Quality of Major Transport Infrastructure Project Business Cases

Snapshot

Do business cases for major transport infrastructure projects support informed investment decisions?

Why this audit is important

Developing a business case for a major transport infrastructure project involves significant resources, time and expenditure, and requires close oversight and assurance.

Business cases give the government information it needs to make important choices about potential investments.

Transport infrastructure projects make up around 70 per cent of the state’s planned capital expenditure.

Who and what we examined

We looked at 4 transport infrastructure business cases against the Department of Treasury and Finance’s (DTF) Investment Lifecycle and High Value High Risk (ILHVHR) guidelines:

- the Suburban Rail Loop (SRL) rail and precinct development project

- the Melbourne Airport Rail (MAR) project

- 2 much smaller scale road projects—Barwon Heads Road Upgrade and the Mickleham Road Upgrade.

We audited the Department of Premier and Cabinet, Department of Transport (DoT), DTF, Major Transport Infrastructure Authority (MTIA) and Suburban Rail Loop Authority (SRLA).

What we concluded

Business cases for 3 of the 4 projects we reviewed do not support fully informed investment decisions.

The audited agencies’ business case development and oversight processes for the projects were usually consistent with DTF and agency requirements. However, 3 business cases lacked sufficient analysis of alternative project options and 2 lacked an assessment of the value for money the projects could provide under different scenarios. Agencies provided other advice but did not finalise these 3 business cases until after the government made significant financial commitments to them.

Without a comprehensive business case, decision-makers do not know whether the investments they make will maximise benefits to Victorian communities.

Our recommendations

We made 6 recommendations to DTF, DoT, MTIA and SRLA about:

- improving the ILHVHR guidelines and Gateway review process

- providing the government with a full business case for the entire SRL program of investments

- disclosing the justification for and impacts of departures from DTF’s ILHVHR guidance in any published version of the MAR business case.

Video presentation

Key facts

Source: VAGO, based on audited agencies’ information.

What we found and recommend

We consulted with the audited agencies and considered their views when reaching our conclusions. The agencies’ full responses are in Appendix A.

The quality of business cases for major projects is important because they provide the basis for investment decisions. Agencies need to ensure that the information contained in business cases is timely and comprehensive so that governments can make informed decisions.

The Department of Treasury and Finance's (DTF) Investment Lifecycle and High Value High Risk Guidelines (ILHVHR guidelines) do not have the status of a statutory instrument with mandatory requirements. However, the content and presentation requirements of the ILHVHR guidance do provide a framework and basis against which DTF and decision makers can compare and assess all standard and non standard business cases. The guidelines state that they are applicable to any investment proposal and support the development of business cases, which are mandatory for capital investments with a total estimated investment of $10 million or more.

We concluded that 3 out of the 4 business cases we assessed in this audit do not support fully informed investment decisions because their content was not sufficient or timely and did not meet the requirements set out in DTF’s guidance.

The Department of Premier and Cabinet (DPC), DTF, Department of Transport (DoT), Suburban Rail Loop Authority (SRLA) and Major Transport Infrastructure Authority (MTIA) do not agree with our assessment of the Suburban Rail Loop (SRL) and Melbourne Airport Rail (MAR) business cases. They told us that the MAR project is a very large scale and complex project and that SRL is much more than a typical transport project because it includes an unprecedented, city-shaping and multi generational program of integrated and precinct development works. They said our assessment of the SRL and MAR business cases against DTF’s standard business case development process and guidance, which they say is typically followed for projects with a narrower scope and influence, is inappropriate and misleading.

DTF’s guidance is designed to cater for large-scale investment projects and programs that have higher risks and opportunity costs than smaller scale projects. Commonly accepted better practice suggests that a well-formulated business case should precede and inform investment decisions. Circumstances where governments make commitments to projects before receiving a complete business case do not relieve agencies from their responsibility to develop a comprehensive business case to inform subsequent government decisions.

Timing of business cases

DoT and relevant transport agencies developed the SRL, MAR and Barwon Heads Road Upgrade (BHRU) business cases between 2018 and 2021 and gave regular advice to central agencies and the government to inform progressive decision making on the projects. However, they did not give the government complete business cases in time to inform key decisions on investment commitments and project solutions for these 3 projects.

Figure A shows our assessment of whether DoT, SRLA and MTIA gave the government a business case before it committed to the project, as required by DTF’s ILHVHR guidance.

Figure A: Assessment of business case timing for the 4 projects

|

|

Business case |

|||

SRL |

MAR |

BHRU |

MRU1 |

|

| Did the business case timing meet DTF’s ILHVHR guidance? | A | A | R | G |

Note: *MRU1 stands for Mickleham Road Upgrade.

We have used a green (G), amber (A), red (R) scale, where:

G= no or minor departures from relevant guidance and/or expected processes

A = some departures from relevant guidance and/or expected processes

R = significant departures from relevant guidance and/or expected processes.

Source: VAGO.

The timing of 3 of the business cases does not align with DTF's guidance:

- For SRL and MAR, the business cases came after the government made funding commitments to the projects.

- For BHRU, while DoT and MTIA completed draft versions of the business case before the government made a funding commitment in 2018, they did not complete the final version and receive government approval until August 2020.

For MRU1, DoT and MTIA provided the government with a complete business case in time to inform key decisions.

The MAR business case did not fully meet its key purpose under the ILHVHR guidance to inform key government decisions on investment commitments and project solutions. This was because it was provided too late to inform decision-making.

DoT disagrees and told us that:

- our finding does not reflect the ‘progressive government decision-making’ that is required for a project of its scale and complexity

- this decision-making occurred in parallel with the development of the business case to inform the planning, approval and procurement of the project.

The decisions for the MAR project (before the final business case was completed) were informed by other detailed briefings and advice from DoT, MTIA, DTF and DPC. However, this advice did not fully meet the standard expected in a business case and agencies used it to justify the limited analysis they included in the final business case.

The timing and approach adopted by DoT and SRLA for assessing the SRL investment program is also not consistent with DTF’s ILHVHR guidelines. However, it does support the government’s decision-making for SRL, where project development and delivery are progressing in parallel. Despite this, the government does not yet have a business case for the entire SRL program of planned investments.

Recommendation about the timing of business cases

| We recommend that: | Response | |

|---|---|---|

| Department of Treasury and Finance | 1. amends the Investment Lifecycle and High Value High Risk Guidelines to provide departments and agencies with clarity that a comprehensive business case is still required in circumstances where the government has made project-specific commitments, announcements and/or decisions before a business case is completed (see sections 2.1, 3.1 and 4.1). | Accepted in principle |

Business case content and analysis

The DTF ILHVHR guidelines indicate that a business case should provide a detailed examination of an investment proposal. They state that:

’The purpose of submitting a business case is to provide confidence to decision-makers that:

- the strategic justification for the investment is valid

- the right investment option is selected

- the agency can deliver the investment as planned’.

Figure B shows our assessment of whether the content in the business cases we examined comprehensively meets DTF's ILHVHR guideline requirements in key content areas.

We found:

- significant issues and departures from the guidance in the SRL and MAR business cases in the options assessments and economic analyses

- that the business cases for the BHRU and MRU1 roads projects largely complied with DTF’s guidance requirements. However, DoT and MTIA’s options assessment and analyses in the BHRU business case were too narrow.

Figure B: Assessment of business case content for the 4 projects

Business case content area |

||||

SRL |

MAR |

BHRU |

MRU1 |

|

| definition | A | A | G | G |

| Case for change (benefits) | A | G | G | G |

| Options assessment | R | R | A | G |

| Economic appraisal method and presentation | R | R | G | G |

| Delivery case | A | A | G | G |

We have used a green (G), amber (A), red (R) scale, where:

G= no or minor departures from relevant guidance and/or expected processes

A = some departures from relevant guidance and/or expected processes

R = significant departures from relevant guidance and/or expected processes.

