Local Government Assets: Asset Management and Compliance

Overview

At 30 June 2018, the 79 Victorian councils controlled $102.1 billion in assets and infrastructure, including land, roads, buildings, drains, footpaths and bridges. Our previous audits of councils' asset management practices over the past 15 years have identified persistent weaknesses in their asset management. Councils require accurate asset information to comply with state and federal disaster response programs—if their asset management programs are noncompliant, they risk being unable to access funding.

In this audit, we assessed whether local councils accurately document infrastructure assets in their information systems and use this data in their asset management and planning.

We audited five councils: Colac Otway Shire, Nillumbik Shire Council, City of Darebin, Hindmarsh Shire Council and Mildura Rural City Council.

We made seven recommendations to Victorian councils to support improvements in their asset information management and use.

Transmittal Letter

Independent assurance report to Parliament

Ordered to be published

VICTORIAN GOVERNMENT PRINTER May 2019

PP No 25, Session 2018–19

President

Legislative Council

Parliament House

Melbourne

Speaker

Legislative Assembly

Parliament House

Melbourne

Dear Presiding Officers

Under the provisions of section 16AB of the Audit Act 1994, I transmit my report Local Government Assets: Asset Management and Compliance.

Yours faithfully

Andrew Greaves

Auditor-General

23 May 2019

Acronyms

| AIMS | asset information management system |

| ALGA | Australian Local Government Association |

| AMAF | Asset Management Accountability Framework |

| AMP | asset management plan |

| DELWP | Department of Environment, Land, Water and Planning |

| DRFA | Disaster Recovery Funding Arrangements |

| DTF | Department of Treasury and Finance |

| IIMM | International Infrastructure Management Manual |

| ISO | International Organization for Standardization |

| LG Act | Local Government Act 1989 |

| LGPMC | Local Government and Planning Ministers' Council |

| LGV | Local Government Victoria |

| MAV | Municipal Association of Victoria |

| NAMAF | National Asset Management Assessment Framework |

| NDRRA | Natural Disaster Relief and Recovery Arrangements |

| RM Act | Road Management Act 2004 |

| SAMP | Strategic Asset Management Plan |

| VAGO | Victorian Auditor-General's Office |

| VGC | Victoria Grants Commission |

Audit summary

One way in which local councils deliver services to the community is through effective use of their assets. Council assets include roads, bridges, footpaths, drains, libraries, town halls, parks, recreational centres, and other community facilities. The 79 Victorian councils control more than $102.1 billion in assets and infrastructure, including more than $26.5 billion in roads and bridges and $8.7 billion in drains.

To ensure they realise full value from these assets, councils need to effectively plan for, manage, and utilise them. Effective management of these assets requires the collection of appropriate information, including their value, cost to maintain and operate, condition, performance, risk and utilisation. Councils should then use this information to make decisions about their assets. These asset management decisions include how and when to invest in new assets, as well as decisions about maintenance, replacement, upgrades, and disposals.

This audit assessed whether local councils accurately document infrastructure assets in their information systems and use this information in their asset management and planning.

The audit focused on five local councils:

- Colac Otway Shire Council (Colac Otway)

- Darebin City Council (Darebin)

- Hindmarsh Shire Council (Hindmarsh)

- Mildura Rural City Council (Mildura)

- Nillumbik Shire Council (Nillumbik).

Conclusion

The audited councils do not have enough comprehensive and accurate information to support asset planning, and they do not make enough use of the information that they have. Although they maintain basic data about their assets—such as location and description—councils do not always supplement this with asset maintenance and failure data. This reduces their ability to identify poor performing assets and to justify new asset investments.

Councils use some asset information to support asset planning and decision-making, however, this is not consistent across all asset classes and councils. For example, all audited councils have and use better information about their roads than other asset classes, largely due to their obligations under the Road Management Act 2004 (RM Act).

Complex and unintegrated asset information management systems (AIMS) compound the information gaps, which make it difficult for staff to find the asset information they need to support decision-making. This means asset decisions depend heavily on the experience and judgement of individual staff without the benefit of objective data.

Findings

Managing asset information

Asset management policy, governance, and roles

All audited councils have governance arrangements for asset information management within their asset management policies, although Darebin and Colac Otway could improve this by clarifying roles and responsibilities. In an example of better practice, Nillumbik has a data framework that outlines the information the council will collect against each type of asset. Mildura is developing similar guidelines.

Identifying asset information needs

None of the audited councils have comprehensively documented their asset information needs. However, all audited councils have asset management plans (AMP)—either final or draft—that identify and prioritise asset information needs for roads and related infrastructure—such as traffic control signs and street lights.

|

Essential safety measures are the features of public buildings that ensure the safety of occupants, such as fire doors, alarm systems, fire extinguishers and emergency lighting. |

Councils need to identify and document their legal obligations about asset information to ensure that they collect the right type of information. Colac Otway, Mildura and Nillumbik have done this—their AMPs refer to relevant regulatory and statutory requirements. In contrast, Hindmarsh has not fully documented its obligations and Darebin has only noted its legal obligations about roads information.

Except Nillumbik, the audited councils keep information about essential safety measures and asbestos registers separate from their standard AIMS. Not keeping this information in a central and accessible location makes it difficult for council staff to find and update the information when they need to.

None of the audited councils have identified the asset information they need to support claims for funding under the Disaster Recovery Funding Arrangements (DRFA). As a result, councils risk not having the right information to satisfy claims for funding in the event of a natural disaster.

|

Under the Disaster Recovery Funding Arrangements, the Australian Government can give funding to state and local governments after a natural disaster to repair assets. To satisfy claims for this funding, councils need information about the pre-disaster function and condition of assets. |

Information management processes

Documenting new assets

Nillumbik, Hindmarsh and Mildura have documented processes for recording new asset information. In contrast, Colac Otway and Darebin advise that they sometimes record information about new assets as they find them, for example during condition inspections.

Asset handover occurs when teams within a council transfer responsibility for an asset, such as when a new asset transfers from the construction team to the team responsible for operating the asset. Ineffective asset handover processes can affect data quality. For example, Colac Otway advised that during fire and flood recovery work, its asset handover process failed—the council acquired new assets but did not record them in its AIMS. This means the council's asset information was not complete and up-to-date at that time.

Asset maintenance and failure information

The maintenance and failure history of an asset helps councils to predict the likelihood of future failures or performance issues. None of the audited councils have documented processes to capture this information and, as a result, have missed opportunities to use maintenance data to inform decisions about operational and capital planning. For example, councils do not record the cost of maintenance works against specific road assets. This means they can only access the overall cost of their road maintenance program and cannot analyse the cost of maintaining each road.

Similarly, except for Darebin, the audited councils link maintenance data to buildings, rather than to component assets—such as air conditioner units or generators. This means councils must use an overall average of a building's condition to predict future maintenance and renewal costs. This is ineffective, as component assets may require renewal or replacement at different times.

Accuracy and completeness of asset information

We asked councils to self-assess the completeness of their asset information as well as their confidence in it. We then tested the assessments by reviewing a sample of asset records from roads, stormwater and building asset classes.

Based on this process, Nillumbik has the highest completeness across all asset classes, with an average completeness of 89 per cent, compared with an average of 41 per cent across the remaining audited councils. The audited councils have a greater proportion of complete data on their road and related assets—an average of 67 per cent across the councils—than other asset classes.

Councils need to be confident that their asset information is accurate and complete, so that they can use it to make evidence-based decisions. Except Nillumbik, the audited councils had low confidence that their asset information was accurate and complete. The audited councils had more confidence in their roads data than in their other asset classes—they had high confidence in the information for 45 per cent of their road assets. In contrast, the audited councils had high confidence in only 25 per cent of building assets, 20 per cent of drains, bridges and culverts and 18 per cent of recreation assets—such as sporting fields, playgrounds, and trees.

Nillumbik had higher confidence in its recreational asset information because it had identified and documented these assets in its Reserves Asset Management Plan.

Asset information management systems

AIMS are software applications for capturing, managing and analysing asset information. Ideally, a council's AIMS should comprise a small number of integrated core software products.

Except Mildura, the audited councils have complex AIMS and use multiple software applications to manage their asset information, which are not well integrated. In addition, Hindmarsh and Colac Otway have limited documentation on how to use or manage their applications. This can lead to council staff manually transferring data from one application to another, resulting in inefficiencies and potential errors.

