian public servants.

Many aspects of government ICT, including data security and adoption of new technologies, rely on CenITex's performance. CenITex's performance also impacts the cost of delivering government services that use the systems that CenITex manages.

CenITex uses a performance management framework to manage and report its performance and publishes key performance data on its website.

This audit will assess CenITex's performance against the framework, including assessing the framework itself, and whether customers are receiving reliable services, and explore how CenITex and its customers gauge the competitiveness of its services, both now and in the future.

Proposed agencies CenITex and DTF.

Sharing information to address family violence

2018–19

Objective To determine whether agencies have established arrangements to share information about family violence and whether these arrangements enable timely interventions that keep victims safe.

Issues Family violence is a serious and prevalent issue—the Australian Bureau of Statistics reports that one in four women in Australia have experienced at least one incident of violence by a male intimate partner.

In March 2016, the Royal Commission into Family Violence released its report, making 227 recommendations and emphasising the importance of coordination and collaboration between agencies to effectively address family violence.

In November 2016, the government released Ending Family Violence: Victoria's Plan for Change, its 10-year plan in response to the Royal Commission's recommendations. In the plan, the government commits to supporting departments and agencies to build their capability in data analytics and improve the way they collect and share information. The Royal Commission recognised information sharing as a critical aspect of effectively identifying and managing family violence cases.

The audit will focus on agencies' progress in implementing the data sharing and coordination aspects of the government's plan to end family violence.

Proposed agencies Department of Premier and Cabinet (DPC), Department of Health and Human Services (DHHS), Department of Justice and Regulation (DJR), Court Services Victoria, Victoria Police, Anglicare Victoria and the Victorian Aboriginal Childcare Agency.

Security of government buildings

2018–19

Objective To determine whether Victorian Government office accommodation is sufficiently secure to prevent unauthorised access and other criminal or anti‑social behaviour that may threaten the safety of staff, visitors and members of the public.

Issues The Victorian Government owns and occupies a significant amount of office space across the state. Public sector agencies that use these premises need to apply active and passive security, and other safety measures to respond to a range of threats. These threats can be to personal safety, the security of government property and information, or the structural integrity of the premises.

Unauthorised access to government buildings could potentially cause significant disruption to public sector activities. Therefore, it is critical that:

- DTF—as the agency responsible for coordinating government office accommodation across metropolitan and regional areas—help departments and agencies to mitigate security risks by providing comprehensive and up‑to-date guidance and assessments based on the Commonwealth Protective Security Policy Framework

- departments and agencies apply DTF's guidance to meet appropriate levels of security.

This audit will explore whether existing guidance for designing and applying security measures within government buildings reflects effective, contemporary methods, and the extent to which agencies are applying these measures to protect buildings from unauthorised access and other criminal or anti-social behaviour.

Proposed agencies DTF, DJR and DHHS.

Fraud and corruption control—Part 2

2018–19

Objective To determine whether local councils' fraud and corruption controls are well designed and operating as intended.

Issues Fraud is dishonest activity involving deception that causes actual or potential financial loss by an entity or others. Corruption is dishonest activity in which an employee of an entity acts contrary to its interests, abusing his or her position of trust to achieve personal gain or advantage.

Investigations by the Independent Broad-based Anti-corruption Commission, together with various performance audits, have found that agencies have not consistently applied the integrity systems intended to control fraud risks, and that these systems require regular testing.

Our 2012 audit report Fraud Prevention Strategies in Local Government concluded that the five councils we examined had not effectively managed their exposure to fraud risk, as none had developed a strategic and coordinated approach to controlling fraud.

This audit will examine whether councils have well-designed fraud and corruption controls, and the extent to which these controls are operating as intended. This audit is part of an annual series of fraud and corruption audits that will each focus on different issues and agencies.

Proposed agencies Department of Environment, Land, Water and Planning (DELWP) and a selection of local councils.

Service Victoria: Digital delivery of government services

2019–20

Objective To determine whether use of digital and mobile technologies is cost‑effectively improving service delivery to Victorians.

Issues The Victorian Government is working to make digital technology the preferred method for providing government services. One of the actions outlined in the Information Technology Strategy for the Victorian Government 2016–2020 is the development of a digital distribution channel for simple, high‑volume government transactions.

To do this, DPC, through Service Victoria, is developing better digital channels and mobile services to replace the hundreds of phone hotlines and different websites currently in use, which often make it difficult for the public to access government services, as well as being costly for taxpayers.

Customer experience is a key aspect of realising the intended benefits of digital service delivery. In addition, effective cyber security contributes significantly to public confidence in these services.

This audit will assess whether responsible agencies are cost-effectively delivering services digitally and have implemented the relevant recommendations from our 2015 audit reports Delivering Services to Citizens and Consumers via Devices of Personal Choice (Phase 1 and Phase 2).

Proposed agencies Service Victoria and DPC.

Sexual harassment in the Victorian public sector

2019–20

Objective To assess whether the Victorian public sector is providing work places that are free from sexual harassment.

Issues A 2012 survey by the Australian Human Rights Commission found that one in five people over the age of 15 (21 per cent) had experienced sexual harassment in the workplace in the past five years. Sexual harassment at work can have wide-ranging impacts, such as psychological harm, social isolation, health issues and economic loss.

For the public sector, the Public Administration Act 2004 enshrines respect as a core value—it states that public officials should demonstrate respect for colleagues, other public officials and community members by ensuring freedom from discrimination, harassment and bullying. Every employer, regardless of size, must take reasonable steps to prevent sexual harassment in the workplace to uphold this value and avoid liability.