Source: VAGO.

Problem definition, evidence and benefits

Under DTF’s ILHVHR guidance, business cases supporting bids for government funding need to describe and provide evidence for the problems they are trying to solve and the benefits they are trying to achieve.

The departures from the guidance that related to problem definition and evidence occurred mainly in the SRL and MAR business cases. Specifically, the problems described:

- in the SRL business case do not:

- clearly identify how the proposed benefits flow from the problems identified

- adequately demonstrate how some of the benefits are a direct consequence of the SRL project

- immediately point to the need for a transport-related intervention

- in the SRL and MAR business cases are not supported with comprehensive evidence for or detailed descriptions of:

- their root causes or underlying drivers

- why the government needs to act now.

Options assessment

DTF’s business case guidance expects an agency to explore and assess a broad range of interventions and options so it can recommend a preferred one based on evidence of relative costs and benefits. The guidance states, ’Business cases that are weakest in this area often propose just three options: do nothing, do something that is infeasible, or do what the business case is proposing'.

The SRL, MAR and BHRU business cases fall short of this standard because, although none of the options were infeasible:

- the MAR business case completes a cost–benefit analysis (CBA) only on a single option relative to the do-nothing base case

- SRL has only 2 options relative to the base case and those options only differ in the timeframe to build the rail loop and undertake related precinct initiatives

- DoT, SRLA, DPC and MTIA relied on high-level early assessments of potential strategic interventions and options to narrow their subsequent analysis of both SRL and MAR, which is not consistent with DTF’s guidance

- for the BHRU, DoT and MTIA restricted their project options analysis by narrowing it to the parameters of the government’s funding commitment, which preceded the full business case.

The SRL and MAR projects are large scale and complex, and their benefits are for the long term.

We expected that business cases for significant long-term transport infrastructure projects, such as the SRL and MAR projects, would consider options to defer or delay the proposed intervention to account for uncertainty. Neither did.

Given the limited number of options assessed both in the high-level early assessments and in the actual business cases, there is a risk that DoT, MTIA and SRLA have not provided the government with advice that maximises value for money.

Relevant guidance for the economic appraisal of transport projects includes guidance from DTF, DoT, Infrastructure Australia and the Australian Transport Assessment and Planning (ATAP) guidance.

Discount rates are like interest rates. They express the value or cost of money at a particular time. Organisations use them in discounted cashflow analysis to value a project.

Wider economic benefits (WEBs) are benefits associated with changes in accessibility or land use that are not captured in traditional cost–benefit analyses. DTF and DoT guidance say WEBs should be considered separately from primary benefits and excluded from headline BCR results.

A benefit–cost ratio (BCR) is a number that represents the value of a project’s benefits divided by its costs. Projects with a BCR of less than 1.0 do not usually proceed.

Economic appraisal method and presentation

The economic analyses in the SRL and MAR business cases lack transparency and are not consistent with key elements of relevant guidance.

The methodology used for the economic and cost–benefit analyses in the SRL and MAR business cases creates a material risk that the economic value of these projects is overstated.

Specifically:

- the discount rate used in the economic appraisals in the SRL and MAR project business cases of 4 per cent was approved by the Minister for Transport Infrastructure (the minister) and accepted by the Treasurer. DTF’s guidelines recommend a discount rate of 7 per cent for projects in core service delivery areas of government with benefits that are easy to monetise, such as public transport and roads

- the economic appraisal results for both projects are sensitive to small changes in the discount rate. DoT, MTIA and SRLA did not provide government decision-makers with the results of discount rate sensitivity analysis

- DoT, MTIA and SRLA included wider economic benefits (WEBs) and other non standard benefits when presenting the primary economic analysis benefit–cost ratio (BCR) results in the SRL and MAR business cases. This materially improved the economic results for the projects. In particular:

- for SRL, the business case highlights BCRs ranging between 1.0 and 1.7. The BCR for the project is 0.51 when calculated in line with DTF’s guidance by excluding WEBs and other non-standard benefits and using a discount rate of 7 per cent

- for MAR, the business case shows BCRs ranging between 1.1 and 1.3 when assuming that an SRL connection to the airport will be built. The BCR for the project is 0.48 when calculated in line with DTF’s guidance by excluding WEBs and other non-standard benefits and using a discount rate of 7 per cent.

DTF and DoT guidance says that the primary CBA results of business cases should be shown exclusive of WEBs, with WEB-inclusive results presented separately.

DoT, MTIA and SRLA’s inclusion of WEBs in primary economic analysis results and lack of discount rate sensitivity tests in the SRL and MAR business cases mean decision makers did not have all necessary information at their disposal.

Recommendations about business case content and analysis

| We recommend that: | Response | |

|---|---|---|

| Department of Transport and the Suburban Rail Loop Authority | 2. provide the government with a full business case for the entire Suburban Rail Loop program of investments that includes economic analysis results for all stages of the proposed investment program (see Section 2.1) | Not accepted by: Department of Transport or the Suburban Rail Loop Authority |

|

3. include updated economic analysis results in funding submissions for all future stages of the program (see Sections 2.1 and 2.2) |

Not accepted by: Department of Transport or the Suburban Rail Loop Authority

|

|

|

Department of Transport and Major Transport Infrastructure Authority |

4. disclose in any published version of the Melbourne Airport Rail business case the justification for and impacts of departures from the Department of Treasury and Finance's Investment Lifecycle and High Value High Risk Guidelines guidance for the conduct of and disclosure of results from economic analysis (see Section 3.2) |

Not accepted by: Department of Transport or the Major transport Infrastructure Authority |

|

Department of Treasury and Finance |

5. amends the Investment Lifecycle and High Value High Risk Guidelines to require departments and agencies to include information in business cases to acknowledge, justify and disclose the impacts of any significant departures from the guidance (see sections 2.2 and 3.2). |

Accepted in principle |

Business case development processes

Project development, governance and quality assurance

Processes used by DoT and agencies to manage, oversee and quality assure the 4 audited business cases were largely consistent with DTF and agency-specific requirements and demonstrated active management of the business case development process.

However, DoT and SRLA’s decision to adopt a program-level business case approach for the SRL project, which is acceptable under DTF’s ILHVHR guidance, meant that they should have developed a preliminary and full business case for the entire project. They did not.

Instead, DoT and SRLA provided the government with a business case for the eastern and northern parts of the project only and funding submissions for specific components of the eastern part of the program only. This meant that they did not demonstrate the economic rationale for the entire project, and they have told us that they have no plans to do so. DoT and SRLA’s approach does not fully meet DTF’s guidance requirements and creates risks that their advice to government on these investments is not sufficiently comprehensive.

While not supported by a full business case for the SRL project, other advice and progressive reviews provided by DoT, SRLA, DTF and DPC to the government informed its decisions on funding submissions that have secured over $11.5 billion.

Projects are identified as high value and/or high risk (HVHR) by DTF or government. They are subject to more rigorous scrutiny and approval processes than other projects.

Gateway reviews are performed by a team of independent, experienced reviewers engaged by DTF at key points of the project/program life cycle as a critical check on business cases and to provide insights and learnings to assist project delivery.

Compliance with external assurance and review requirements

DTF’s high value high risk (HVHR) project assurance process requires a project assurance plan, Gateway reviews and a DTF assessment of the deliverability of the business case for projects designated as HVHR.

When projects receive funding from the Australian Government, Infrastructure Australia also reviews the business case.

Figure C summarises our assessment of compliance with external assurance and review requirements for the 4 business cases.