In 2014, Mildura purchased and began implementing a new AIMS. The system represents better practice in that it links to the council's customer relationship management system, geographic information systems and, through a manual export process, its finance system. Although it requires further effort to fully implement and transfer information into the system, the council has established a project control group to oversee implementation and progressively improve the system.

Using asset information

Capital and operational planning

Relying on staff judgement to make decisions about assets—rather than asset information and documented processes—creates a risk that councils will not make evidence-based decisions. Darebin, Hindmarsh and Mildura rely heavily on council staff experience when making asset management decisions, and do not always document these decisions.

None of the audited councils have sufficient documentation on capital planning processes to adequately support evidence-based asset management for all asset classes, and over the asset lifecycle. Nillumbik, Mildura and Darebin are applying some processes to use asset data and information to inform capital plans, especially relating to roads and related infrastructure and drainage.

Similarly, none of the audited councils have sufficiently documented their operational planning processes, although Colac Otway and Hindmarsh use some maintenance and operational cost data to inform operational plans and budgets. The other three councils—Nillumbik, Mildura, and Darebin—only use previous historical maintenance costs for developing their annual maintenance budgets. These councils have recognised a gap in their processes and advise they are working on projects to rectify the issue.

Using asset risk

None of the audited councils consistently use risk information in their decision-making across all asset classes, though all use more risk information when planning for road and drainage assets.

Audited councils do not have formal processes for assessing which assets are critical or important to service delivery, which would help them prioritise investment and works activities. Despite a lack of processes, all audited councils except Colac Otway use risk assessment to identify critical drains.

Asset management capability and resources

None of the audited councils' resource capability plans identify a need for skills in analysing asset information. In addition, none have established clear roles and responsibilities for the use of asset information in asset planning and decision-making. Without this, councils cannot be sure they have the skills available to use asset information to support decision-making about assets.

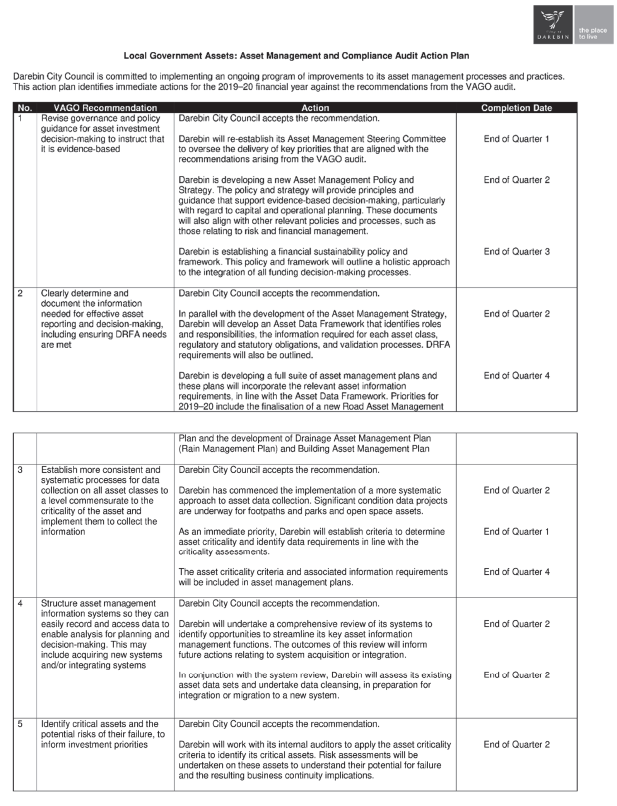

Recommendations

We recommend that Victorian councils:

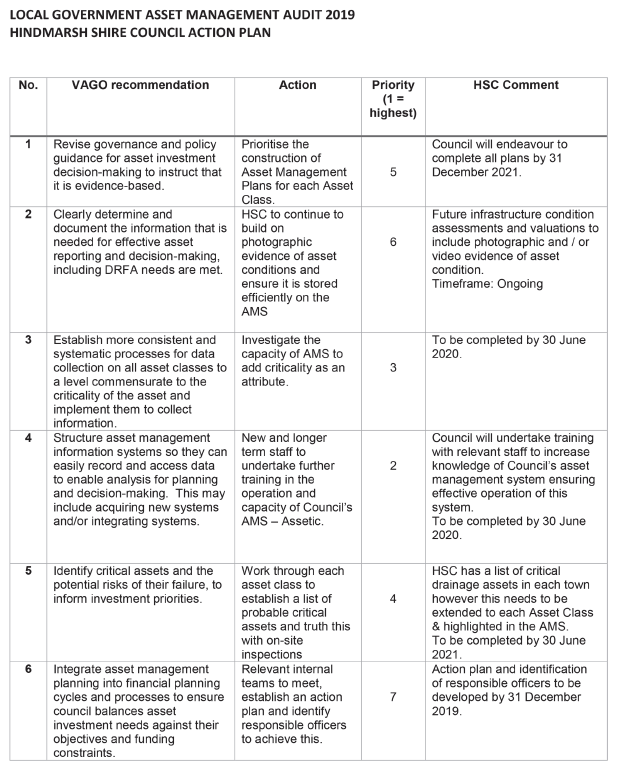

1. revise their governance and policy guidance for asset investment decision-making to ensure that it is evidence-based (see Section 3.2)

2. clearly determine and document the information that they need for effective asset reporting and decision-making, including ensuring Disaster Recovery Funding Arrangements needs are met (see Section 2.3)

3. establish more consistent and systematic processes for data collection on all asset classes to a level commensurate to the criticality of the asset and implement them to collect the information (see Section 2.4)

4. integrate asset management information systems so staff can easily record and access data to enable analysis for planning and decision-making (see Section 2.6)

5. identify their critical assets, and the potential risks of their failure, to inform investment priorities (see Section 3.4)

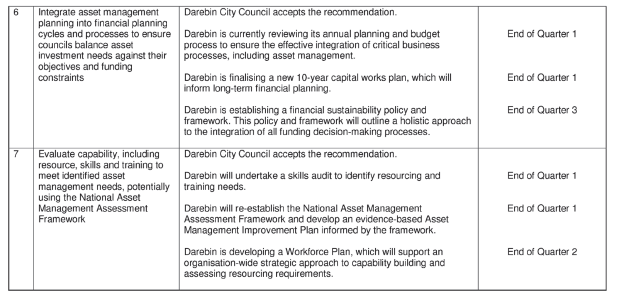

6. integrate asset management planning into financial planning cycles and processes to ensure councils balance asset investment needs against their objectives and funding constraints (see Section 3.3)

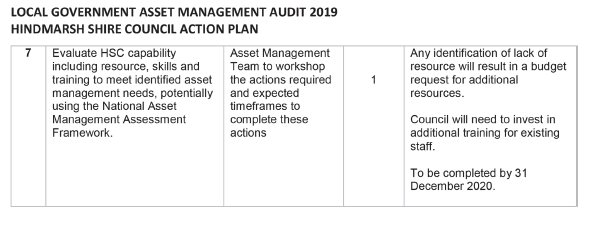

7. evaluate their capability, including resource, skills and training to meet their identified asset management needs, potentially using the National Asset Management Assessment Framework (see Section 3.2 and Section 3.5).

Responses to recommendations

We have consulted with the audited councils and we considered their views when reaching our audit conclusions. As required by section 16(3) of the Audit Act 1994, we gave a draft copy of this report to the councils and asked for their submissions or comments. We also provided a copy of the report to the Department of Premier and Cabinet.

All audited councils have accepted the recommendations from this audit. Councils' full responses are included in Appendix A.

1 Audit context

1.1 Background

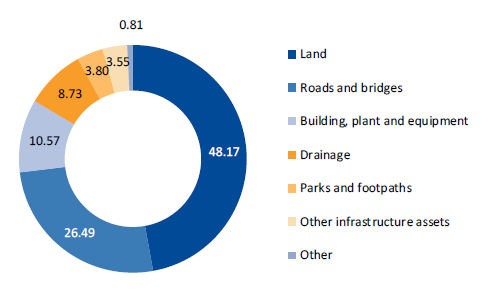

One way in which local councils deliver services to the community is through effective use of their assets. Council assets typically include roads, bridges, footpaths, drains, libraries, town halls and recreational centres, and may include other specialised facilities such as airports and landfills. The 79 Victorian councils control more than $102.1 billion in assets and infrastructure, including more than $26.5 billion in roads and bridges and $8.7 billion in drains, as shown in Figure 1A.