In the public sector, some workplaces may have increased risk of sexual harassment because of cultural or historical gender balances. Reporting and recording of sexual harassment complaints can be complicated, as the behaviour is often accompanied by other forms of victimisation. Addressing sexual harassment may involve multiple agencies depending on how the victim describes the event, which agency receives the complaint, and what legislation is then applied. Since 2016, the Victorian Public Sector Commission's (VPSC) People Matter Survey has included questions about sexual harassment to help improve monitoring and understanding of patterns of harassment in the public sector.

This audit will use data to investigate the prevalence of sexual harassment in the Victorian public sector and assess the effectiveness of agencies' actions to address it.

Proposed agencies DPC, DTF, DHHS, DELWP, Department of Economic Development, Jobs, Transport and Resources (DEDJTR), Department of Education and Training (DET), DJR, Victoria Police and WorkSafe Victoria.

Fraud and corruption control—Part 3

2019–20

Objective To determine whether agencies' fraud and corruption controls are well designed and operating as intended.

Issues Fraud is dishonest activity involving deception that causes actual or potential financial loss by an entity or others. Corruption is dishonest activity in which an employee of an entity acts contrary to its interests, abusing his or her position of trust to achieve personal gain or advantage.

Investigations by the Independent Broad-based Anti-corruption Commission, together with various performance audits, have found that agencies have not consistently applied the integrity systems intended to control fraud risks, and that these systems require regular testing.

Our 2012 audit report Fraud Prevention Strategies in Local Government concluded that the five councils we examined had not effectively managed their exposure to fraud risk, as none had developed a strategic and coordinated approach to controlling fraud.

This audit will examine whether agencies have well-designed fraud and corruption controls, and the extent to which these controls are operating as intended. This audit is part of an annual series of fraud and corruption audits that will each focus on different issues and agencies.

Proposed agencies A selection of government agencies.

Outcomes for Aboriginal Victorians: Community housing

2020–21

Objective To assess whether the ownership transfer of public housing assets to Aboriginal Housing Victoria (AHV) is supporting improved housing access, stability and uptake of support services for Aboriginal Victorians.

Issues The Aboriginal population experiences poorer outcomes than the general population on multiple indicators. Aboriginal people are seven times more likely to be the subject of a child protection assessment and are incarcerated at 11 times the rate of non-Aboriginal people. In total, 16.4 per cent of the Aboriginal population is unemployed compared with 6.3 per cent for the general population. Research indicates that for Aboriginal people, access to stable housing can be a significant barrier to positive health, wellbeing and employment outcomes.

In early 2017, the Victorian Government's housing strategy Homes for Victorians committed to transferring management of 4 000 public housing assets to the community housing sector. This follows the government's 2016 announcement that it would transfer ownership of 1 448 public housing assets to AHV, valued at approximately $500 million.

Transferring ownership of these properties is a key part of the government's commitment to self-determination for Aboriginal Victorians. It will empower AHV to plan for, maintain and develop a property portfolio that is financially sustainable and improves stability of housing for Aboriginal Victorians. As a consequence, this should improve referrals to support services and ultimately help to improve the health and wellbeing of residents, as well as helping them secure employment.

This audit will assess the extent to which the transfer of ownership of assets to AHV has improved stability of housing for residents, improved referrals to relevant support services, and contributed to positive outcomes.

Proposed agencies DHHS, DTF, DPC and AHV.

Cyber resilience in the Victorian public sector

2020–21

Objective To determine whether departments and agencies can adequately prevent, respond to and recover from cyber security attacks.

Issues The Victorian Government released its cyber security strategy in 2017. The strategy's purpose is to develop and implement cyber security capabilities to:

- protect sensitive data against loss, malicious alteration and unauthorised use

- ensure the resilience of government services, systems and infrastructure to cyber threats

- ensure the continuity of government during and after serious cyber incidents

- protect and secure new digital services for citizens

- coordinate Victoria's response to threats against infrastructure

- ensure the security and viability of the Victorian Government's core infrastructure.

In addition, the Victorian Protective Data Security Framework (VPDSF) and Victorian Protective Data Security Standards (VPDSS) provide direction for Victorian public sector agencies on their data security obligations, which includes cyber breaches.

Our previous audit reports have found that agencies' inadequate ICT security controls and immature operational processes may expose them to cyber attacks. We found that agencies had immature disaster recovery procedures and a low level of awareness of how their ICT systems would likely perform if subjected to a cyber attack. Further, agencies needed to significantly improve their adherence to the Australian Signals Directorate's Top 4 strategies to mitigate cyber intrusion.

This audit will assess whether the government's cyber security strategy and its implementation of the VPDSF and VPDSS have effectively improved government's cyber resilience.

Proposed agencies DPC, the Office of the Victorian Information Commissioner, CenITex, DTF, DHHS, DET, DELWP, DJR and DEDJTR.

Fraud and corruption control—Part 4

2020–21

Objective To determine whether agencies' fraud and corruption controls are well designed and operating as intended.

Issues Fraud is dishonest activity involving deception that causes actual or potential financial loss by an entity or others. Corruption is dishonest activity in which an employee of an entity acts contrary to its interests, abusing his or her position of trust to achieve personal gain or advantage.

Investigations by the Independent Broad-based Anti-corruption Commission, together with various performance audits, have found that agencies have not consistently applied the integrity systems intended to control fraud risks, and that these systems require regular testing.

Our 2012 audit report Fraud Prevention Strategies in Local Government concluded that the five councils we examined had not effectively managed their exposure to fraud risk, as none had developed a strategic and coordinated approach to controlling fraud.