Figure C: Assessment of compliance with external assurance and review requirements

Assurance and review requirements |

||||

SRL |

MAR |

BHRU |

MRU1 |

|

| Project assurance plan | G | G | G | N/A |

| Gateway reviews | A | A | A | N/A |

| HVHR business case deliverability assessment | A | A | G | N/A |

| Infrastructure Australia review of business case | To be confirmed | G | G | N/A |

We have used a green (G), amber (A), red (R) scale, where:

G= no or minor departures from relevant guidance and/or expected processes

A = some departures from relevant guidance and/or expected processes

R = significant departures from relevant guidance and/or expected processes.

Source: VAGO.

While DTF provided ongoing input to agencies and advice to the Treasurer on all 4 business cases, it has not fully applied the HVHR major project assurance framework to the SRL and MAR project business cases because it is yet to complete the required HVHR deliverability assessment on them.

This means that a key intent of the HVHR assurance process—to provide confidence to government that business cases are robust before they are approved—has not been fully met for 2 of the largest infrastructure projects ever undertaken in Victoria.

MRU1 is not an HVHR project and therefore it did not require Gateway reviews or an HVHR deliverability assessment of the business case.

Gateway reviews

Gateway reviews were not fully effective in making recommendations on shortcomings with the SRL and MAR business cases.

Both SRL and MAR undertook combined Gate 1 and Gate 2 reviews with a stated purpose to:

'… confirm that the business case is robust—meets the business need, is affordable, achievable with appropriate options explored, likely to achieve value for money and aligns well with the department’s overall strategy’.

The combined reviews lack evidence that due consideration was given to affordability, options assessment or value-for-money requirements. Given this, these Gateway reviews fell short of their stated scope and missed a key opportunity for crucial elements of each business case to be tested and challenged.

For the BHRU project, DoT and MTIA did not fully respond to recommendations from the Gateway review of the draft business case that related to:

- providing a stronger alignment between the project and land-use objectives

- considering a wider range of transport options

- providing a more rigorous justification for the project option assessment framework.

DTF’s deliverability assessments

A fundamental purpose of the HVHR process is for DTF to apply added scrutiny to the business cases for HVHR projects before they are approved and funded by the government. The process exists to inform the government’s deliberations on the merits of business cases.

DTF is yet to complete an HVHR deliverability assessment on the SRL and MAR business cases, even though the government has committed significant funding and begun procurement for major works packages on both projects.

However, DTF told us that:

- it has provided ongoing advice to the government on the SRL and MAR business cases that addresses the substance of the required deliverability assessments

- the HVHR deliverability assessment will be completed once the final MAR business case is ready for approval by government

- it is undertaking a business case deliverability assessment based on the SRL business case, SRL East main works funding submission and other relevant information but has not indicated when it expects to complete this.

DTF did conduct a deliverability assessment on a short-form version of the business case for the BHRU project.

Recommendation about business case development processes

| We recommend that: | Response | |

|---|---|---|

| Department of Treasury and Finance | 6. amends the template for Gateway review reports to require review teams to explain any departures from the recommended scope for each review gate (see sections 2.1 and 3.1). | Accepted |

Audit context

Victoria’s population growth has prompted a significant increase in government investment in infrastructure. Capital investments of nearly $129 billion in transport represent around 70 per cent of the state’s capital program in the 2022–23 Budget.

The unprecedented scale of investment in major transport infrastructure projects and the attendant impact on the state’s debt burden underline the central importance of government decisions on these investments being well informed. A well formulated, comprehensive business case that precedes investment decisions is commonly accepted to be better practice.

Among a range of other issues, VAGO performance audit reports since 2010 on the planning and delivery of major transport projects have variously found problems with business case content, development processes and timing.

This chapter provides essential background information about:

1.1 What is a business case and why is it important?

Investment life cycle

The investment life cycle is the process of planning, proposing and delivering investments.

Responsible fiscal management demands that governments are as well informed as practicable before making decisions about whether and how to proceed with an investment.

DTF set up the ILHVHR guidelines, including templates and technical guidelines, to help departments analyse investments and inform government decision-making throughout the investment life cycle.

The ILHVHR guidelines seek to promote consistently good practice in the detailed examination of proposed investments. The guidelines do not have the status of a statutory instrument with mandatory requirements. However, they do state that they are applicable to all investment proposals. Where we refer to ‘requirements’ throughout this report we are typically referring to DTF’s guidance.

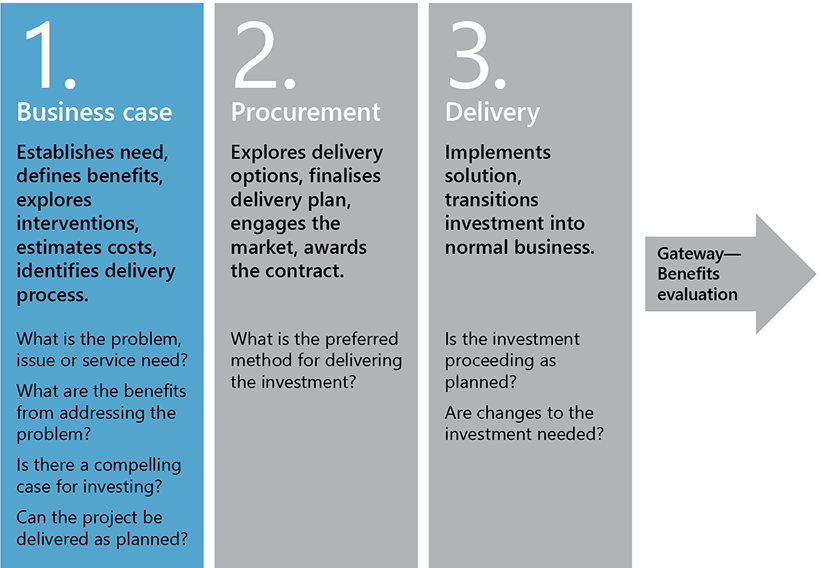

There are 3 key stages to the investment life cycle under the guidelines, as shown in Figure 1A. The business case is the first stage in this cycle.

FIGURE 1A: Investment life cycle framework

Source: VAGO, based on Investment Lifecycle and High Value High Risk Guidelines: Business Case (2019).

The ILHVHR guidelines help shape proposals, inform investment decisions, monitor project delivery and track the benefits projects achieve throughout the investment life cycle.

The business case: purpose, timing and guidance

A business case should provide confidence to decision-makers that there is a compelling case for investing. This requires understanding whether the investment:

- is of net benefit, meaning it is expected to generate benefits that exceed costs

- is the best use of government funding, meaning better value than other alternatives to solving a problem.

According to the ILHVHR guidelines, the core purpose of a business case is to provide a detailed examination of an investment proposal. The ILHVHR guidelines state that:

’All investment proposals over $10 million seeking budget funding are required to submit a full business case. The purpose of submitting a business case is to provide confidence to decision-makers that the:

- strategic justification for the investment is valid

- right investment option is selected

- agency can deliver the investment as planned’.

The business case should be provided at the time funding is sought for an investment. It has a fundamental role in showing the investment rationale, analysing response options and establishing whether proposed investments have sufficient value and can be delivered.

While the ILHVHR guidelines communicate a clear purpose to provide practical assistance to anyone developing investment projects in Victoria, the guidelines also state that:

- all capital projects over $10 million require a business case and should follow DTF’s business case guidance

- DTF will use its economic evaluation technical guidelines to determine whether rigorous economic evaluations have been undertaken and whether the findings of such evaluations should be accepted by the government at face value.

DTF’s ILHVHR guidance is not meant to unduly restrict agencies in the approaches they adopt in differing contexts. However, it does outline critical steps, methods and questions that should be taken and answered to comprehensively inform government decisions about whether to proceed with an investment. Comprehensively addressing the guidelines is more important for larger, more complex and costly projects.

Figure 1B shows the 2 main types of business cases.

FIGURE 1B: Two types of business cases

| Business case type | Features |

|---|---|

| Preliminary business case |

|

|

Full business case |

|

Source: VAGO, based on DTF's ILHVHR guidelines.