Figure 1A

Victorian local government assets ($ billions), 2017–18

Note: 'Other infrastructure assets' includes works in progress, waste management, recreational facilities, aerodromes, and car parks.

Note: 'Other' includes investment property and other intangible and financial assets.

Source: VAGO, based on council annual reports.

To ensure they realise maximum value from their assets, councils need to manage and utilise them effectively. Asset management is the systematic process that guides the planning, acquisition, operations, maintenance, and eventual replacement or disposal of assets. Its purpose is to ensure councils' assets allow them to deliver services that meet community standards and needs efficiently, while managing risks.

Effective asset management includes collecting appropriate information and using it to make decisions on planning and managing assets. The types of information for councils to collect include asset value, cost to operate and maintain, condition, maintenance, performance, risk, and utilisation.

1.2 Roles and responsibilities

Multiple government agencies and associations provide information and guidance to the local government sector to support councils' asset management activities.

Local Government Victoria

Local Government Victoria (LGV)—a division of the Department of Environment, Land, Water and Planning (DELWP)—provides advice and support to councils to improve their business and governance practices, including asset management. Its objectives include the development and implementation of evidence-based policy and projects that strengthen councils' capacity to meet the needs of Victorian communities.

Guidelines released to support better asset management practice include:

- Local Government Asset Management: Better Practice Guide (2015)

- Good Practice Guide for Asset Protection Permits in Local Government (2013)

- Local Government Asset Investment Guidelines (2006)

- Guidelines for Measuring and Reporting the Condition of Road Assets (2006)

- Guidelines for Developing an Asset Management Policy, Strategy and Plan (2004)

- Sustaining Local Assets: Local Government Asset Management Policy Statement (2003).

Municipal Association of Victoria

The Municipal Association of Victoria (MAV) runs the STEP Asset Management and Financial Sustainability Program, which it has designed to help councils improve their asset management processes with support from asset management consultants. The STEP program uses the National Asset Management Assessment Framework (NAMAF) (discussed in 1.4) as a basis for assessing councils' asset management performance.

Victoria Grants Commission

Victoria Grants Commission (VGC), supported by DELWP, allocates financial assistance grants from the Australian Government to Victorian councils.

It collects data on a range of asset-related matters, including capital assets and outlays, valuations, and road inventory expenditure.

1.3 Legislation

Section 140(2) of the Local Government Act 1989 (LG Act) requires councils to ensure they have adequate control over their assets. Further, section 136 of the LG Act requires councils to manage their financial risks prudently, having regard to economic circumstances, including the management and maintenance of assets. Unlike the Financial Management Act 1994, which does not apply to councils, there is no explicit obligation under the LG Act for councils to maintain an asset register.

The previous government introduced the Local Government Bill 2018 in the Parliament in May 2018. If enacted, it would have replaced the current LG Act. The Bill proposed a requirement for a 10‐year AMP as well as a 10‐year financial plan and a four‐year budget. These changes aimed to encourage councils to consider short, medium, and longer‐term approaches to asset management and resource planning. In the lead up to the 2018 state election, the Bill lapsed, leaving the LG Act as the legal framework for Victorian local government.

A range of applicable legislation covers aspects concerning council-owned assets. Some of these include:

- Road Management Act 2004—local roads are one of the most significant asset classes that councils own, representing more than a quarter of the total value of Victorian council assets. Under the RM Act, councils must maintain a register of all public roads for which they are the coordinating road authority.

- Occupational Health and Safety Act 2004—promotes improved standards for occupational health, safety, and welfare. It places obligations on councils to provide a safe working environment for their employees and to ensure that councils maintain their plant and equipment in a manner that is safe and fit for purpose.

- Building Regulations 2018—as owners of public buildings, councils must keep records of maintenance checks, service and repair works for essential safety measures (such as fire alarms and emergency lighting).

1.4 Frameworks and guidance

Councils can access guidance on asset management and asset information from a range of sources.

National Asset Management Assessment Framework

Since 2010, Victorian councils have self-assessed against NAMAF, developed by the Australian Centre of Excellence for Local Government. The NAMAF consists of 11 key asset management elements, including councils' asset data and systems.

Asset Management Accountability Framework

The Department of Treasury and Finance's (DTF) Asset Management Accountability Framework (AMAF)—applicable to Victorian Government agencies—outlines requirements over four key stages of the asset management lifecycle, from planning, acquisition, operation, and maintenance, to disposal.

The AMAF, although not compulsory for Victorian councils, provides useful guidance on how councils can manage their asset information. The AMAF sets out that agencies must maintain asset information—both financial and non- financial—to support asset planning, and performance monitoring and reporting.

ISO 55000 Asset Management

The International Organization for Standardization's ISO 55000:2014 Asset Management (ISO 55000) provides a global guide to better practice in asset management, including asset information management.

ISO 55000 specifies that entities should align information requirements to asset management needs and risks, along with requirements for collecting, managing, evaluating, and ensuring consistency and availability of information for asset management decision-making.

ISO 55000 identifies several requirements for sound asset information. These are summarised in Figure 1B.

Figure 1B

Elements of sound asset information

|

Element |

Description |

|---|---|

|

Information governance |

Define roles and responsibilities for managing asset information and processes to ensure asset information is suitable to achieve council objectives. |

|

Information requirements |

Identify the asset information needed to support:

Better practice is to capture this in a strategy, including actions to improve the asset information over time. |

|

Information management |

Formalise processes for managing asset information. The processes should ensure that information is available and suitable for councils' needs. They will describe how councils collect, analyse and evaluate information. Asset information should have appropriate coverage and accuracy, and be consistent with other data held by councils. |

|

Information systems |

Ensure capability to store, manage, access, analyse and share information for asset management, planning and decision-making purposes. Councils make continual improvements for ongoing adequacy and effectiveness. |

Source: VAGO, based on ISO 55001:2014.

Institute of Public Works Engineering Australasia

The Institute of Public Works Engineering Australasia has released materials since 1994 designed to support asset management processes and AMP development. These materials, which provide guidance on asset management information and its use in planning, include:

- International Infrastructure Management Manual (IIMM)

- Australian Infrastructure Financial Management Manual.

1.5 Using asset information

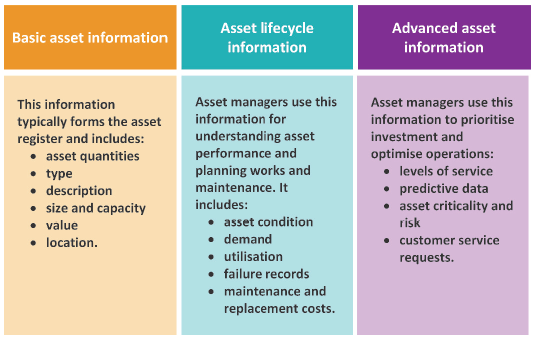

There are three key types of asset information, as shown in Figure 1C.

Figure 1C

Types of asset information

Source: VAGO.

Asset management and planning

Asset information, including the asset's condition, is essential to support a range of important council decisions. Councils should use their asset information in developing their long-term strategic and financial plans.

A 2016 Queensland Audit Office report found that, due to inaccurate and incomplete asset condition data, councils were undertaking asset renewals in an unstructured and reactive manner. The report noted that this limited their understanding of the level at which to set council rates and charges and how to optimise the life of the assets.

Similarly, a 2017 report by the Controller and Auditor-General of New Zealand highlighted that high-quality asset information improved councils' longer-term planning.

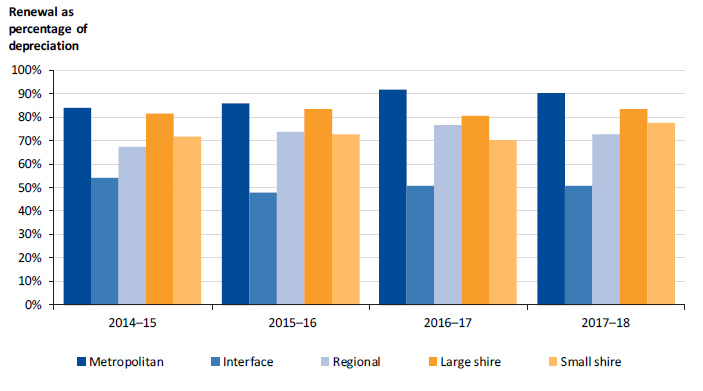

Figure 1D shows the Victorian local government sector's renewal gap—the difference between what a council spends on renewing, restoring or replacing existing assets and its depreciation costs—over the past four years.