This audit will examine whether agencies have well-designed fraud and corruption controls, and the extent to which these controls are operating as intended. This audit is part of an annual series of fraud and corruption audits that will each focus on different issues and agencies.

Proposed agencies A selection of government agencies.

Education

School compliance with Victoria's Child Safe Standards

2018–19

Objective To determine whether the systems and supports that oversee Victoria's Child Safe Standards assure school compliance.

Issues Schools have a duty of care for over 932 000 students and are responsible for providing a safe learning environment. Victoria's more than 2 228 government and non-government schools are required to protect their students from child abuse.

In 2016, the government introduced compulsory minimum Child Safe Standards that apply to all organisations that provide services for children. The standards aim to drive cultural change in public sector agencies so that protecting children from abuse is embedded in everyday thinking and practice.

A 2016 ministerial order imposes obligations on schools which aim to ensure schools implement and satisfy the Child Safe Standards. It also confirmed that the Victorian Registration and Qualifications Authority (VRQA) has some responsibility for monitoring and enforcing schools' compliance with the standards.

This audit will examine oversight and support activities relating to schools' compliance with the Child Safe Standards.

Proposed agencies Department of Education and Training (DET), VRQA and a selection of schools.

TAFE admission and enrolment processes

2018–19

Objective To determine the efficiency of admission and enrolment processes at technical and further education (TAFE) institutes.

Issues Victoria's vocational education and training (VET) system delivers workplace-specific skills to help improve employability. Victoria has over 1 000 registered training organisations (RTO) that offer thousands of VET courses, including dual-sector universities, TAFE institutes and private providers.

Since 2010, TAFEs have experienced considerable reform, including reductions in funding and adjusting to operating in a competitive VET sector. In 2017, the government released its reform to the Victorian training system, Skills First. Skills First aims to make vocational training more accessible to those without post-school qualifications, or those seeking higher-level qualifications than they already hold. Through the Skills First model, DET contracts RTOs to deliver government-subsidised training to eligible students.

A key component of a TAFE's economic success is its ability to progress inquiries from prospective students into admissions and enrolments.

This audit will examine whether TAFEs have processes to ensure only eligible students are enrolled, that their information systems are adequate to meet contractual requirements for admissions and enrolments and that they achieve efficiencies in these processes.

Proposed agencies DET, Box Hill Institute of TAFE, Swinburne University, Melbourne Polytechnic, William Angliss Institute and SuniTAFE.

Early Years Management in the Victorian kindergarten system

2019–20

Objective To determine whether Victoria's Early Years Management (EYM) framework has increased the sustainability and responsiveness of kindergarten services.

Issues Kindergarten and early-childhood development are important for helping to realise children's potential early in life.

From 2003, Victoria's community-based kindergartens were managed through the Kindergarten Cluster Management (KCM) model. Under this model, local councils, community-based organisations, or federated/amalgamated kindergarten organisations could be KCM organisations, managing multiple kindergarten services. By 2015, over 80 per cent of KCM organisations also delivered other early years services, such as long day care, occasional childcare and playgroups. A number of cluster-managed integrated learning centres and services provided in partnership with schools had also formed.

In 2016, service providers began transitioning to the EYM policy framework. The aims of the EYM framework reflect the expanded role of EYMs by better integrating services and improving their sustainability.

DET has overarching responsibility for EYM-funded services. This includes supporting, monitoring and evaluating EYM organisations' performance.

This audit will examine DET's oversight of EYM services and whether EYM organisations are meeting the new performance requirements.

Proposed agencies DET, Wyndham City Council, Hume City Council, Whitehorse City Council, Greater Shepparton City Council, Macedon Ranges Shire Council, Goodstart Early Learning and The Young Men’s Christian Association of Ballarat.

The principal's role in improving school performance

2019–20

Objective To determine whether DET's initiatives to develop and support school principals are contributing to improvements in school performance.

Issues A key focus of the government's Education State agenda is strong leadership in every school. School principals are expected to lead improvements in teaching quality and performance. They also manage a combined expenditure of around $12.9 billion in school budgets and teaching salaries, as well as significant infrastructure and other assets.

The role of the principal is complex and multifaceted, with three primary responsibilities—delivery of a comprehensive curriculum, governance of a school council, and management of the school's financial and human resources. DET has a range of initiatives aimed at cultivating a pipeline of potential leaders to perform these complex roles.

DET employs school principals and oversees their performance. In 2017, DET aligned its government schools' performance and development model for principals with the Australian Professional Standard for Principals. It also introduced online performance and development assessments to help it identify systemic issues and principals' developmental needs.

This audit will examine DET's work to nurture and prepare a pipeline of leaders to occupy the principal role, and how its support and oversight is assisting principals to improve school performance.

Proposed agencies DET and a selection of schools.

Student literacy in digital technology

2019–20

Objective To determine whether students are developing literacy in digital technology and design to meet future skill requirements.

Issues The employment market is increasingly volatile—technological change, automation leading to redundancy, and digitisation and globalisation of markets are having a growing influence on industries and jobs. In 2016, the Foundation for Young Australians reported that, based on current trends, individuals will have an average of 17 different jobs across five distinct industries in their working life.

The government has recognised the need for students to be better equipped to deal with our changing world, and the Victorian Curriculum and Assessment Authority (VCAA) rolled out a new curriculum in 2017. It established two new curriculum areas in technologies, both aimed at enabling students to become confident and creative developing digital solutions. These new areas are:

- digital technologies—providing students with practical opportunities to learn how to use computational, design and systems thinking to transform data into digital solutions

- design and technologies—encouraging students to consider the economic, environmental and social impacts of technological change, and how technologies may contribute to a sustainable future.