1.2 Required structure and content of a business case

Under the ILHVHR guidelines business cases have 2 key sections:

- The investment case sets out the rationale for the investment, provides evidence of the scale of need, measures the impact of the problem and analyses response options.

- The delivery case shows how the preferred solution can successfully deliver the intended benefits on time and on budget.

The business case currently consists of 10 chapters. Figure 1C outlines each chapter and its purpose. The ILHVHR guidelines indicate that comprehensive evidence and effort is required across all 10 chapters for a full business case on a project classified as HVHR

FIGURE 1C: Business case chapters and levels of evidence and effort required

| Section | Chapter | Purpose |

|---|---|---|

| Investment case | Problem definition | Define the problem the project is trying to solve with supporting evidence. The problem should identify a cause and an effect |

| Case for change (benefits) | Define the benefits or direct advantage gained by Victoria as a result of undertaking the investment and solving the defined problem | |

| Response option development | Outline a mix of high-level strategic interventions to respond to the problem, known as response options. A preferred response option should be identified from a range including a base case or a realistic option of what will occur if continuing under the current policy setting | |

| Project options assessment | Project options explore how the preferred response option might be implemented | |

| Delivery case | Project solution | Present the evidence relied on in the options analysis in arriving at the preferred project option, including major assumptions on the project scope, why costs and benefits have been included or excluded and valuation methodologies employed to estimate costs and benefits |

| Commercial and procurement |

Analyse procurement options and a recommendation on the preferred procurement method The business case must demonstrate that the investment would be procured by the most appropriate method and provide an overview of the recommended procurement strategy |

|

| Planning environment, heritage and culture | Outline relevant planning, environment, heritage and culture considerations and approvals required to deliver the project solution | |

| Project schedule | Outline a detailed project schedule and list all major milestones so that decision makers understand the extent of pre-construction works required | |

| Project Budget | Develop estimate-level costing data used for the project options assessment to a preliminary design estimate level. This forms the basis for the budget funding consideration | |

| Management | Outline project governance so that roles and responsibilities are clear and decision makers know who is accountable for effective project delivery |

Source: VAGO, based on DTF’s ILHVHR guidelines.

What is involved in response and project option assessments?

Assessing response and project options are key functions of a business case. Business cases should identify and assess a range of realistic and feasible project options to address the underlying problem and meet investment benefits. The ILHVHR guidelines state that business cases are weakest if they propose only 3 options: do nothing, do something infeasible or do what the business case is proposing.

The ILHVHR guidelines and business case template seek an options assessment with the following stages:

- identify a range of strategic interventions—described as ‘high-level actions’ that should ’examine a range of capital, service delivery, legislative, and/or market based solutions available’

- establish response options—DTF’s business case guidance describes a response option as ’a combination of interventions that, when packaged together, form a response’ and says, ’The response options should represent a broad coverage and include a focus on changing demand, improving productivity and changing supply’

- assess the response options by evaluating the extent to which options deliver the benefits targeted in the business case together with identifying risks, disbenefits, interdependencies, cost and timeframe. The end result is a ranking of response options and identification of a recommended response option

- assess project options aligned to the preferred response option by undertaking detailed financial, economic, risk and other analysis to arrive at a recommended project solution.

Following this process gives the government confidence that it is selecting the best solution to address the stated problems and benefits targeted in the business case.

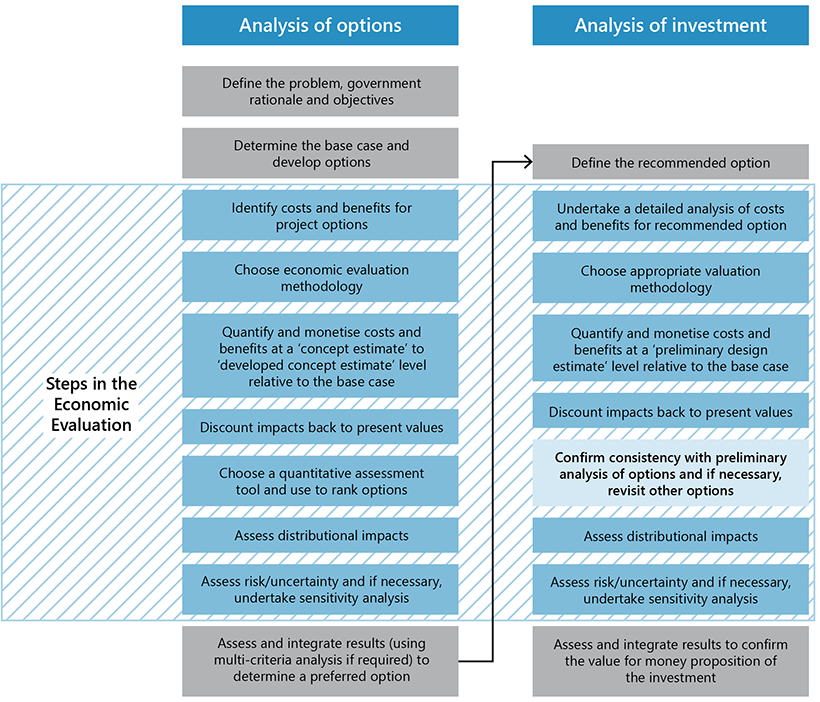

Economic and cost–benefit analysis

The assessment of economic impacts is a key feature of the project options assessment and the business case. It gives the government an understanding that what it funds will provide a net benefit to society.

DTF’s preferred method for assessing economic impacts is through a cost–benefit analysis (CBA). The CBA produces a benefit–cost ratio (BCR) for each project option. The BCR is one indicator of how successfully a project could meet its intended benefits.

Figure 1D summarises the process steps for a CBA.

FIGURE 1D: Steps in a CBA

Source: VAGO, based on DTF’s Economic Evaluation for Business Cases Technical guidelines.

A CBA assigns monetary value to the anticipated impacts or benefits of project options and compares it to the cost of investment. DTF’s ILHVHR requires agencies to monetise benefits in a defensible, neutral manner wherever possible.

Investments are delivered over a number of years and their benefits may not be experienced until after a project is completed. Therefore, monetary values assigned to costs and benefits for the CBA must be calculated and represented as a net present value (NPV).

NPV is the difference between the present value of costs and the present value of benefits over a period of time or appraisal period. DTF advises that the appraisal period should generally be evaluated over the full life cycle of an investment, but this can be difficult for infrastructure projects with a long life cycle like the SRL.

As the appraisal period becomes longer, the integrity of estimates generally declines. ATAP guidelines suggest that a standard appraisal period for road projects is 30 years and for rail projects, 50 years.

The economic analysis will also show a BCR result for project options. A BCR of less than 1.0 indicates the estimated benefits of the investment are less than the estimated costs.

Discount rates

The present-value results in the CBA are calculated by discounting real values.

DTF guidance indicates that the economic evaluation for a business case ‘is used to support informed decision making’ and that ‘discounting is based on the concept of time preference’. That is, the discount rate reflects society’s preferences for incurring costs and obtaining benefits over time. DTF’s guidance defines the time preference of society through a standardised approach to discount rates recommended for business cases based on the nature of the project.

DTF’s Economic Evaluation for Business Cases: Technical Guidelines (August 2013) recommends that business cases for proposed investments in projects use a discount rate of:

- 7 per cent in the CBA for core service delivery areas of government with benefits that are easy to monetise, such as public transport and roads

- 4 per cent in core service delivery areas of government with benefits that can be articulated but are not easily translated to monetary terms, such as schools, hospitals, police stations and civic open spaces.

The guideline also requires projects using a discount rate of 7 per cent to be sensitivity tested using real rates of 4 per cent and 9 per cent.

Standard practice in transport business cases has been to apply a discount rate of 7 per cent with sensitivity tests at 4 and 10 per cent. This matches Infrastructure Australia’s requirements.