Figure 1D

Asset renewal expenditure as percentage of depreciation, 2014–15 to 2017–18

Source: VAGO, based on LGV Local Government Performance Reporting Framework.

|

Interface councils refers to a group of 10 municipalities that form a ring around metropolitan Melbourne. |

Due to considerable population growth, interface councils spend a much larger proportion of their budget on new assets compared with the other council cohorts, and less on asset renewal. Interface councils have the lowest ratio of asset renewals, at about 50 per cent, while metropolitan councils have improved in the past few years.

Natural disasters and asset information

The Australian Government provides funding to the states and territories for up to 75 per cent of their relief and recovery costs following a natural disaster.

Councils can receive financial support for costs associated with the restoration and replacement of essential public assets such as roads and bridges, public hospitals, schools, local government offices and stormwater infrastructure that are a direct result of damages due to a natural disaster.

On 1 November 2018, the DRFA replaced the former Natural Disaster Relief and Recovery Arrangements (NDRRA). Councils can submit claims for reimbursement to DTF, which administers the arrangements in Victoria.

Under the DRFA, the Australian Government will give funding only to restore an asset to its pre-disaster function. This means that if a natural disaster destroys an asset, the Australian Government will not cover the cost of improving it. The DRFA sets out the Essential Public Asset Function Framework, which state and local governments must use to decide the pre-disaster function of assets.

Under the DRFA, to make a claim for reimbursement for the restoration or replacement of an essential public asset, state and local governments must be able to provide supporting evidence of the pre-disaster condition and function of their assets. This needs comprehensive and up-to-date asset information management. Examples of this include asset information for condition, asset maintenance, and visual and geospatial data.

Councils also must prepare and maintain Municipal Emergency Management Plans under the Emergency Management Act 1986. Under this legislation, councils play a role in the provision of relief and recovery services and in supporting emergency response operations. Reliable asset information is important for implementing Municipal Emergency Management Plans.

Funding asset management

Under the LG Act, councils have the power to levy rates and charges to fund and deliver essential community infrastructure and services. The delivery of many of these services depends on asset performance.

Fair Go Rates System

In 2015, the Victorian Government introduced the Fair Go Rates System, which enables the Minister for Local Government to establish a yearly rate cap that limits councils' ability to increase their rates and municipal charges each year. This acts as a constraint on how councils have previously raised revenue. To increase rates beyond the cap, councils must apply to the Essential Services Commission.

Under section 185E of the LG Act, councils applying for a higher cap must demonstrate a range of factors, including:

- how councils have considered the views of ratepayers and the community in proposing the higher cap

- how the higher cap is an efficient use of council resources and is value for money

- whether the council has considered re-prioritising proposed expenditure and alternative funding options and why those options are not adequate.

The Essential Services Commission has advised that councils seeking a higher rate cap must establish a long‐term funding need. The council needs to demonstrate this through a rigorous approach to long‐term financial planning, which can include:

- service reviews—service planning and service prioritisation—leading to affordable services and service levels, informed by community engagement

- asset management planning that identifies cost‐effective outlays and is based on properly considered and documented risk-management practices

- rigorous and well‐documented financial strategies and practices.

Under the Fair Go Rates System, a key challenge for councils is to become more efficient while continuing to deliver services, maintain infrastructure, and renew assets that meet the needs of their communities.

The effectiveness of asset management processes, the quality and appropriateness of AIMS data and integration with council planning process are key elements to addressing this challenge.

Strategic and financial planning

The current LG Act requires councils to develop strategic and financial plans, including:

- a four‐year council plan that outlines the council's strategic objectives and strategies for achieving these

- a four‐year strategic resource plan that details the resources needed to achieve the council's strategic objectives

- an annual budget that outlines how the council will deliver specific services and initiatives.

The quality of these plans is heavily dependent on the maturity of a council's asset management processes, and the quality of their asset information.

Councils should integrate asset management and planning with their strategic and financial planning processes. Ideally, the AMPs for essential infrastructure asset classes should outline the current asset management strategy, use asset information to detail current condition and risk, and make funding recommendations for both capital requirements and operational programs.

1.6 Why this audit is important

Our audits of councils' asset management practices over the past 15 years have found persistent weaknesses and recommended that councils improve their asset management frameworks and their related policies, strategies, and plans.

Our 2014 audit Asset Management and Maintenance by Councils found problems with councils' asset management frameworks and strategies, and that asset management information systems at councils were underdeveloped.

More recently, results of our 2016–17 financial audits of local government show that councils are experiencing a gradual decline in asset renewal and maintenance indicators and are forecasting reduced spending in this area.

We also found issues with councils' asset information management practice. In 2016–17, 29 councils identified $175.3 million in found assets—assets that they had not known about or previously recorded. Assets that are not recorded are not subject to regular maintenance and may continue to deteriorate, resulting in considerable long-term costs. We found that although councils have improved their asset registers through technological advances, including global positioning systems, councils need further work to reduce the number of found assets across the sector.

1.7 What this audit examined and how

In this audit, we looked at whether councils have comprehensive and accurate information about assets and whether councils use asset information to support effective evidence-based asset management and planning.

We did not look at large specialised assets—such as airports and landfills—as these are generally operated as separate business units and council asset teams do not manage them.

We audited a mix of councils to provide a view across the state and across council categories, as shown in Figure 1E.

Figure 1E

Audited councils and council categories

|

Audited Council |

Council category |

|---|---|

|

Colac Otway |

Large shire |

|

Darebin |

Metropolitan |

|

Hindmarsh |

Small shire |

|

Mildura |

Regional city |

|

Nillumbik |

Interface |

Source: VAGO.

The methods we adopted for this audit included:

- discussions and formal interviews with staff at audited councils

- assessment of councils' asset management systems and processes

- assessment of the comprehensiveness and accuracy of the asset data

- testing of actual council assets and plans against council asset registers and other asset data

- case studies of asset information management practices at the audited councils.

The audit did not undertake a full review of councils' NAMAF self-assessments. However, we did test whether councils have accurately assessed themselves in areas that this audit examined, as discussed in section 3.5.

Audit assessment tools

Drawing on available better practice material, we developed a tool to assess councils' asset management practices against a scale of asset management maturity. We initially assessed councils in a one-day workshop with council staff, and agreed on scores against the maturity scale. We later adjusted these scores based on documentary evidence that the councils provided. This formed the basis of our audit findings, a summary of which is available in Appendix B.

We also developed a tool to assess the completeness of councils' asset information, as well their confidence in it. Councils self-assessed this using our tool. We then moderated these results based on further documentation and by reviewing a sample of assets and asset records. Section 2.5 outlines the results of this assessment.

We conducted our audit in accordance with section 15 of the Audit Act 1994 and the Australian Auditing and Assurance Standards. The cost of this audit was $320 000.

1.8 Report structure

This report is set out as follows:

- Part 2 examines the information councils collect and maintain about their assets.

- Part 3 examines how councils use that information to support effective evidence-based asset management and planning.

2 Managing asset information

Comprehensive and accurate asset information enables councils to make informed decisions about their assets—for example, decisions about maintaining, renewing, and replacing assets.

2.1 Conclusion

The audited councils do not have enough comprehensive and accurate information to understand asset performance and enable evidence-based decision-making. Although they maintain basic data about their assets—such as location and description—councils do not always supplement this with asset maintenance and failure data. This reduces their ability to identify poor performing assets and justify new asset investments.

The audited councils collect more detailed asset information where there is a legal requirement to do so—for example, all audited councils have better information about their roads than other asset classes, due to obligations under the RM Act.

Except for Mildura, the audited councils store their asset information across a range of partially integrated systems, making it difficult for staff to access and manage information. This further reduces the ability of decision-makers to find and use asset information to support decision-making.

2.2 Asset information governance arrangements

Governance arrangements for asset information should:

- identify roles and responsibilities for capturing, managing and maintaining all asset information

- establish procedures to ensure the council collects, maintains and manages all information efficiently.

All audited councils have governance arrangements for asset information management within their asset management policies.

Nillumbik, Mildura and Hindmarsh outline more specific and clear roles and responsibilities for asset information—for example, responsibility for assuring the quality of the information—in position descriptions or in AMPs. This detail improves staff accountability for managing asset information.

|

The data owner has ultimate responsibility for the data. The data custodian is the person with the delegated authority from the data owner to approve the use and access of the data. |

Mildura and Colac Otway have asset management steering groups with defined roles and responsibilities, such as responsibility for monitoring asset management. This arrangement provides better coordination of asset information requirements.