This audit will focus on how well the Victorian curriculum, and its implementation, is supporting students to develop digital literacy.

Proposed agencies DET, VCAA and a selection of schools.

Breaking the Link between disadvantage and student outcomes

2020–21

Objective To determine if students at risk of poor learning outcomes are supported to reach their potential and stay in education.

Issues In Victoria, there is a persistent gap in educational outcomes for students from disadvantaged backgrounds at all stages of their education. Breaking the Link is a key initiative in the government's broader Education State reforms. The initiative aims to reduce the impact of disadvantage.

Breaking the Link provides increased equity funding for schools with students who may face more barriers to success than their peers. The increased funding enables schools to invest in additional resources and expertise to support disadvantaged students. It also includes the following initiatives:

- LOOKOUT Education Support Centres—education experts and support staff in regional offices to support children and young people in out-of-home care with any education challenges they may face

- Navigator program—a case management service to support people aged 12–17 years to re-engage with education and training

- Marrung: Aboriginal Education Plan 2016–2026—a strategy to ensure that all Aboriginal Victorians achieve their learning aspirations and realise the full benefits of the Education State reforms.

This audit will examine whether these initiatives are:

- reducing the number of school leavers during years 9–12

- closing the reading achievement gap between disadvantaged and non‑disadvantaged students in years 5 and 9

- effectively re-engaging disengaged 12–17 year olds in education and training.

Proposed agencies DET and a selection of schools.

Enhanced maternal and child health services for vulnerable families

2020–21

Objective To determine whether the enhanced maternal and child health (MCH) service is resulting in improved access, participation and outcomes for vulnerable children and their families.

Issues The MCH service is a universal primary care service for families with children from birth to school age. It includes developmental health surveillance, parenting support, and health education and services. Local councils plan and deliver MCH services funded by DET through a partnership agreement between DET and the Municipal Association of Victoria (MAV).

An enhanced MCH service is available for children and families who may be at risk of poor outcomes and need additional support. In 2017, DET received funding to expand the enhanced MCH service, with the aim of providing services to about 37 000 families. Additional funding was also provided to attract new nurses to an ageing MCH workforce—65 per cent are over 51 years old.

This audit will examine the enhanced MCH service's impact on vulnerable children and their families.

Proposed agencies DET, MAV and a selection of local councils.

Student attendance in Victorian schools

2020–21

Objective To assess whether schools are best supporting all children to regularly attend school.

Issues Participation in education maximises students' life opportunities by helping them develop skills, knowledge and values that will enable them to lead fulfilling, productive lives.

While most children and young people attend school regularly, a small proportion leave school early for a variety of reasons. Others facing complex problems may remain enrolled in a school but may be disengaged and have poor attendance. Students who do not participate in school face a number of challenges, including not getting qualifications, increased likelihood of unemployment and experiencing long-term disadvantage.

Children aged six to 17 years must be enrolled at a registered school, or registered for home schooling. Parents and carers have legal responsibility for ensuring children in their care attend school. Schools must record student attendance twice per day in primary schools, and in every class in secondary schools.

This audit will examine whether schools are successfully managing students' attendance at school.

Proposed agencies DET and a selection of schools.

Environment

Managing onsite domestic wastewater systems

2018–19

Objective To determine whether onsite domestic wastewater is effectively managed to prevent environmental impacts.

Issues Effective management of wastewater generated from household use is necessary to protect both public and environmental health. Properties must either connect to the reticulated sewerage system (the sewer) or use an onsite wastewater management system, commonly known as a septic tank, to treat household wastewater before it is discharged to the environment.

Reticulated sewerage systems did not keep pace with Melbourne's significant population growth since the 1950s and, as a result, there is still a large number of properties in Melbourne's north east and south not yet connected to the sewer which rely on septic tank systems.

More than 14 000 properties in the outer northern and eastern suburbs, and 30 000 across the Mornington Peninsula are still not connected to the sewer. Many of these properties have ageing, failing and poorly maintained septic tanks risking pollution of groundwater and waterways.

Water authorities need to effectively plan and integrate these high-risk areas into established and extended sewerage infrastructure networks in the long term. In the short term, councils need to ensure existing septic systems are being used and managed effectively.

This audit will examine whether relevant agencies are effectively managing the environmental and public health risks posed by septic tanks, with a focus on the Mornington Peninsula and Yarra Ranges.

Proposed agencies Department of Environment, Land, Water and Planning (DELWP), Environment Protection Authority (EPA), South East Water, Yarra Valley Water, and Yarra Ranges and Mornington Peninsula shire councils.

Recovering and reprocessing resources from waste

2018–19

Objective To determine whether responsible agencies are maximising the recovery and reprocessing of resources from Victoria's waste streams.

Issues Population growth will almost double the level of Victorian waste in the next 30 years. As the state's population spreads into new residential areas, there will also be an impact on locations available for waste and resource recovery sites.

The decreasing capacity of current landfills and the rising cost of diverting waste to landfill will increase the cost of resource recovery activities. The Statewide Waste Resource Recovery Infrastructure Plan identifies that Victoria's existing infrastructure for waste and resource recovery lacks the capacity and capability to meet projected increases in waste or to fully realise the economic value of waste materials.

This audit will examine whether DELWP, EPA and Sustainability Victoria are working with the Metropolitan Waste and Resource and Recovery Group and relevant local councils to ensure that the state's waste is effectively recovered and reprocessed where appropriate, with a focus on three challenging waste streams—tyres, electronic waste and organic waste.