DoT’s guideline, The standard approach to transport modelling and economic evaluation in Victoria, 2019–20 (October 2019), acknowledged DTF’s ILHVHR guidance. DoT updated this guidance in December 2020 to require the presentation of economic analysis results under discount rates of both 4 per cent and 7 per cent.

Transport modelling

Transport modelling underpins key components of all transport project business cases. This modelling provides the basis for problem definition, response and project option assessment, and quantification of conventional transport project benefits for the economic analysis.

Non-standard benefits—wider economic benefits and option and non-use benefits

Wider economic benefits (WEBs) relate to economic benefits not typically captured in traditional CBA. They can include ‘agglomeration' impacts expected to arise from an investment, such as an increase in productivity due to improved proximity or access to suppliers and labour markets.

DTF and national guidance state that caution should be exercised when estimating and considering WEBs as part of the economic assessment of projects. The guidance clearly states that the primary results of the economic analysis should be presented without including WEBs and that WEB-inclusive results should be separately disclosed.

Option and non-use benefits are a benefit stream to reflect the value that people who do not use the infrastructure or services provided by the planned investment nevertheless place on their being available. This is not a conventional benefit included in standard transport CBA approaches.

Relevant ATAP guidance suggests that:

- option and non-use value benefits should be quantified and included in the economic appraisal of public transport initiatives that would involve substantial changes in the availability of public transport services serving local communities outside main urban areas

- including option value and, particularly, non-use value benefits creates considerable risks of double counting the direct user benefits already incorporated in a conventional CBA.

1.3 Who is responsible for developing business cases?

Departments and agencies are responsible for developing business cases and can set up their own guidance, tools and resources to complement DTF's ILHVHR guidelines.

Several public sector entities are directly involved in the transport portfolio. Figure 1E outlines their roles and responsibilities for the business case stage.

FIGURE 1E: Agency roles and responsibilities at the business case stage

| Entity | Role | Business case-specific responsibilities |

|---|---|---|

|

DoT |

|

|

|

MTIA |

MTIA is responsible for planning and delivering major transport infrastructure projects. It comprises a number of project offices, including Rail Projects Victoria (RPV) and Major Road Projects Victoria (MRPV), and developed 3 of the 4 business cases examined in this audit. |

Manages the development of business cases for projects under project-specific agreements with DoT |

|

SRLA |

SRLA is a statutory authority established to plan and deliver the SRL program. |

Manages the development of business cases and funding submissions for the SRL program based on a development brief with DoT |

|

DTF |

|

|

|

OPV |

Provides additional technical assurance on business case quality for projects subject to the HVHR project assurance framework |

Undertakes technical and project assurance reviews |

|

DPC

|

Supports the government to achieve its strategic objectives |

|

|

Government |

|

Considers and approves investments and funding |

Source: VAGO, based on information from DoT, MTIA, SRLA, DTF and DPC.

1.4 Assurance framework for major infrastructure projects

The ILHVHR guidelines include a project assurance framework to provide independent and objective oversight of the development, assessment and future performance of major projects.

The HVHR project assurance framework involves:

- DTF and OPV preparing project assurance plans to specify and guide the application of external assurance activities to HVHR projects

- DTF undertaking HVHR reviews at key milestones, including a deliverability assessment on the business case

- Gateway reviews.

HVHR project assurance framework

The government introduced the framework in 2010 to apply more rigorous review and assurance processes to projects meeting defined cost and risk criteria. The framework’s aim is to provide government with more certainty that claimed benefits can be delivered within the timelines and costs estimated by proponents.

In 2010, DTF advised government that the key priorities in introducing the HVHR process were to:

- enforce the requirement for a robust business case with clear project objectives, well-defined benefits, a rigorous appraisal of options, selection of appropriate procurement methods and appropriate governance and management

- clearly articulate a tender proposal, appointment approach and contract management framework that appropriately allocates and manages risk, delivers benefits and effectively manages scope and cost.

Under the HVHR process as originally designed, the Treasurer’s approval was required for HVHR project business cases before they were lodged for funding consideration. This required DTF to complete HVHR deliverability assessments based on final lodged business cases and to brief the Treasurer prior to the government considering these proposals.

The HVHR process has been refined since 2010 with the objective of creating a more efficient and targeted project assurance process. The most recent significant updates to the framework occurred in late 2017, based on advice from DTF. The revised framework requires DTF to include deliverability advice on business cases in briefings to the government, rather than just the Treasurer, on budget submissions.

Irrespective of the refinements to the HVHR process in recent years, the fundamental principle and goal—that DTF should apply additional scrutiny to the business cases for HVHR projects before they are approved and funded by government—remains unchanged. This additional scrutiny should take the form of an HVHR deliverability assessment of the business case by DTF to inform government consideration of the business case.

Gateway reviews

Gateway reviews, which are performed by a team of independent, experienced reviewers engaged by DTF, are done at key points of the HVHR project/program life cycle. They act as both a critical check and balance for government business cases and to provide insights and learnings to assist the investment going forward.

The aim of the Gateway review process is ‘to assist agencies across the Victorian budget sector achieve better capital investment outcomes and to enhance their procurement processes.’

The standard approach for an HVHR project is to step through the 6 Gateway review gates sequentially. The business case review is at Gate 2 of the process.

1.5 Major transport infrastructure project business cases

For this audit, we looked at recently developed business cases and relevant reviews, advice and funding submissions for the following major transport infrastructure projects:

- SRL—a commuter rail network intended to trigger urban renewal in and around station precincts traversing suburbs 15 to 25 km from the CBD along an approximately 90 km route from Cheltenham to Werribee:

- The SRL business case provided to the government in April 2021 referred to ‘SRL East’ as the eastern section of the SRL project between Cheltenham and Melbourne Airport and ‘Stage One’ as the first stage of SRL East between Cheltenham and Box Hill.

- The business case publicly released in August 2021 renamed project sections to SRL East (the section from Cheltenham to Box Hill), SRL North (the section from Box Hill to the Melbourne airport) and SRL West (the section from Melbourne Airport to Werribee).

- In this report we have adopted the current section naming approach of SRL East, SRL North and SRL West. We have changed our descriptions of earlier decisions and events to be consistent with this approach.

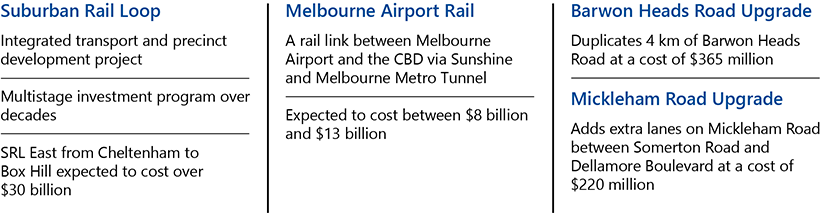

- MAR—12 km of new track from Melbourne Airport to Sunshine Station. MAR will use the Melbourne Metro Tunnel to access Melbourne’s CBD. Expected project cost is between $8 billion and $13 billion ($5 billion was committed by the Australian Government)

- MRU1, which adds extra lanes on Mickleham Road between Somerton Road and Dellamore Boulevard. It also replaces the roundabout at the Somerton Road intersection and upgrades existing (and builds new) walking and cycling paths ($109.5 million is the commitment from the Australian Government)

- BHRU, which duplicates 4 km of Barwon Heads Road from Settlement Road to Reserve Road. The Australian Government contribution is $292 million.

Figure 1F summarises these projects.

FIGURE 1F: Project business cases examined in this report

| Project | Expected start and finish | Total estimated investment |

|---|---|---|

| SRL |

SRL East Expected start 2022 Expected finish 2035 |

SRL East $30.0b to $34.5b |

| SRL North To be determined |

SRL North To be determined |

|

| SRL West Subject to further investigation |

SRL West Subject to further investigation |

|

| MAR | Expected start 2022 Expected finish late 2029 |

$8b–$13b |

| MRU1 | Expected start mid-2023 Expected finish early 2025 |

$220m |

| BHRU | Started 2021 Expected finish late 2023 |

$365m |

Note: b = billion; m = million.