However, no audited council has clearly nominated data owners and data custodians. Darebin, Colac Otway and Hindmarsh advise that they see asset data control and assurance as the responsibility of the assets team. However, by not documenting roles and responsibilities, there is a risk that council staff across the organisation do not know who is accountable for data quality, use and security.

Guidelines and frameworks

Data guidelines or frameworks help councils standardise data collection and maintenance to ensure consistency.

In an example of better practice, Nillumbik has a data framework that outlines the information the council will collect against each type of asset. Mildura is developing similar guidelines.

2.3 Identifying asset information needs

The more information councils have about their assets, the more evidence they have to support decision-making on asset maintenance, renewal and replacement. However, not all assets require the same level of information—critical, riskier and higher-cost assets, such as bridges and roads, require more information. Councils should identify the level of asset information they need to support management and decision-making, and to meet legal requirements.

None of the audited councils have comprehensively documented all their asset information needs. However, all audited councils have AMPs—either final or draft—that identify and prioritise asset information needs for roads and related infrastructure.

Legal requirements for asset information

As outlined in section 1.3, councils have a range of legal obligations about how they manage their asset information. Councils need to identify and document these obligations in their AMPs to ensure that they collect the right type of information. Colac Otway, Mildura and Nillumbik have done this—their AMPs refer to relevant regulatory and statutory requirements. In contrast, Hindmarsh has not fully documented its obligations in AMPs, and Darebin has only noted its legal obligations about roads information.

Road management information

Under the RM Act, councils must maintain a register of all public roads for which they are the coordinating road authority, however, they can choose whether to develop a formal road management plan that sets out its system for maintaining and repairing roads. We found that all audited councils keep a register and a road management plan.

Due to these obligations, councils have better asset information about roads than other asset classes, and are better at using roads data in planning and decision-making. We discuss this further in Sections 2.5 and 3.3 of this report.

Essential safety measures

Councils, as owners of public buildings, must keep records of maintenance checks and service and repair works for essential safety measures, such as fire doors and alarm systems. Except Nillumbik, the audited councils keep information about essential safety measures separate to their standard AIMS. By keeping this information across multiple locations, councils create a risk that staff will be unable to find and update the information.

In contrast, Nillumbik addresses this risk by transferring information from its essential safety measures and asbestos audits—including compliance status and inspection dates—into its AIMS. It also has a documented procedure for essential safety measure audits, which also assigns responsibilities for monitoring compliance.

Asbestos registers

Under the Occupational Health and Safety Regulations 2017, anyone who controls a building or workplace where asbestos has been identified must maintain a register which notes the location and type of asbestos as well as any workplace activities likely to disturb it.

All audited councils have asbestos registers. Mildura maintains asbestos registers but does not include this information in its general asset register.

Disaster Recovery Funding Arrangements

None of the audited councils refer to the DRFA in their AMPs. This includes Colac Otway, which received financial assistance through the federal government's previous disaster relief program, the NDRRA. This creates a risk that councils may fail to collect appropriate information about their assets and may not be able to satisfy claims for financial assistance.

2.4 Asset information management processes

To ensure that asset information is accurate and consistent, councils need to document their processes for capturing, maintaining and improving asset information, rather than rely solely on staff expertise and knowledge.

Capturing new assets

|

Asset handover is the process of transferring the responsibility for maintaining and managing a new asset from the staff that constructed it to the staff that will be responsible for its ongoing management. |

To maintain comprehensive asset information, councils need to capture and record information about the new assets they acquire. Councils should do this at the point of asset handover.

Nillumbik, Hindmarsh and Mildura have formal processes for capturing new asset information as part of the asset handover process. In an example of better practice, Nillumbik captures this information through an online process. Hindmarsh advised that it is in the initial stages of improving their process by implementing an asset handover form.

In contrast, Colac Otway and Darebin do not have established processes for documenting new assets during asset handover. Both councils advise that they do not have established processes for finding assets. If they find assets during condition inspections they typically record the assets. Processes such as these are ineffective, as they create a risk that councils will fail to record information about new assets. For example, Colac Otway advised that during fire and flood recovery work, its asset handover process failed—the council acquired new assets, but did not record them in the council's AIMS. This means the council's asset information was not complete and up-to-date at that time.

Colac Otway and Darebin advise they are now planning improvements to their asset handover processes.

Asset maintenance and failure data

Understanding the maintenance and failure history of an asset helps councils to predict the likelihood of future failures or performance issues. This allows councils to identify and plan preventive maintenance on assets to avoid failure.

The audited councils do not have adequate processes to capture detailed asset maintenance and failure information. This reduces their ability to analyse and make informed decisions for operational and capital planning. All audited councils—except Hindmarsh—have documented improvement actions to remedy this.

Roads and related assets

|

Intervention level refers to the lowest condition level of an asset that a council will allow; that is, the point in the asset's life that the council has decided is appropriate for renewal or replacement. |

By value, roads, bridges, and related infrastructure represent 26 per cent of council assets in Victoria. As a result, councils devote a significant proportion of their asset maintenance activities to roads. The road management plans at each council provide well-documented maintenance performance criteria and intervention levels.

Asset teams at the audited councils do not always receive feedback from the staff who complete maintenance works and do not record the cost of the works against specific road assets. As a result, while councils can access the overall cost of their road maintenance program in their finance systems, they cannot analyse the cost of maintaining each road. This lack of detail reduces councils' ability to compare the cost of maintaining a road with the value it provides to the community.

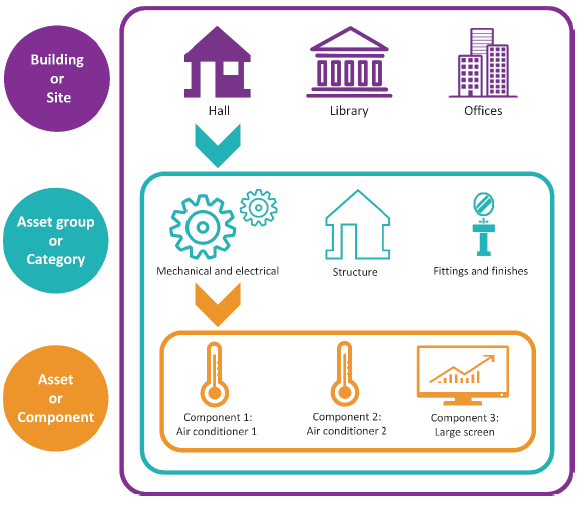

Buildings assets

Building, plant and equipment assets represent 10 per cent of the value of Victorian council assets. Although a building can be considered as a single asset, it also comprises asset categories—such as electrical equipment—and many component assets—such as coolrooms, bathroom fixtures and switchboards. Each of these component assets have specific maintenance needs, risks and costs. Figure 2A outlines the relationship between component assets and buildings.

Figure 2A

Building assets

Source: VAGO.

Four of the audited councils assign work orders—tasks necessary to fix an issue—to the building, rather than to the relevant component asset. In addition, three audited councils—Colac Otway, Nillumbik and Mildura—do not separate planned and reactive maintenance, and combine the maintenance and operational costs into one account or work order for the building.

As a result, most councils do not have the information they need to make decisions about maintaining and improving buildings. For example, without information linked to component assets, councils must use an overall average of building condition to predict future renewal costs. This is ineffective, as different component assets may require renewal or replacement at different times. In addition, if councils want to understand the maintenance and failure history of a particular component asset, their staff need to review all work orders for that building.

Darebin has started to assign planned tasks to building component assets and, as a result, it can access planned contractor and material costs for these components. If the council continues to do this, it will improve the quality and usefulness of the building asset information.

Reviewing asset information

To ensure asset information is accurate and complete, councils need to review, validate, correct and continuously improve it.

Of the audited councils, only two—Nillumbik and Mildura—have adequate processes for validating asset data. Colac Otway and Darebin do not have adequate processes, while Hindmarsh relies on contractors to conduct their own quality assurance processes when collecting data. As a result, these councils cannot assure themselves that they are collecting and using accurate asset information.

In an example of better practice, Nillumbik's asset data framework—discussed in Figure 2B—sets out processes for reviewing and validating data.