Proposed agencies DELWP, EPA, Sustainability Victoria, Metropolitan Waste and Resource and Recovery Group, City of Monash, Banyule City Council and Greater Shepparton City Council.

Security of infrastructure control systems for water agencies

2018–19

Objective To determine whether information and communications technology (ICT) systems used to operate, manage and monitor critical water infrastructure are secure.

Issues Victoria's 19 water operators rely on critical infrastructure to deliver their services, including physical assets, facilities, distribution systems, information technology and communication networks. This infrastructure relies on supervisory control and data acquisition (SCADA) systems to digitally monitor and control water infrastructure.

Cyber attackers have been known to target critical infrastructure, including SCADA systems, to endanger public health and safety. If successful, these attacks could result in overflows of untreated sewage, reductions in water pressure, or shutdowns in the distribution of water.

In 2014, CERT Australia—the Australian Government's computer emergency response team—responded to 11 073 cyber security incidents affecting Australian businesses, 153 of which involved systems of national interest, critical infrastructure and government.

This audit will examine whether DELWP and selected water operators have implemented effective measures to protect critical ICT systems in the water sector.

Proposed agencies DELWP, Melbourne Water, Yarra Valley Water, Barwon Water, Emergency Management Victoria and Aquasure/Watersure (private partner desalination plant).

Follow up of 2013–14 performance audit: Oversight and Accountability of Committees of Management

2018–19

Objective To verify agencies’ attestations about the actions they have taken to address recommendations made in response to the performance audit Oversight and Accountability of Committees of Management, tabled in 2013–14.

Issues We ask agencies each year to attest to their progress in responding to and monitoring recommendations from previous performance audits. Using these attestations and other sources of intelligence we then select past performance audits which we follow up.

The follow-up performance audits are limited to the review of the recommendations made by the Auditor-General to the selected agencies, whether and how effectively they have responded to these performance audit recommendations, and whether and how effectively the actions taken have addressed the root issue that led to the recommendation.

Proposed agencies DELWP.

Conserving Victoria's threatened species

2019–20

Objective To determine whether threatened species are being conserved on public and private land.

Issues Victoria's native plants and animals have intrinsically high environmental value as well as contributing major economic benefits to the state.

Historic clearing of native vegetation in much of Victoria has resulted in the widespread loss of habitat and the decline of many species. Victoria is the most cleared state in Australia, with nearly two-thirds of the state's landscape now modified for agriculture and urban development. Combined with further clearing, habitat fragmentation, changed river flows, inappropriate land use and fire regimes, and invasive species and diseases, land clearing has put enormous stress on native species.

In Victoria: State of the Environment 2013 report report identified that only 11 of 294 threatened species showed signs of recovery. There are many signs that the state's threatened species continue to decline and some formerly common species are now threatened.

The Flora and Fauna Guarantee Act 1988 is the primary piece of Victorian legislation for conserving threatened species and ecological communities, and managing the processes that threaten the state's native flora and fauna.

Our 2009 audit report Administration of the Flora and Fauna Guarantee Act 1988 found that the main tools for managing threatened species were either not working or were not being used. A review of the Flora and Fauna Guarantee Act 1988 is currently being finalised.

This audit will examine whether DELWP is appropriately managing and applying the available laws and tools cost-effectively to prevent further declines in threatened species. It will also assess the impact of any reforms arising from the review of the Flora and Fauna Guarantee Act 1988.

Proposed agencies DELWP and Parks Victoria.

Managing clearing of native vegetation

2019–20

Objective To determine whether management of vegetation clearing is protecting sensitive native vegetation.

Issues Victoria is the most cleared Australian state—around 46 per cent of public land retains its original native vegetation, compared to around 21 per cent for private land.

The Victorian Government's native vegetation programs aim to conserve indigenous plant species, including trees, shrubs, herbs and grasses. These programs include various ecological activities such as creating stable animal habitats, preventing land degradation and maintaining the land's productive capacity.

The removal of native vegetation in Victoria is regulated through the Victorian Planning Provisions of the Planning and Environment Act 1987. The native vegetation clearing regulations were reformed in December 2017.

However, the removal of vegetation on private land and the felling of old‑growth trees as part of planned burning and vegetation removal are exempt from normal planning controls. These activities have resulted in a decline in the quality and extent of Victoria's native vegetation.

This audit will examine whether responsible agencies are appropriately applying the native vegetation clearing regulations following recent changes, as well as how effectively Victoria is managing the clearing that occurs outside these regulations.

Proposed agencies DELWP, City of Whittlesea, Surf Coast Shire and Yarra Ranges Council.

Reducing bushfire risk

2019–20

Objective To assess whether agencies are effectively working together to reduce Victoria's bushfire risk.

Issues Victoria is already one of the most bushfire-prone areas in the world. Increases in severe weather conditions due to climate change, as well as a growing population, may lead to even greater bushfire risk in the future.

While it is not possible to eliminate the threat of bushfires, the Victorian Government plays a key role in reducing the risk and the impact of bushfires on people, property and the environment.

Fuel management is the main method that government uses to manage bushfire risk. Reducing the leaves, bark, twigs and shrubs that fuel bushfires can reduce their intensity and make them easier for firefighters to control. Fuel management includes planned burning—that is, lighting and managing fires in the landscape at times of the year when bushfire risk is lower. Other fuel management treatments include mowing, mulching and applying herbicides.

In 2013, the Bushfires Royal Commission Implementation Monitor concluded that the previous planned target of burning 5 per cent of public land to reduce bushfire risk was not achievable, affordable or sustainable. The Inspector‑General for Emergency Management agreed and recommended that government replace the hectare-based target with a risk-reduction target that measures the impact of fuel management activities on the overall risk of bushfire.