Source: VAGO, based on information from DPC, DTF, DoT, MTIA and SRLA.

Adequacy of Suburban Rail Loop business case

Conclusion

The business case DoT and SRLA provided to the government for the SRL program did not support informed investment decisions. The business case only analysed part of the program and did not fully meet DTF’s guidance requirements.

DTF has provided substantial advice to the government on the SRL program since 2019. However, it is yet to complete the assessment of the business case required under its HVHR project assurance framework to give the government confidence in its deliverability.

This chapter discusses:

2.1 SRL business case development and timing

Figure 2A shows our assessment of the extent to which DoT, SRLA and DTF conformed to the good practice requirements of the ILHVHR guidelines.

FIGURE 2A: Assessment of SRL business case development process and timing

| Process stage | Assessment |

|---|---|

| Business case development and oversight | |

| Development process | A |

| Governance, project management, quality assurance, approval | G |

| Assurance and external review requirements | |

| Project assurance plan | G |

| Gateway reviews | A |

| DTF HVHR assessment of business case deliverability | A |

| Infrastructure Australia review of business case | To be confirmed |

| Timing | |

| Did the business case timing meet DTF’s guidance? | A |

Note: We have used a green (G), amber (A), red (R) scale, where:

G= no or minor departures from relevant guidance and/or expected processes

A = some departures from relevant guidance and/or expected processes

R = significant departures from relevant guidance and/or expected processes.

Source: VAGO.

We judge that DoT and SRLA’s project management, governance, and quality assurance and review processes for the business case were satisfactory because:

- they demonstrated a systematic approach to managing the business case development work streams between 2019 and 2021

- the level of governance is appropriate to its scale and complexity and has covered the development of the business case and funding submissions

- the quality assurance processes included progressive reviews by SRLA, DoT and DTF, and a formal peer review of the transport demand forecasting and economic appraisal underpinning the business case.

In relation to our amber ratings, in summary:

- the approach adopted by DoT and SRLA for assessing the SRL investment program is not consistent with DTF’s ILHVHR guidelines

- DTF did not complete its deliverability assessment of the business case before government funded it, but provided other relevant advice

- the timing of DoT’s business case was much later than the expectations expressed in DTF’s investment life cycle framework and ILHVHR guidelines, but it met the timing set by government.

SRL business case development processes

Government’s decision-making on the SRL program since 2018 has not followed the standard investment development process, where departments first develop a comprehensive business case to inform a government investment decision. Instead, the SRL project development and delivery are progressing in parallel.

DPC, DTF, DoT and SRLA took the view that the SRL is much more than a typical transport project because it includes an unprecedented, city-shaping and multi generational program of integrated transport and precinct development works that required a tailored approach to informing government on the investment, rather than the standard investment development process.

DTF lent support to this by advising us that their view was that the HVHR framework should not be seen as a ‘one size fits all’ approach and needs to be applied flexibly to projects, while maintaining appropriate rigour and confidence. DTF indicated that the need to be agile in applying the framework to fulfil the intent of the assurance task is more prominent in complex, large-scale intergenerational infrastructure projects like SRL.

In response we have assessed whether the tailored approach adopted has met the intent and key required content of DTF’s investment life cycle framework and ILHVHR guidance.

Figure 2B provides a timeline of key events, decisions and announcements relevant to the SRL business case development.

FIGURE 2B: SRL business case key events, decisions and announcements

| Date | Relevant event, decision or announcement |

|---|---|

|

December 2016 |

Infrastructure Victoria releases its first 30-year infrastructure strategy for Victoria. This strategy did not identify a need for or recommend an orbital rail project in Melbourne. |

|

2017 |

DPC commissions a strategic business case for the Orbital Metro project. |

|

October 2017 |

Government releases the Victorian Infrastructure Plan (VIP). This plan does not refer to an Orbital Metro or suburban rail loop project. |

|

January-April 2018 |

Development Victoria completes and government notes the Orbital Metro Strategic Business Case. |

|

August 2018 |

Suburban Rail Loop Strategic Assessment is publicly released. |

|

27 August 2018 |

Government requests DPC to commission a full business case for SRL. |

|

28 August 2018 |

Government announces a commitment to develop a full business case for the SRL if re-elected. |

|

November 2018 |

Victorian state election. |

|

May 2019 |

Government agrees that RPV will prepare an investment case for SRL and allocates $300 million for the business case and early planning works. |

|

June 2019 |

Government approves an approach to the SRL investment case, including a scope covering SRL East and SRL North, and an approach to the economic appraisal. |

|

February 2020 |

SRL East initial works, early works and precinct activation funding submission completed by SRLA. |

|

June 2020 |

Government approves $2.2 billion in funding for initial and early works and the SRL preferred delivery option and delivery program. |

|

December 2020 |

Gateway Gate 1 review on SRL investment case and Gateway combined Gate 1 and Gate 2 business case review on the SRL initial and early works and Stage One main works funding submissions. |

|

February 2021 |

|

|

April 2021 |

Government:

|

|

August 2021 |

SRL Business and Investment Case publicly released. |

|

November |

Government announces funding of $9.3 billion towards major works on SRL East. |

Source: VAGO, based on information from DPC, DTF, DoT and SRLA.

Early development process for SRL business case during 2017 and 2018

The early development of the SRL business case was atypical for the state’s largest ever transport infrastructure project because:

- no transport agencies were involved in the planning and development of the orbital metro line

- the VIP released in October 2017 made no reference to an orbital rail line for Melbourne

- DPC, the agency that commissioned its development, has no record of its decision to do so, or of its review of the business case before it provided it to government in April 2018

- DTF was not involved in its development and did not provide any advice to the Treasurer when the business case was submitted to the Cabinet in April 2018.

In late August 2018 the government:

- released the Suburban Rail Loop Strategic Assessment that examined 3 potential corridors for the SRL (inner, middle and outer Melbourne), recommended a rail line through Melbourne’s middle suburbs and committed to a full business case for the entire project

- requested DPC to engage Development Victoria to lead development of a full business case for the project

- announced its commitment to the SRL project if re-elected and committed $300 million for the development of a full business case for the entire SRL project.

Before the SRLA was set up in September 2019, DPC, DTF, DoT, RPV (a project office of MTIA), Development Victoria and the Department of Jobs, Precincts and Regions continued planning for SRL. These departments and agencies established teams and engaged technical and commercial advisers to develop the business case.

SRL business case approach between 2019 and 2022

DoT and SRLA advised us that in mid-2019, the government endorsed an approach involving:

- a single program-wide investment case, positioning SRL as an orbital rail project from Cheltenham to Werribee, providing integrated analysis to establish the strategic need and consider the program’s transport and precinct development benefits, but focusing principally on the SRL sections from Cheltenham to Melbourne Airport

- the SRL Western section from Melbourne Airport to Werribee to be delivered as part of the MAR and the Western Rail Plan (WRP)

- separate funding submissions to secure the release of funding for individual packages of works, consistent with the investment case, and submitted progressively to align with the program’s delivery timeframes.

This approach indicates SRLA adopted a program-level business case approach, which is accepted under DTF’s ILHVHR guidance. The guidance states that, ‘Programs bring together multiple projects under a single coordinating structure, where each project contributes to the program outcomes'.

The DTF ILHVHR guidelines say that for a program of related investments, the business case approach should involve:

- a preliminary business case for the entire program outlining the program ‘master plan’ and justifying the program logic

- a full business case for the entire program

- separate full business cases for the major projects that form part of the program master plan.