Figure 2B

Nillumbik's asset data framework

|

Nillumbik has established asset data control and assurance processes to ensure that the information it collects is accurate and meets the council's information needs. The council uses error scripting—a computer program that automatically checks data within a system for consistency—to validate its asset information on drains. This program highlights missing or inaccurate data and notifies the asset manager. The asset manager then sends the data back to the responsible person to correct any errors. The council has also documented its procedures for receiving asset information from contractor reports. For example, one procedure details how to check and clean data from contractor condition reports. In addition, the council rates its asset information by self-assessing its availability and completeness. This provides the council with a higher confidence level in their data. |

Source: VAGO, based on information from Nillumbik.

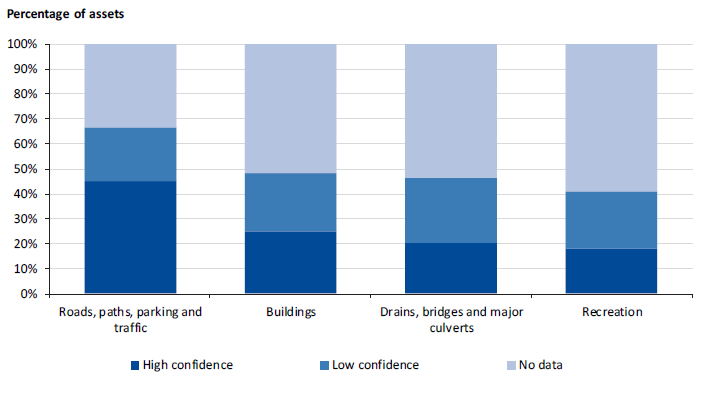

2.5 Accuracy and completeness of asset information

Completeness of asset information

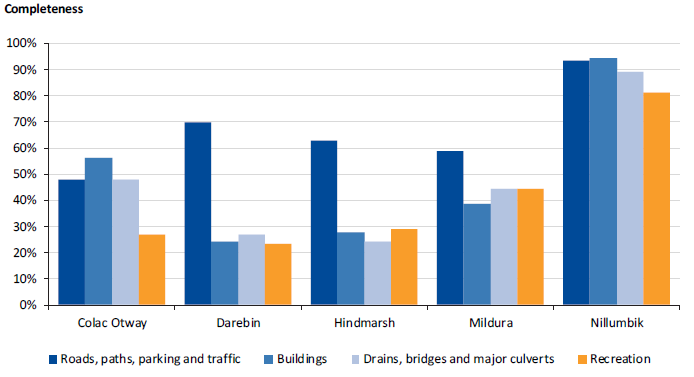

We found Nillumbik had the highest completeness across all asset classes, with an average completeness of 89 per cent. As shown in Figure 2C, councils have more data on their road and related assets—an average of 67 per cent—than on other asset classes.

Figure 2C

Comparison of asset data completeness by asset class

Note: This self-assessment considers the councils' confidence in the data they collect at the building or asset category level.

Source: VAGO, based on audited councils' data.

Confidence in asset information

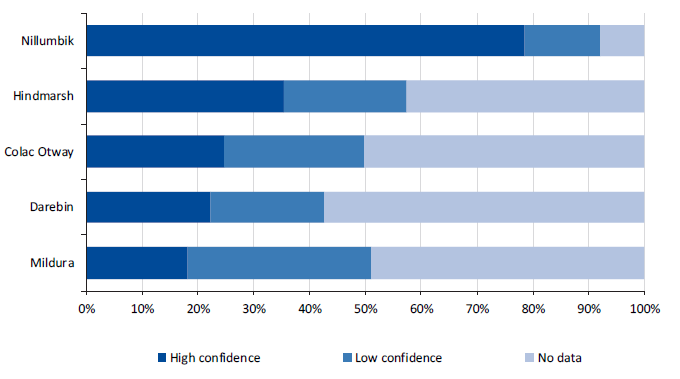

Councils need to be confident that their asset information is accurate and complete, so that they can use it to make evidence-based decisions.

Except Nillumbik, the audited councils had low confidence that their asset information was accurate and complete. As shown in Figure 2D, Nillumbik had high confidence in 79 per cent of its asset information.

Figure 2D

Council confidence in accuracy and completeness of asset information

Note: 'High confidence' means available data is based on reliable information systems, records and procedures, with minor shortcomings only. 'Low confidence' means data is unconfirmed or based on cursory analysis. 'No data' means the council lacked information about the assets.

Note: Assets are weighted by estimated value.

Source: VAGO, based on audited councils' data.

The audited councils had more confidence in their roads data than in their other asset classes, as shown in Figure 2E. As discussed in section 2.3, this is due to councils' obligations under the RM Act.

Figure 2E

Average data confidence by asset class

Note: Assets weighted by estimated value.

Source: VAGO, based on audited councils' data.

Except for Nillumbik, audited councils had low confidence that they had accurate and complete data for parks and recreation assets—such as sporting fields, playgrounds and trees. Nillumbik had higher confidence in this type of data because it had identified and documented these assets in its Reserves Asset Management Plan.

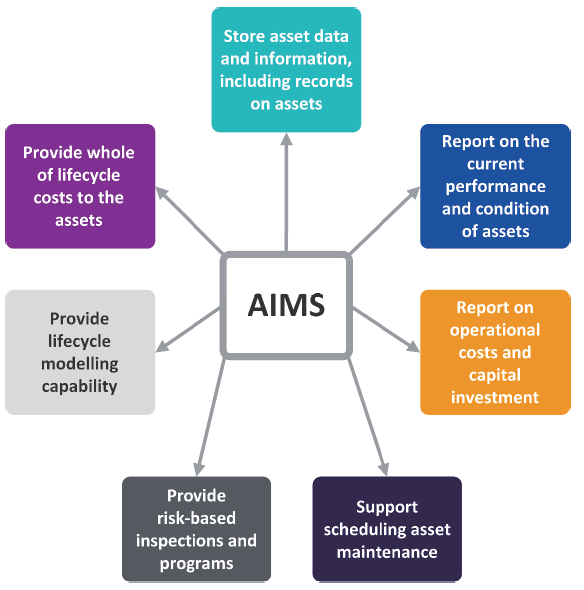

2.6 Asset information management systems

An AIMS is a software solution for capturing, managing and analysing asset information. Councils need to select an AIMS that meets their needs, scale of operations and available resources. To best support asset information management, including using it to support decision-making, an AIMS should integrate the functions outlined in Figure 2F.

Figure 2F

AIMS functions

Source: VAGO, based on DTF's AMAF.

To allow councils to effectively maintain and use their asset information, all software applications that form a part of councils' AIMS should be well integrated.

Except Mildura, the audited councils use multiple software applications, but these are not well integrated. In addition, Hindmarsh and Colac Otway have limited documentation on how to use or manage their applications. This often leads to manual data entry, resulting in inefficiencies and potential for error.

In 2017, Nillumbik hired a consultant to review its asset information management applications. The consultant highlighted that the council had procured and implemented its various applications over time, creating a complex network of asset information management. They also found that the council had not documented the links between these applications and instead relied on staff knowledge of how the applications worked together. Nillumbik advised that, in response to the consultant's findings, it has developed a plan to prepare and implement a new AIMS over the next three years.

As outlined in Figure 2G, Mildura has purchased a single AIMS to meet its asset information management needs.

Figure 2G

Mildura's asset information management system

|

In 2014, Mildura purchased and began implementing a new AIMS. The system links to the council's customer relationship management system, geographic information systems and—through a manual export process—its finance system. Although it has not done so yet, Mildura advises that it plans to enter data about all asset classes into the AIMS. To date, it has entered roads data and work orders and has recently started to enter parks and recreation data. The council has also not yet used the AIMS's cost modelling capability, which would allow the council to forecast future asset costs based on available asset information. The council has established an AIMS project control group to oversee implementation of the AIMS. The group maintains a register of improvement tasks and issues, including software issues to address with the vendor. This helps the council to ensure the AIMS meets the council's needs. Mildura advises that the AIMS has led to improvements in asset information and better management of work orders. |

Source: VAGO, based on information from Mildura.

3 Using asset information

Councils should use the asset information available to them to inform their asset planning and decision-making, including decisions on acquiring, replacing or renewing assets and ongoing maintenance activities.

3.1 Conclusion

More asset information is available to the audited councils than they use. Although they use some of the information available to them for asset planning and decision-making—for example, information about road condition and use—this is not consistent across all asset classes. Councils depend heavily on staff experience and judgement for decision-making, without properly supporting this with objective data.

