Performance Reporting by Local Government

Overview

Councils invest significant resources each year in the delivery of a range of services to their communities. Effective performance reporting is essential for assuring councils are accountable to local residents and ratepayers, and for demonstrating value-for-money, achievement of objectives and the delivery of good quality services. Our 2008 audit of Performance Reporting in Local Government found that, for most councils, reporting had limited relevance to ratepayers because it lacked information about outcomes, achievement of objectives and service quality.

This audit assessed the effectiveness of existing local government reporting arrangements and the adequacy of associated reform initiatives. It found that council performance reporting remains inadequate, focused on inputs and operating activities, thereby offering little insight into the impact of services and the achievement of objectives. Some improvements were evident since 2008, but reporting has not sufficiently progressed to satisfy the information needs of residents and ratepayers, or drive continuous improvement within councils. Ongoing performance challenges in the sector indicate that work on a statewide performance reporting framework should continue.

Performance Reporting by Local Government: Message

Ordered to be printed

VICTORIAN GOVERNMENT PRINTER April 2012

PP No 126, Session 2010–12

President

Legislative Council

Parliament House

Melbourne

Speaker

Legislative Assembly

Parliament House

Melbourne

Dear Presiding Officers

Under the provisions of section 16AB of the Audit Act 1994, I transmit my report on the audit Performance Reporting by Local Government.

Yours faithfully

![]()

D D R PEARSON

Auditor-General

18 April 2012

Audit summary

Introduction

Councils invest significant resources each year in the delivery of a range of services to their communities. The Local Government Act 1989 (the Act) requires them to use these resources effectively and efficiently by implementing sound financial management, and to provide their services in line with the best value principles to meet the needs of their local community.

Effective performance reporting by councils is essential for assuring they are accountable to local residents and ratepayers. It provides the opportunity to demonstrate value-for-money, the achievement of objectives, and that equitable access is provided to appropriate, cost-effective and good quality services.

Key changes to the Act in 2003 introduced important reforms designed to improve councils’ accountability through more transparent performance reporting. These included the requirement to disclose, within annual reports, progress against strategic objectives set out in four-year council plans, and the results for key strategic activities identified within annual budgets.

Our 2008 audit Performance Reporting in Local Government examined how well councils had implemented these reforms. It found that, for most councils, reporting had limited relevance for ratepayers because it lacked information about the quality of council services, the outcomes being achieved, and how these related to councils’ strategic objectives. The audit recommended councils critically review and improve their performance information. Our 2008 guide Local Government Performance Reporting: Turning Principles into Practice was subsequently produced to assist councils to achieve this.

This audit assessed the effectiveness of existing local government performance reporting arrangements, and the adequacy of statewide initiatives to reform local government performance reporting.

Conclusions

Performance reporting by councils remains inadequate. It is focused on inputs and operating activities, and offers little insight into the impact of services and the achievement of objectives.

While some improvements were evident at councils since 2008, the progress to date has not been sufficient to satisfy the information needs of residents and ratepayers, to drive continuous improvement, or to deliver timely performance reporting.

These shortcomings continue to impair accountability for performance and represent major obstacles to effectively addressing recurring performance deficiencies at councils.

Ongoing performance challenges in the sector strongly indicate that significant further work towards an appropriate local government performance reporting framework is warranted.

The Report on Government Services (RoGS), produced by a Productivity Commission Secretariat for the Steering Committee for the Review of Government Services, is a mature model that demonstrates the feasibility of reporting common benchmarks and metrics across disparate jurisdictions. This model offers an opportunity to expedite addressing the longstanding challenge of performance reporting in the sector by building on an authoritative and established approach.

Findings

Recurring performance challenges in the sector

A review of the Victorian Auditor-General’s performance audits of local government between 2000 and 2011 reveals a range of ongoing performance challenges for councils.

Specifically, a meta-analysis of 16 performance audits identified the recurring themes of:

- ineffective planning and budgeting

- inadequate implementation of initiatives and adherence to policies and procedures

- weak oversight and monitoring of council activities and outcomes

- inadequate attention to addressing persistent performance issues.

These recurring issues are, in part, a by-product of a lack of accountability for performance due to weaknesses in performance monitoring and related information. Feedback from councils indicates that they are also influenced by ongoing resource constraints, the administrative burden of complying with state and Commonwealth funding and reporting requirements, and by the difficulty of attracting and retaining skilled staff, particularly in regional and rural areas.