However, DoT and SRLA have not given the government a full business case and economic appraisal for the entire SRL program of investments and none have been requested. They have provided the government submissions for specific components of SRL East and SRL North:

- a funding submission for initial and early works on SRL East in February 2020

- a funding submission for the SRL East main works in February 2021

- the business case for SRL East and SRL North in April 2021.

This approach creates risks that the advice to the government on these investments is not sufficiently comprehensive. This is because the funding submissions for SRL stages have not, and will not, provide any further investment rationale or economic analysis for either the significant individual investments proposed under those submissions or the SRL project as a whole.

The Gateway review of the draft business case in December 2020 raised this risk and stated that:

‘Greater clarity on the scope of all works covered by the investment analysis is needed if it is the intention that future funding submissions do not require a further investment rationale'.

The final SRL business case made it clear that its scope was limited to SRL East and SRL North, but it does not:

- provide an economic appraisal for the entire SRL program

- make it clear that DoT and SRLA do not intend to provide government or the community the economic appraisal results for the entire project or individual stages of the project.

The separate funding submissions for specific components of SRL East so far have detailed the scope, budget and other information relevant to these requests but not an economic appraisal for this project. The other advice from DoT, SRLA, DTF and DPC to the government on these funding submissions has also lacked economic appraisal results for the SRL East component of the SRL program.

External review and assurance on the SRL business case

HVHR projects require a project assurance plan, Gateway reviews and a DTF assessment of the deliverability of the business case before it is funded.

Important steps in DTF’s HVHR project assurance process did not provide sufficient assurance or recommendations on key elements of the SRL business case.

Project assurance plan

DTF established an SRL program assurance framework document by July 2020. This substantively meets the intent of a project assurance plan for the entire SRL program. DTF advised that the Treasurer has also approved project assurance plans for the SRL East initial and early works package and the SRL East main works package.

Gateway reviews

The Gateway reviews of the SRL project business case and funding submission for SRL East main works could have provided greater value to the SRL project team if they had been more comprehensive.

Gateway review teams undertook:

- a Gate 1 (concept and feasibility) review on the SRL investment case, completed on 3 December 2020

- a combined Gate 1 and Gate 2 business case review on the SRL initial and early works and SRL East main works funding submissions, completed on 6 December 2020.

A Gate 1 review is primarily ‘to review the outcomes and objectives of the proposed investment (and the way they fit together)’. In contrast:

‘The key purpose of a combined Gates 1 and 2 review is to confirm that the business case is robust—meets the business need, is affordable, achievable with appropriate options explored, likely to achieve value for money and aligns well with the department’s overall strategy'.

The Gate 1 review of the SRL business case found that the economic appraisal approach diverges from standard guidance on the discount rate used and also that the inclusion of WEBs in primary results was not in line with DTF guidance. However, it is not clear why the reviewers made no recommendations about these matters.

The review team for the combined Gate 1 and Gate 2 business case review of the SRL East main works funding submission acknowledged previous government decisions on the project and tailored its approach to focus on project implementation and governance. As a result, the report on the review did not adequately address key elements of its required scope, including affordability, options assessment and value for money.

HVHR deliverability assessment of the business case

DTF’s deliverability assessments on HVHR project business cases aim to provide confidence to the government that business cases are robust before they are considered for funding.

However, DTF has not yet completed its deliverability assessment of the SRL business case, even though the government approved the SRL business case in April 2021 and has committed funding of over $11 billion to the project and SRLA has commenced procurement for major works packages. In addition, DTF did not do a deliverability assessment on the SRL East initial and early works funding submission that secured funding of $2.2 billion in June 2020.

In June 2022 DTF told us that:

- the information submitted to the government in June 2020 did not have enough detail to enable DTF to complete the HVHR deliverability assessment for SRL East initial and early works

- it was unable to complete the deliverability assessment of the business case before it was approved in April 2021 because DTF required additional information

- it is undertaking a business case deliverability assessment based on the SRL Business and Investment Case, SRL East main works funding submission and other relevant information.

DTF also advised us that it has provided advice to the government on the SRL business case that addresses the substance of the required deliverability assessment. Our review of this advice shows that it did not fully address the scope of a deliverability assessment.

In any case, DTF has:

- provided extensive ongoing advice to the Treasurer on the SRL business case

- reviewed the funding submissions for SRL East initial and early works and main works

- provided ongoing input to SRLA on the business case

- commissioned an independent cost review of the initial and early works packages

- commissioned a review of the cost estimate for the SRL East main works tunnelling package

- plans to undertake reviews of cost estimates for other SRL East work packages

- carried out HVHR reviews on procurements for the project.

DTF has not indicated when it expects to complete the HVHR deliverability assessment for the SRL business case.

SRL business case timing

The business case for SRL East and North was completed in February 2021 and was consistent with earlier government decisions and requests. However, it was too late to inform key government decisions on proceeding with the investment and the project solution and its timing was not consistent with DTF’s investment life cycle framework and ILHVHR guidelines.

The advice provided to inform earlier government decisions on the SRL program did not address gaps and issues with the options and economic assessment we identified in the business case.

2.2 SRL business case content

Figure 2C summarises our assessment of 5 key business case content areas in the ILHVHR guidelines.

FIGURE 2C: Assessment of SRL business case content

| Business case content areas | Assessment |

|---|---|

| Problem definition and evidence | A |

| Case for change (benefits) | A |

| Options assessment | R |

| Economic analysis and presentation of results | R |

| Delivery case | A |

Note: We have used a green (G), amber (A), red (R) scale, where:

G= no or minor departures from relevant guidance and/or expected processes

A = some departures from relevant guidance and/or expected processes

R = significant departures from relevant guidance and/or expected processes.

Source: VAGO.

In summary:

- the high-level problems and benefits articulated in the SRL business case lacked necessary and sufficient supporting evidence

- a narrow set of options were considered and analysed both before and as part of the business case development

- the economic analysis does not cover the entire SRL program and lacks consistency with the guidance in key areas.

Problem definition and evidence

Plan Melbourne 2017–2050 is the metropolitan planning strategy to manage Melbourne’s growth and change over the next 3 decades.

SRL business case describes 3 problems that are consistent with addressing challenges and objectives identified in Plan Melbourne 2017–2050:

- Melbourne’s monocentric form is constraining economic growth.

- Concentration of growth in inner and outer Melbourne is contributing to inefficient infrastructure and service provision.

- Inequitable access to jobs and services is entrenching disadvantage.

The discussion of problems in the business case is consistent with relevant requirements in DTF’s ILHVHR guidance. However, these high-level problems:

- are not supported with comprehensive evidence

- are not supported by detailed descriptions of their root causes or underlying drivers or how they may be impacted by uncertainty

- do not immediately point to the need for a transport-related intervention.

The business case lacks comprehensive evidence on why the problems need to be addressed now by the government. It notes that SRL was an election commitment before the 2018 state election but does not acknowledge that:

- Infrastructure Victoria’s independent 30-year infrastructure strategy released in 2016 did not include or signal a need for an orbital rail line in Melbourne

- the VIP released in October 2017 did not include an orbital rail loop in Melbourne

- no transport or rail plan publicly available in Victoria in 2017 or 2018 identified the need for an orbital rail loop in Melbourne.

The case for change and benefits

The ‘case for change’ section in the SRL business case is not fully consistent with DTF’s ILHVHR guidelines.

The investment logic map included in the business case identifies 3 benefits:

- increase Victoria’s productivity and economic growth

- improve connectivity across Victoria

- improve Melbourne’s liveability and thriving communities.

These benefits are of high value to the government. However, the business case does not:

- clearly identify how the proposed benefits flow from the problems identified

- adequately demonstrate how some of the benefits are a direct consequence of the SRL project

- demonstrate how some of the benefits specifically relate to the key performance indicators identified

- substantively discuss key dependencies critical to benefit delivery and it lacks detail on the degree to which the benefits are dependent on other infrastructure projects.