In 2015, the government accepted this recommendation. From 1 July 2016, DELWP's fuel management program became driven by a statewide target to maintain bushfire risk at or below 70 per cent of Victoria's maximum bushfire risk. DELWP’s Reducing Victoria’s bushfire risk: Fuel management report 2016–17 estimates the state's bushfire risk at 63 per cent.

This audit will examine whether DELWP is effectively and efficiently reducing the state's bushfire risks.

Proposed agencies DELWP and a selection of agencies.

Rehabilitating mine sites

2019–20

Objective To determine whether the state has minimised its exposure to liabilities from the remediation and rehabilitation of privately operated mines.

Issues Mine rehabilitation repairs the damage caused to a site by mining. This can be a long and expensive process. Licence and lease holders are required to provide financial security in the form of a rehabilitation bond if they are unable to meet their rehabilitation obligations.

Previous limited or poor-quality rehabilitation of mine sites has caused significant environmental issues across large areas of Victoria. Many of these sites remain contaminated or unusable.

The report on the inquiry into the 2014 Hazelwood mine fire made a number of recommendations to the Department of Economic Development, Jobs, Transport and Resources (DEDJTR) to address issues in the Latrobe Valley, including limited or slow rehabilitation of mines, poor rehabilitation plans, insufficient rehabilitation bonds and a regulatory system that lacked transparency and clarity. The government committed to implementing actions to address these recommendations.

This audit will examine whether agencies' responses to the recommendations are effectively rehabilitating mines and minimising the state's exposure to liabilities from remediation and rehabilitation.

Proposed agencies DEDJTR, DELWP and EPA.

Minimising stormwater impacts on Port Phillip Bay

2020–21

Objective To determine whether responsible state and local government agencies are minimising the impacts of stormwater discharge on Port Phillip Bay (the Bay).

Issues Scientific investigations have concluded that the most significant source of pollution in Port Phillip Bay (the Bay) is stormwater from the surrounding catchment. There are currently hundreds of stormwater drains that discharge directly into the Bay.

Poor water quality in the Bay usually occurs after episodic storm events where stormwater carries nutrients, sediment, litter, pathogens and toxicants from the Bay's catchment area. After heavy rains in December 2016, the EPA initially closed 21 and then all 36 of the Bay's beaches. Three of the Bay's beaches remained closed until the first week of 2017. Poor water quality and beach closures can impact both public health and the economic performance of surrounding businesses that rely on people visiting the beach.

Minimising the impacts of stormwater discharge on the Bay requires a coordinated effort by various state and local government agencies using a range of tools for both catchments and the Bay. These tools include stormwater management plans, water-sensitive design for new and retrofitted developments, and the installation of stormwater infrastructure that reduces the volume of both stormwater and pollutants entering the Bay.

This audit will investigate whether state and local government agencies are effectively coordinating their efforts to implement these tools.

Proposed agencies DELWP, Melbourne Water, EPA, Bayside City Council, Port Phillip City Council, Frankston City Council and City of Greater Geelong.

Effectiveness of water markets

2020–21

Objective To assess whether Victoria's water markets are providing an equitable and efficient way to manage our finite water resources.

Issues Victoria's water grid connects sources—such as dams, reservoirs and the desalination plant—via infrastructure, such as pipes and pumps, and natural elements like rivers. Water trading is the process of buying, selling or exchanging rights to water. Water markets allow users to move water in connected systems to where it is most valued. Local, regional and statewide networks operate both independently and together to allow water to be moved from where it is captured and stored to where it is needed.

Water markets allow for sharing of water security benefits. Farmers, the Victorian Environmental Water Holder and water corporations buy and sell water entitlements and seasonal allocations, so they can manage their risk based on their willingness to pay. Environmental water holders trade allocations to ensure environmental water is available when and where it is needed to maintain the health of Victoria's waterways.

Climate change and population growth will reduce the amount of water available. The effectiveness of the water grid and markets is important for future water security and minimising adverse impacts on the environment and water users.

This audit will examine the effectiveness of Victoria's water markets in providing improved water security for all water users.

Proposed agencies DELWP and a selection of agencies.

Victoria's renewable energy targets

2020–21

Objective To determine whether Victoria is on track to meet its renewable energy targets.

Issues Victoria's share of electricity generated from renewable resources has increased substantially, from 4.8 per cent in 2009 to 15 per cent in 2017. In June 2016, the government committed to renewable energy generation targets of 25 per cent by 2020 and 40 per cent by 2025. Growing investment in renewables, energy storage and electricity distribution connections is key to lowering carbon emissions and reducing greenhouse gases.

Victoria's Climate Change Act 2017 established a target for the state to have net zero greenhouse gas emissions by 2050. Victoria's Climate Change Framework makes it clear that moving to a clean energy supply by increasing renewable energy generation is a key pillar of the state's approach to reducing emissions.

Transitioning from centrally located infrastructure for producing, transmitting and distributing fossil-fuel energy to the flexible and decentralised energy grids associated with renewable energy will be potentially challenging and costly.

This audit will examine whether DELWP is effectively planning and implementing programs to ensure that the state is on track to meet the 2020 and 2025 Victorian renewable energy generation targets.

Proposed agencies DELWP.

Health and Human Services

Managing private medical practice in public hospitals

2018–19

Objective To determine whether the Department of Health and Human Services (DHHS) and health service providers are effectively managing private practice to optimise outcomes for the health sector.