These issues typically manifest themselves in:

- poor asset management

- poor financial management and investment decisions

- poor planning enforcement policies and practices

- poor procurement policies and practices

- inadequate business continuity planning

- lack of service reviews.

These challenges have persisted over several years and in various council functions. Deficiencies in the quality and availability of relevant performance information to managers and councillors have impeded their capacity to take appropriate and timely corrective action.

Additionally, the average annual percentage increase in council rates exceeded both the Local Government Cost Index and the Consumer Price Index between 2000 and 2010. While it is important to note that rate increases may be necessary to renew assets, complete essential works and mitigate external budgetary pressures beyond councils’ direct control, deficiencies in performance information prevent councils from identifying internal efficiencies that can moderate the need for such increases, or from adequately demonstrating to their communities why rate increases are necessary.

The long-term and recurring nature of these challenges also highlights a significant and growing opportunity cost to councils and their communities and, therefore, reinforces the need for more effective performance management and reporting across the sector.

Performance reporting by local government

Improvements to elements of performance reporting practices since 2008 were evident at all 10 councils examined. However, these were limited. No council had developed a set of indicators that adequately measured the impact of services and achievement of objectives.

Improvements to performance reporting practices included:

- aligning performance information with councils’ strategic objectives—at all councils

- refining performance information to be more balanced—at Boroondara and Knox

- strengthening service planning processes to improve accountability for service outcomes in relation to strategic objectives—at Moreland and Knox

- introducing new electronic reporting systems that link day-to-day activities with strategic objectives—at Colac Otway.

These developments are encouraging, however, further action is required to establish the foundations necessary for effective performance reporting.

Key issues compromising the effectiveness of performance reporting at councils were:

- poorly expressed objectives that cannot be effectively measured

- indicators that do not comprehensively cover all aspects of councils’ objectives and key strategic activities

- indicators that do not provide balanced information about quality, efficiency and outcomes

- a lack of adequate policies for performance reporting

- limited training for councillors and staff in performance measurement and management.

These issues were evident at all examined councils, demonstrating they have yet either to fully implement previous audit recommendations or to produce performance reports that adequately meet stakeholder needs.

Further issues identified at a subset of councils were:

- a lack of connection between strategic objectives and service objectives—at Baw Baw, Central Goldfields, Indigo and Wangaratta

- reports that did not include results for all indicators identified within council plans—at Horsham, Knox, Moreland and Wyndham

- an over-reliance on limited community satisfaction metrics for assessing services, which do not provide a sufficiently comprehensive and balanced view of performance—evident at Baw Baw, Indigo and Wangaratta.

Better practice was evident at Boroondara and Knox. Both councils reviewed their practices following our 2008 audit and introduced new indicators resulting in more balanced performance reporting overall, compared to the other councils examined.

However, further development of outcome and efficiency indicators is required to consolidate and build on these improvements to achieve effective performance reporting.

Councils identified a number of challenges that affected their capacity to improve performance reporting processes. These included:

- the administrative requirements of contributing to work by the Essential Services Commission (ESC) on developing a reporting framework, which diverted attention away from related internal improvement initiatives

- resource limitations, particularly at regional and rural councils

- councillors and communities assigning lower priority to addressing performance information issues.

These challenges need to be addressed so councils can acquit their statutory obligations to use their resources efficiently and effectively in line with best value principles, and to mitigate the significant opportunity cost currently borne by ratepayers.

Statewide local government performance reporting initiatives

The ESC undertook extensive work during the period 2009–11 to develop a statewide performance assessment and benchmarking framework for local government service delivery.

This was a positive initiative designed to improve performance reporting in the sector.

ESC proposed the progressive implementation of a framework for council reporting based on a set of 17 or 18 service indicators, and between 17 and 20 supporting indicators, subject to applicability each year.

The initial set of indicators was chosen following an extensive review of performance information in the sector that highlighted the low maturity of existing performance indicators, and the relative absence of outcome-based measures linked to council objectives—a situation affirmed by both this audit and our 2008 report.

ESC intended to refine and improve its initial set of indicators in consultation with councils over time to address these gaps. However, the early discontinuation of this initiative meant ESC was unable to fully implement its plan and therefore achieve its intended goal.

Although ESC’s framework required further development at the time it was discontinued, ESC’s work offers valuable insights on the way forward.

In summary, key lessons include:

- the need for an iterative approach to improving the maturity of council performance information

- the importance of consultation and engagement with the sector

- the need to focus on a common core set of council services as identified by ESC’s classification

- the need to recognise and address the significant challenge that disparate council objectives and priorities pose to developing meaningful outcome measures common to all councils.