These issues arise because the business case defined such a high-level set of benefits that they may not be achievable with a single investment or even a major program of investments, such as the SRL.

Option development and assessment

The SRL business case does not meet the DTF ILHVHR guideline requirements because it does not consider a sufficient breadth of strategic interventions for the scope of the problems it describes.

The 2 program options assessed in the business case and supporting economic analysis have the same scope and only differ in their delivery timelines. Given the size and complexity of the SRL project, we expected the business case to examine a wider range of options, including as part of the economic analysis. This would have given the government greater confidence that the recommended program is the best value-for-money solution.

Strategic response options assessment

The narrowness of the options analysis in the business case is not mitigated by earlier advice to government. The Orbital Metro Strategic Business Case (January 2018) and Suburban Rail Loop Strategic Assessment (2018) both lacked a robust assessment of alternative response options:

- The Orbital Metro Strategic Business Case included only a brief assessment of a relatively narrow set of strategic interventions.

- The Suburban Rail Loop Strategic Assessment only considered potential corridors for an orbital rail link.

These assessments identified and assessed an insufficient range of strategic options and they were not packaged into response options. Gaps in the response options assessment in the strategic business case mean that this assessment may not have identified the best way to address the problems and deliver the benefits targeted in the SRL business case.

The fact that neither the SRL business case nor its preceding strategic assessment and strategic business case attempted to package the high-level strategic interventions into response options is inconsistent with the DTF ILHVHR guidance. This omission may have led to an early focus on an orbital metro rail solution rather than exploring a broader set of solutions.

Advice from DTF and SRLA indicates that the government had made a decision on a preferred strategic option when considering the Orbital Metro Strategic Business Case in 2018 and that this removed the need for the SRL business case to review other strategic options. This is concerning, given that:

- evidence provided to us on government consideration of the Orbital Metro Strategic Business Case in April 2018 does not show any decision on a preferred strategic option

- both DTF and DPC have advised us that they can find no evidence that they reviewed the strategic business case or provided any advice to government on its merits and comprehensiveness in meeting DTF’s ILHVHR guidelines.

Project options economically assessed in the business case

The SRL final business case includes an economic appraisal of just 2 program cases compared to a base case:

- Program Case Option A: proposed SRL East and North rail along with select precinct initiatives, with completion scheduled for 2053

- Program Case Option B: rail and precinct initiatives as per Program Case A, with completion scheduled for 2043.

These 2 options have the same scope and only differ in the timing of their delivery. For an investment of this scale, and to meet DTF’s ILHVHR guidance, the economic appraisal should have been used to test a shortlist of substantively different options covering a range of feasible solutions.

Because the business case does not do this, the project options assessment provides little assurance to decision-makers that, from a value-for-money perspective, the best option has been selected to deliver the benefits targeted in the business case.

Economic analysis

The SRL business case provided to government in April 2021 only includes economic analysis of the combined SRL East and North sections and this analysis is not sufficiently comprehensive, robust or transparent.

The business case method and content for the economic analysis are consistent with earlier government decisions but are inconsistent with key elements of the relevant guidance. The business case also does not present the results transparently. It:

- uses a discount rate of 4 per cent, whereas DTF guidance recommends 7 per cent

- does not include the required sensitivity analysis at different discount rates

- includes WEBs and urban consolidation benefits when presenting the primary economic evaluation results

- presents the CBA results as a range, without highlighting that this range incorporates only some of the uncertainties.

These issues increase the likelihood that the business case overstates the economic value of the project.

The business case and economic appraisal report acknowledge and seek to justify these departures from guidance and standard practice. However, the business case does not:

- explain the lack of sensitivity analysis at higher discount rates

- clearly show how these departures from guidance impact the CBA results.

The sensitivity analysis included in the business case is not sufficiently robust or comprehensive because it is unclear how the CBA results would change if assumptions around cost, public transport demand and land-use demand were altered. These are likely to be key areas of uncertainty for the SRL project and should have been explored further as part of the sensitivity analysis.

In addition, the business case and the SRL East main works funding submission do not provide distinct CBA results for the stage from Cheltenham to Box Hill. This failure to report a separate BCR for SRL East is significant because the government was advised to commit to an extended and unprecedented costly investment program without any advice on the expected economic value of only SRL East being completed.

Discount rate

SRLA used a discount rate of 4 per cent for the economic evaluation in the final SRL business case. This discount rate does not align with relevant Victorian or national guidance, which recommend a discount rate of 7 per cent for transport infrastructure projects.

The Minister for Transport Infrastructure approved the use of a 4 per cent discount rate in February 2021, based on advice from DoT and SRLA. The Treasurer accepted this approach in April 2021, 2 months after the business case was completed, based on advice from DTF. The minister and Treasurer did not approve the omission from the business case of sensitivity results using different discount rates.

The business case acknowledges that, ‘Standard approaches require future costs and benefits to be discounted at a real rate of 7 per cent.’ The key rationale presented in the business case for diverging from this approach is that:

‘SRL [is intended] to benefit Victorians for generations to come. Application of the standard 7 per cent discount rate would render almost worthless many of the benefits enjoyed by the intended beneficiaries of SRL East and SRL North'.

The rationale provided in the business case and the advice to the minister and Treasurer supporting the use of 4 per cent do not demonstrate a detailed consideration of the issues to justify this specific discount rate.

In particular, the advice commissioned by SRLA and provided to support the recommendation to the minister does not specifically endorse the use of a 4 per cent discount rate for the SRL business case. It finds that the continued application of a fixed 7 per cent discount rate is inappropriate and proposes a revised methodology for calculating a more appropriate discount rate and that further work and analysis is needed to develop the specific discount rate.

DTF has not changed its technical guidance on discount rates. DoT’s standard approach to transport modelling and economic evaluation in Victoria requires economic appraisals to report CBA results using both 4 and 7 per cent discount rates.

DTF has recently advised that the Australian Government and all states and territories, including Victoria, are undertaking work to review discount rate guidance.

DTF has advised us that it was appropriate to use a 4 per cent discount rate for the SRL program because:

- the project is more than a public transport infrastructure investment because it will enhance Melbourne’s liveability with social and environmental benefits that are not easily monetised and quantified for CBA

- the extended delivery timeline of 30 years and the intergenerational economic and social benefits of the projects mean a 7 per cent discount rate was not appropriate.

These observations may be relevant when considering an appropriate discount rate for the economic appraisal of the entire SRL program. However:

- our review of the economic appraisal in the business case indicates that it quantified around $50 billion of present-value benefits, including conventional transport benefits, transport emission environmental benefits, WEBs and reduced social exclusion benefits, and did not suggest that there are material levels of non-monetised benefits

- suggesting that projects with longer-life benefits should have a lower discount rate is not consistent with the accepted purpose of applying a discount rate, which is to reflect the community preference for costs and benefits over time.

In addition, DoT and SRLA have no intention to provide government with a business case or other advice that includes an economic assessment covering the entire SRL program. They have justified the use of 4 per cent with reference to it being the only rate appropriate for an assessment of the full costs and benefits of the full project scope, but this analysis of the full project scope may never be done. The SRL East section funded to date is intended for completion in just over 10 years.

Presentation of primary economic appraisal results

The business case is not consistent with DTF guidance because it presents the economic appraisal results as a range and only shows BCR and NPV results with WEBs and urban consolidation benefits included together with what the business case describes as ‘conventional benefits’.

Non-standard benefits in primary results

Including WEBs and urban consolidation benefits when presenting the primary CBA results is not consistent with DTF guidance that states, ’WEB inclusive results should therefore be presented separately from the standard Net Present Value or Benefit–Cost Ratio results’. DoT guidance also reinforces this requirement.

The SRL business case lacks transparency and is not sufficiently comprehensive because it does not explain how this departure from guidance impacts on the results.