There is also room for improvement in how councils use risk to identify critical assets and prioritise maintenance and investment. Although the audited councils use risk-analysis for their road and drainage assets, they should use it across all asset classes to ensure that decisions about assets are evidence-based and best meet councils' objectives.

3.2 Asset management governance

Effective asset management and planning governance arrangements should include:

- an asset management policy that aligns with other council policies such as risk and financial management

- asset management plans across all asset classes

- documented roles and responsibilities for asset planning, covering short, medium, and long-term timeframes for both capital and operational projects

- assurance processes to confirm that asset planning outputs—such as strategies, plans and budgets—are evidence-based and support decision-making

- resource capability plans that outline the resources, skills and training necessary for the council to analyse and use asset information.

Asset management plans

AMPs document how a council plans to manage its assets to deliver an agreed standard of service and meet community needs.

Nillumbik and Mildura have AMPs covering all asset classes, including roads, buildings, and drainage.

In contrast, Colac Otway, Darebin and Hindmarsh do not have AMPs for all asset classes and have multiple AMPs in draft format. Darebin previously had AMPs for buildings and drainage, but the council did not finalise them.

Although the audited councils' AMPs are useful—they record the overall condition and age profile of asset classes—there is room for improvement. Except Nillumbik, audited councils' AMPS do not inform or align with capital and operating budgets. For example, Hindmarsh's general AMP does not clearly address service requirements or outline which asset information to use to support decision-making. A 2018 internal review of one of Darebin's AMPs highlighted that it was not aligned to the council's long-term financial plan.

Policies and guidance

We found that the audited councils have some high-level policies and guidance for asset management planning. However, these policies do not establish how to use asset information in asset planning and decision-making. The focus of existing council guidance is on budgeting and accounting processes—such as when to consider asset expenditure as a capital or operational expense.

In examples of better practice, Mildura and Nillumbik have multiple documents to guide asset management decisions. Notably, Nillumbik has an asset lifecycle policy that outlines the council's principles for accounting and reporting on assets.

Capability and resources

None of the audited councils' resource capability plans identify a need for skills in analysing asset information. Without this, councils cannot be sure they have the skills available to use asset information to support decision-making about assets.

Nillumbik engaged a consultant to review its asset management processes, which also highlighted this as an issue. Nillumbik advised that it is in the process of addressing this by reviewing current staff resourcing levels and skill sets to develop workforce plans.

Roles and responsibilities

Audited councils have not established clear roles and responsibilities for the use of asset information in asset planning and decision-making. Colac Otway and Mildura have recognised this gap. They advise that they plan to outline roles and responsibilities for all phases of the asset lifecycle—including decision-making—in future asset management strategies.

In response to findings from an external review, Nillumbik has also begun addressing this issue. Its AMPs now include functional roles and responsibility matrices for asset information use and asset planning. Hindmarsh's position descriptions include planning responsibilities. Darebin and Mildura advise that they are currently revising position descriptions, however, their asset frameworks do not articulate roles and responsibilities.

3.3 Asset planning and decision-making

Using asset information to support decision-making—as well as ongoing capital and operational planning—helps councils to:

- respond to community needs

- address areas of higher risk to the council

- share information to make decisions in a consistent way

- allocate funding to maximise benefit.

Capital planning

Capital planning covers the decisions councils make about the creation of new assets, or renewal or replacement of existing assets. Councils should document their processes for making these decisions and support them with asset information—such as performance, condition, utilisation, and maintenance history.

All the audited councils have used asset information to support capital planning decisions, however, this is not done consistently across asset classes. For example, Hindmarsh uses road condition surveys to support decision-making for roads, but for other classes its renewal targets are based on a percentage of depreciation costs.

Darebin also uses asset information to support capital planning for roads, but does not do so consistently for other asset classes. However, it does use capital works program guidelines and a submission form that sets evaluation criteria for capital projects. Similarly, in 2015, Nillumbik developed a framework that set evaluation criteria for capital projects. However, this was not finalised due to restructures at the council. Setting criteria for capital projects encourages councils to use and analyse asset information. For example, because of its framework, Nillumbik used traffic volume to prioritise future road works, and data on flooding to select capital projects for drainage.

Mildura uses project briefs to support bids for capital projects, however, these do not consistently rely on the council's available asset information. For example, the project brief for a street renewal did not consider the condition of the road asset or traffic count data.

In late 2018, Colac Otway began using a new software tool that generates replacement and renewal programs using asset condition data. Although this represents a good use of asset information, the council could improve this further by using population growth and service level data to ensure capital planning decisions meet community need.

Operational planning

Operational planning covers the day-to-day use and maintenance of assets. Councils should use asset performance, condition, failure, maintenance and cost information to inform their operational plans and budgets for assets.

Not all audited councils consistently use asset information to inform operational plans and budgets. In an example of better practice, Colac Otway and Hindmarsh have both documented processes for using asset information to inform operational plans. Colac Otway also has an operational budget manual to support the asset management system.

Nillumbik uses previous inspection budgets to plan for operational costs, however, it does not review maintenance or failure history to inform maintenance planning. Darebin documents planned maintenance tasks using actual costs, but does not use this to inform operational plans or budgets. Mildura uses some historic asset cost information in its operational budgets, however, its staff advise they have low confidence in their cost estimates. All audited councils document intervention levels for road assets, but do not document their rationale, or whether they align with asset information.

As a result, councils are missing an opportunity to support decisions about how they allocate finite council resources.

Relying on staff judgement

Relying heavily on staff judgement to make decisions about assets—rather than informing decisions through asset information and documented processes—creates a risk that councils will not make decisions that best meet their objectives. It reduces councils' ability to defend decisions and ensure they are using resources efficiently to maximise value for their community.

Darebin, Hindmarsh and Mildura rely heavily on council staff experience when making asset management decisions and do not always document these decisions. For example, Darebin upgraded a drainage asset based on the asset team's view of the maintenance team's capability and capacity to do the required work, rather than information about the condition and use of the asset. The council did not document this decision.

3.4 Asset risk informing investment decisions

A key piece of asset information that councils should use to inform decisions about assets is the risk or criticality of an asset. Incorporating risk management into asset planning and decisions ensures that councils:

- direct limited resources to areas and projects of greater importance

- reduce the risk of assets being unable to support service delivery, or of being inefficient or detrimental to the community's health and safety

- consider risk, cost, and performance to prioritise or optimise investment decisions.

None of the audited councils consistently uses risk information in their decision-making across all asset classes.

Audited councils do consider some risks for roads and drainage assets. All councils rate the risk of roads using information about their function and capacity. Nillumbik has also done so for footpath and trails—it assesses usage data to rate footpaths and trails as high, medium, or low-risk, and uses this to drive maintenance and capital works.

Except Colac Otway, the audited councils have all used flood-monitoring programs to identify which drainage assets are critical to the council.

In an example of better practice, Mildura has mapped its drainage assets in a geographical information system, using colours to indicate risk levels. Similarly, Hindmarsh has identified critical drains and, as a result, increased inspections on those assets. Nillumbik has also mapped and colour-coded its asbestos piping based on risk levels and uses risk assessment to plan inspections for drainage systems, as discussed in Figure 3A.

Figure 3A

Nillumbik's risk-based approach to decision-making

|

Nillumbik uses a risk-based approach to prioritise camera inspections for its underground drainage systems. From this process, the council found that its pipes were in an excellent condition. It found that only a small proportion required work and it was able to complete localised renewal—such replacing pipe segments—rather than replace whole pipe lengths. Similarly, the council identified where cleaning or maintenance works would return pipes to their required service level. Nillumbik advise that this reduced the potential cost of pipe inspections for the council. |

Source: VAGO, based on information from Nillumbik.

In their AMPs, Darebin and Colac Otway refer to risk-management frameworks and document their risk assessments across asset class. However, they have not used asset information to explain or quantify these risks. As a result, these high-level risk assessments do not support AMPs.

3.5 Comparison of audit findings with NAMAF

We reviewed the results of the audited councils' 2017 NAMAF self-assessments in terms of asset information and compared them with our own findings.

We found that Colac Otway and Darebin's 2017 self-assessments—both showing low maturity—accurately reflect our findings. Darebin's 2017 self-assessment differed greatly from its result in 2016, when it assessed its asset management as excellent—the highest rating available. This difference was partly due to new staff, who gave a more critical assessment score.

Nillumbik assessed its asset management as having excellent maturity, even in advanced competencies. This aligns with our findings, as we found the council has the documents NAMAF outlines as necessary for good asset management. However, NAMAF does not consider the quality of councils' asset information or how they use it for decision-making. This is an area for improvement for all audited councils, including Nillumbik.