Issues In the Victorian public health system, clinicians have a 'right of private practice' (RoPP) as part of their terms and conditions of employment (enterprise bargaining agreement and individual contracts). RoPP intends to increase patient choice, supplement clinicians' salary to attract and retain them in the public system, and bolster public hospital income.

The Commonwealth Government funds medical practitioners working in a private capacity through the Medical Benefits Scheme (MBS). This funding extends to medical practitioners exercising RoPP within public hospitals.

Despite local variation, there are two main RoPP models used in Victoria:

- 100 per cent donation model—the clinician receives an additional salary in lieu of the MBS payment, while the health service retains the MBS payment and bears the costs of the practice

- 100 per cent retention model—the clinician retains the MBS payment and pays a fee to the health service to access facilities and administrative support.

There is no accurate data on the number of medical practitioners using private practice, the number of patients treated and the cost or benefits to the system. Consultation with stakeholders indicates that the practice is extensive, but the effectiveness of the program in attracting and retaining clinicians and improving access and choice for patients is unknown.

This audit will examine whether the RoPP model is providing positive outcomes for Victorian public health services, including increased treatment.

Proposed agencies DHHS, a metropolitan tertiary health service, Latrobe Regional Hospital and Western Health.

Child and youth mental health

2018–19

Objective To determine whether child and adolescent mental health services are effectively preventing, supporting and treating child and youth mental illness.

Issues Mental illness is the number one health issue facing young people worldwide. One in four young Australians aged 16–24 years will experience mental illness in any given year. Three-quarters of all mental illness manifests itself in people under the age of 25.

For children and young people, intervention early in life and at an early stage of mental illness can reduce its duration and impact. Services that recognise the significance of family and social support and functional recovery are particularly important for children and young people.

Most children and young people with mental illness receive clinical treatment in the community, but a small proportion require inpatient treatment. In 2016–17, there were 10 723 registered child and adolescent clients and 1 835 hospitalisations.

This audit will assess whether Victoria's mental health services for children and adolescents are effective.

Proposed agencies DHHS, Eastern Health, Royal Children's Hospital, Austin Health, Monash Health and Albury Wodonga Health.

Security of patients' hospital data

2018–19

Objective To determine whether patient data within the public health system is safe and secure.

Issues Public sector agencies, including those in the health sector, increasingly rely on information and communications technology (ICT) to deliver services to the public. However, as with other organisations, public hospitals' ICT environments are being threatened more frequently by cyber attacks of increasing scale and sophistication. Successful cyber attacks can have severe consequences for the health sector, such as impacting its ability to treat patients.

This audit will examine whether public health services' ICT security policies, procedures and practices effectively protect patient data.

Proposed agencies DHHS, Royal Children's Hospital, Health Technology Solutions Victoria, Barwon Health and Royal Victorian Eye and Ear Hospital.

Efficiency and economy of Victoria's public hospitals

2019–20

Objective To determine the relative efficiency and economy of Victorian metropolitan acute public hospitals.

Issues Population changes, new technology and increasing costs are influencing the efficient and economical delivery of health care. Since the early 1990s, worldwide healthcare spending per capita has risen by over 70 per cent in real terms. An ageing population and costly developments in medical technology are putting more pressure on healthcare budgets. At the same time, obesity, cardiovascular diseases, hypertension and diabetes are becoming persistent, widespread health problems that are further driving increases in the demand for health care.

These challenges are increasing pressure on acute health services to meet demand that is growing in both size and complexity.

This audit aims to assist public health services to understand and respond to demand pressures by examining and analysing cost and demand drivers across acute metropolitan health services.

Proposed agencies DHHS, Melbourne Health, Alfred Health, Austin Health, Eastern Health, Western Health, Northern Health, St Vincent's Health, Barwon Health and Peninsula Health.

Clinical governance

2019–20

Objective To determine whether DHHS has addressed the accepted recommendations of Targeting zero: Supporting the Victorian hospital system to eliminate avoidable harm and strengthen quality of care, the 2016 review of hospital safety and quality assurance in Victoria, and that these actions have improved clinical governance across the public health system.

Issues In 2016, the Minister for Health commissioned a wide-ranging review of clinical governance in response to the avoidable deaths of seven infants at Bacchus Marsh Hospital, part of Djerriwarrh Health Service. The review, led by Dr Stephen Duckett, identified systemic clinical governance issues, which increase the risk of harm occurring in hospitals across the system. The Duckett review made 178 recommendations focused on improved data collection and analysis, better engaging clinical expertise and enhancing safety in the system.

DHHS accepted all the recommendations and incorporated them into a response plan, Better, Safer Care: Delivering a world-leading healthcare system. Implementing these recommendations requires DHHS to significantly improve how it collects and analyses data, and how it enacts its role in ensuring strong clinical governance in the public hospital system. The changes are underpinned by new structures and two specialist agencies—the Victorian Agency for Health Information and Safer Care Victoria.

This audit will examine whether DHHS has implemented the accepted recommendations and the impact of key response activities on clinical governance across the sector.

Proposed agencies DHHS, Safer Care Victoria and Victorian Agency for Health Information.

Targeted care packages

2019–20

Objective To determine whether targeted care packages (TCP) are successfully transitioning children from residential care to the community.

Issues Children experiencing family violence may be placed in residential care, but this is a costly solution that provides poor outcomes for children in both the short and long term. In Victoria, the number of children entering care is increasing, and recent family violence reforms and changes to mandatory reporting requirements may place further strain on Victoria's child protection system.

In March 2015, the government introduced TCPs to enable eligible children and young people to transition from residential care to more appropriate care arrangements, where their care needs will be better met. Children aged 12 and under, and Aboriginal children have priority access to the program. In October 2015, children at risk of entering residential care and children with a disability were added to the TCP program's priority cohort.

