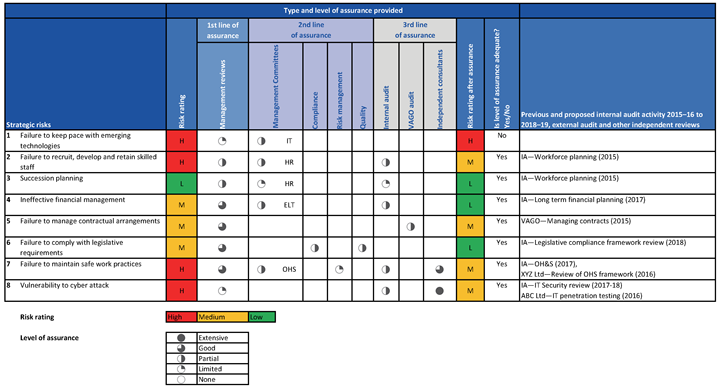

Appendix E Better practice performance measures

Figure E1 shows an example of balanced scorecard reporting of better practice performance measures.

Figure E1

Better practice performance measures

|

Key performance indicator |

Type of measure |

Measure |

Target |

Reporting frequency |

|---|---|---|---|---|

|

Internal audit processes | ||||