NAMAF self-assessment scores for Mildura and Hindmarsh were also high. This does not align with our audit findings. This is because the assessments assumed that councils would finalise the draft documents and activities that were in progress at the time of the assessment, which did not always occur. These councils also scored highly on the basis of documents that, although finalised, council staff did not use.

This highlights limitations in the NAMAF questionnaire, which asks councils about their documents, but does not give as much focus to whether councils effectively implement them. Despite this, councils can still use NAMAF to ensure they have the right documents and policies to support good asset management.

Appendix A. Audit Act 1994 section 16—submissions and comments

We have consulted with Colac Otway, Darebin, Hindmarsh, Mildura, Nillumbik and we considered their views when reaching our audit conclusions. As required by section 16(3) of the Audit Act 1994, we gave a draft copy of this report, or relevant extracts, to those agencies and asked for their submissions and comments. We also provided a copy of the report to the Department of Premier and Cabinet.

Responsibility for the accuracy, fairness and balance of those comments rests solely with the agency head.

Responses were received as follows:

- Colac Otway

- Darebin

- Hindmarsh

- Mildura

- Nillumbik

RESPONSE provided by the Mayor, Colac Otway shire

RESPONSE provided by the Chief Executive Officer, Darebin City Council

RESPONSE provided by the Chief Executive Officer, Hindmarsh Shire Council

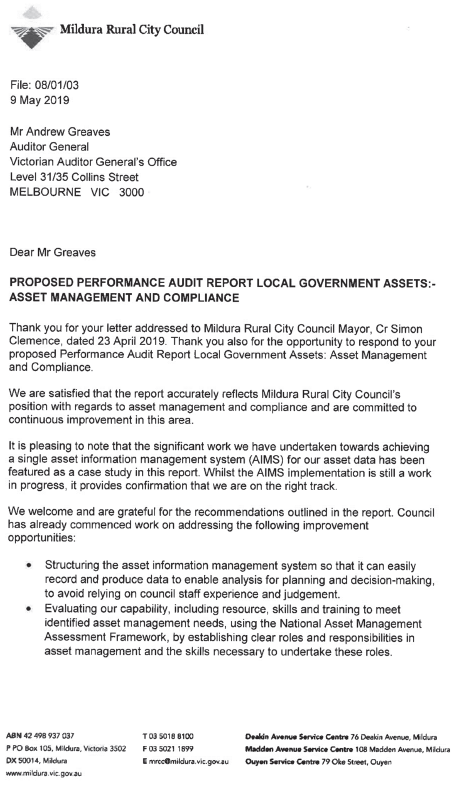

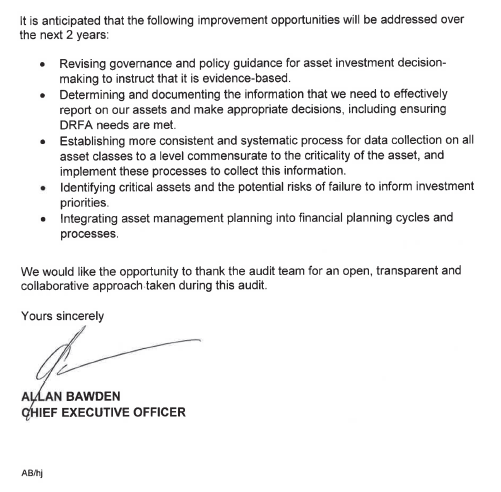

RESPONSE provided by the Chief Executive Officer, Mildura Rural City Council

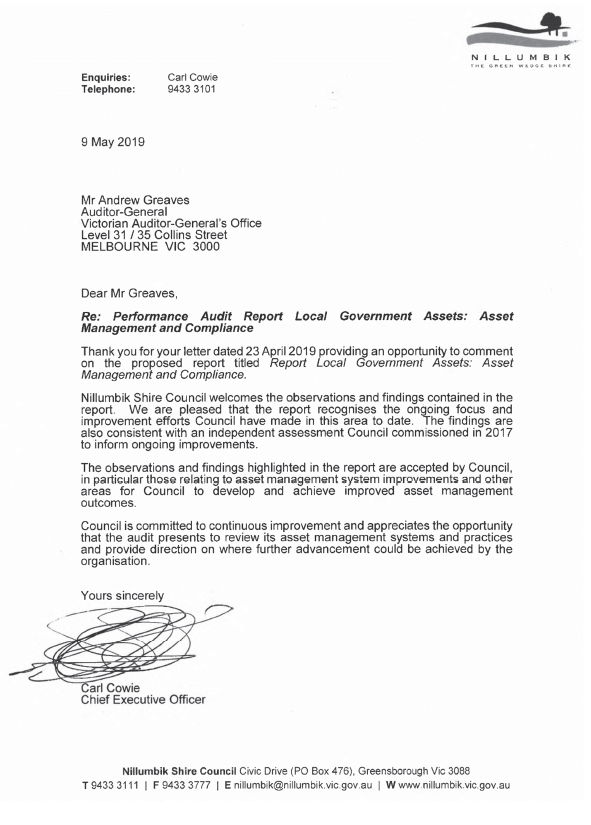

RESPONSE provided by the Chief Executive Officer, Nillumbik Shire Council

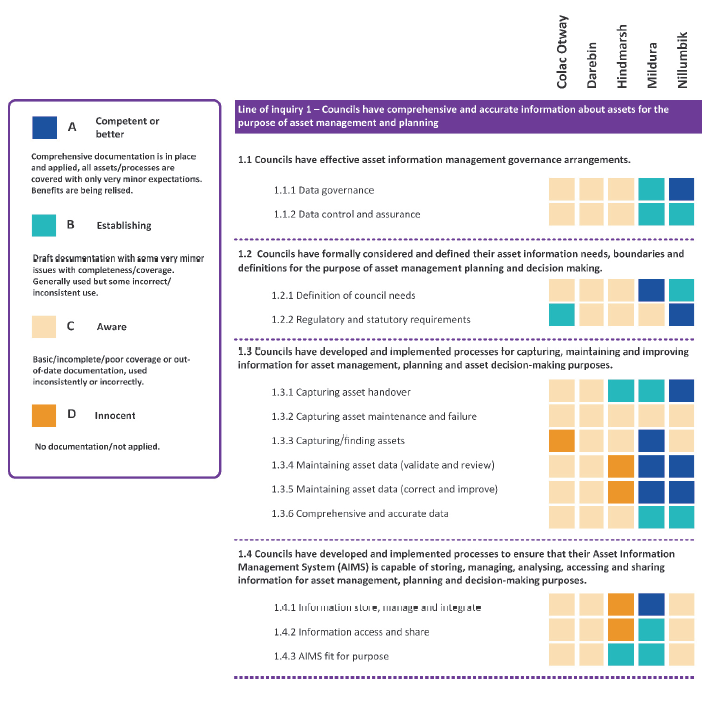

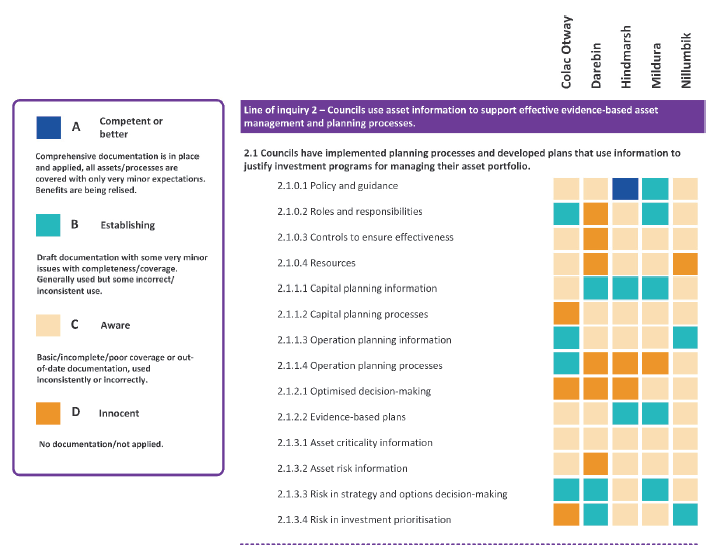

Appendix B. Maturity assessments

Figure B1 compares the results of our maturity assessment across the audited councils.

Figure B1

Maturity assessment results