DHHS had done a preliminary review of TCPs and found some areas for improvement. All TCPs reviewed in DHHS's review had been operating for six months or less, and the review did not examine outcomes.

This audit will examine DHHS's implementation and oversight of the TCP program and outcomes achieved.

Proposed agencies DHHS.

Victoria's homelessness response

2019–20

Objective To determine whether DHHS has reduced the incidence and impacts of rough sleeping through implementation of Victoria's homelessness and rough-sleeping action plan.

Issues Homelessness results in significant social and economic costs, not just to individuals and families but also communities and the nation as a whole. On an individual level, homelessness makes it difficult to maintain school or further study and leaves people vulnerable to long-term unemployment and chronic ill health.

The Australian Bureau of Statistics estimates that there are more than 20 000 Victorians who are homeless. Further, DHHS notes that there are approximately 1 100 people sleeping rough in Victoria each night.

In January 2018, the government launched Victoria's homelessness and rough‑sleeping action plan. The plan is the first phase in the development of a long-term homelessness strategy. Victoria has a number of plans to address homelessness including elements of the response to the Royal Commission into Family Violence.

This audit will examine DHHS's implementation of the plan and the extent to which it has achieved intended outcomes.

Proposed agencies DHHS.

Clinical trials in public hospitals

2020–21

Objective To determine whether the governance of clinical trials in public hospitals enforces responsible conduct.

Issues Clinical research in medicine helps to determine the safety and effectiveness of medications, devices, diagnostic products and treatment regimens intended for human use.

The Therapeutic Goods Administration (TGA) is a division of the Commonwealth Department of Health and Ageing, which is responsible for regulating medications and devices. TGA conducts a pre-market assessment before goods are available for sale and use. To show the efficacy of the goods, this pre-market assessment relies on clinical research often conducted within public hospitals.

Public hospitals are responsible for ensuring their staff adhere to the significant range of governance and regulatory requirements while undertaking clinical trials. In addition, the pharmaceutical industry makes a significant investment in research, which means that public entities should have rigorous processes in place to avoid conflicts of interest.

This audit will examine whether audited agencies have a robust governance framework for ensuring clinical trials align with governance and regulatory requirements.

Proposed agencies DHHS and a selection of public health services.

Managing drug and alcohol rehabilitation services

2020–21

Objective To determine whether DHHS's management of drug and alcohol rehabilitation services is efficient and effective in reducing harm.

Issues The Victorian Government funds drug and alcohol treatment services across the state, including residential and non-residential withdrawal, rehabilitation and pharmacotherapy services. There is also funding available for services providing care and recovery coordination for individuals with complex needs. Treatment services can also help individuals to access other pathways during recovery, such as employment and education.

In 2014, the government used a competitive tender process to recommission alcohol and other drug treatment services, and providers rolled out new services in August 2014. Following criticism from the sector, the government commissioned an external review in September 2015. The review made a range of recommendations to DHHS, including reviewing its central intake process and moving intake assessments back to service providers, improving data collection and reporting, and undertaking a comprehensive review of the drug treatment funding model.

This audit will examine DHHS's implementation of these recommendations and whether services are effective and efficient in reducing harm.

Proposed agencies DHHS and a selection of funded service providers.

Managing Support and Safety Hubs

2020–21

Objective To determine whether DHHS's Support and Safety Hubs are providing effective and efficient service coordination for families.

Issues Family violence has been a major issue in Victoria, with many high-profile murders. The Royal Commission into Family Violence and government's Roadmap to Reform recommended that Victoria introduce family violence safety hubs in a bid to end family violence in Victoria, and help women and children experiencing family violence. In response to this, DHHS established Support and Safety Hubs. The aim of the hubs is to connect people directly to services and provide a coordinated response to a range of different needs identified through risk and needs assessments.

At this stage, it is unclear how Support and Safety Hubs will operate. Victoria is making a significant investment, with a $1.9 billion package announced in the 2017–18 State Budget. Specifically, the government has committed $448 million over four years to establish 17 Support and Safety Hubs statewide by 2021. It will be important that this funding is targeted properly to achieve intended outcomes.

This audit will examine how Support and Safety Hubs are operating and whether they have been effective in addressing family violence issues in Victoria.

Proposed agencies DHHS and a selection of funded service providers.

Managing sexual and reproductive health

2020–21

Objective To determine whether Victorian women have sufficient access to sexual and reproductive health services to support their health and wellbeing.

Issues Sexual and reproductive health issues affect the wellbeing of Victorian women. These issues include endometriosis, polycystic ovarian syndrome, and the symptoms of menopause. The Victorian Government has launched the Women's sexual and reproductive health key priorities 2017–2020. There are four key priority areas:

- Victorians having improved knowledge and capacity to manage fertility

- Victorians having improved access to reproductive choices

- Victorian women with endometriosis and polycystic ovary syndrome or undergoing menopause having improved access to reproductive health services

- Victorian women feeling confident about accessing respectful and culturally safe sexual health services for testing, treatment and support, regardless of their gender identity, cultural identity, ethnicity, age, sexual orientation, disability or residential location.

This audit will examine whether women's access to reproductive health information and services has improved.

Proposed agencies DHHS and selection of health services.

Infrastructure and Transport

Security and privacy of surveillance technologies in public places

2018–19

Objective To determine whether information collected from local government video surveillance activities in public places is secure and the privacy of individuals is protected.

Issues Surveillance devices are becoming more readily available, affordable and sophisticated. They are increasingly used in public spaces as a crime prevention measure and as a tool to detect and identify offenders.