These are important insights for future reform initiatives.

Proposed framework for local government performance reporting

The cessation of ESC’s initiative, coupled with recurring performance challenges in the sector, highlights the need to produce and embrace a statewide performance reporting framework.

The framework should provide a holistic picture of financial and non-financial performance that is outcome focused, based on established models, and capable of implementation without unnecessarily increasing the reporting burden on local government.

RoGS provides a blueprint for developing indicators that is consistent with our 2008 principles. However, the necessary indicators—including data sets and quality assurance arrangements—are not yet in place at councils, and considerable work remains to address these gaps.

This report outlines a pathway for further developing a sound local government performance reporting framework based on the RoGS model, and building on the valuable insights from ESC’s work.

Recommendations

- All councils should:

- review their strategic and service objectives to assure they are clearly expressed, measurable and aligned

- critically review the performance information in their annual reports to assure it is relevant, balanced, appropriate and clearly aligned with their objectives

- document and approve performance reporting policies and standards

- provide training for councillors and staff on effective performance measurement, management and reporting.

- The Department of Planning and Community Development should seek the approval of the Minister for Local Government to develop regulations establishing minimum standards for the form and content of performance statements.

- Local Government Victoria, councils, and local government peak bodies should adopt the proposed local government performance reporting framework and associated implementation strategy.

- Local Government Victoria, in consultation with stakeholders, should lead and expedite establishment of the governance structure for implementation.

Submissions and comments received

In addition to progressive engagement during the course of the audit, in accordance with section 16(3) of the Audit Act 1994 a copy of this report was provided to the Department of Planning and Community Development, the Essential Services Commission, Baw Baw Shire Council, the City of Boroondara, Central Goldfields Shire Council, Colac Otway Shire, Horsham Rural City Council, Indigo Shire Council, Knox City Council, Moreland City Council, Wangaratta Rural City Council and Wyndham City Council with a request for submissions or comments.

Agency views have been considered in reaching our audit conclusions and are represented to the extent relevant and warranted in preparing this report. Their full section 16(3) submissions and comments however, are included in Appendix E.

1 Background

1.1 Introduction

1.1.1 The role of local government and performance reporting

The Constitution Act 1975 establishes local government as a distinct and essential tier of government with the functions and powers necessary to ensure the peace, order and good government of each municipal district.

Each council is therefore primarily accountable to its local community. The Local Government Act 1989 (the Act) reinforces this by establishing the primary objective of each council as endeavouring to achieve the best outcomes for its local community and having regard to the long-term and cumulative effects of decisions.

Victoria’s 79 councils invest significant resources each year in the delivery of a range of services to their communities. They collectively maintain around $60 billion of community assets and infrastructure. They spend around $1.6 billion each year on capital works, and a further $6 billion annually on a variety of services including waste management, recreation, aged, family and other human services.

While the operating context of each council varies depending on geography, size, demographics, local needs and priorities, all councils have the same obligation to manage their finances responsibly and to assure their services and facilities meet community needs.

Effective performance reporting assures councils are accountable to their local residents and ratepayers for these important obligations. It is critical for demonstrating value-for-money, the achievement of objectives, equitable access to services, and that services are appropriate, of good quality, and cost effective.

1.1.2 Councils’ obligations to their local community

Financial management obligations

The Act was amended in 2003 to include a requirement that councils apply principles of sound financial management to their planning and budgeting. These principles require councils to:

- prudently manage financial risks having regard to economic circumstances

- pursue spending and rating policies that are consistent with a reasonable degree of stability in the level of the rates burden

- ensure that decisions made and actions taken have regard to their financial effects on future generations

- ensure full, accurate and timely disclosure of financial information relating to the council.

Service delivery obligations

The Act also requires council facilities and services to be accessible and equitable and sets out the best value principles that should inform council decisions on services.

The application of these principles aims to improve local government services by making them more affordable and responsive to local needs, and to encourage councils to engage with their communities in shaping services and activities.

The Act identifies the following six principles to guide how a service should be monitored and reviewed on an ongoing basis:

- All services should be responsive to community needs.

- Each service should be accessible to those community members for whom the service is intended.

- A council should achieve continuous improvement in the provision of services to its community.

- A council should develop a program of regular consultation with its community in relation to the services it provides.

- All services provided to the community should meet the cost and quality standards set by the council.

Regular service reviews in accordance with the best value principles enable a council to assess the effectiveness and efficiency of its services, and to take action where necessary to assure its services continue to meet the community’s needs.

Strategic and annual planning obligations

The amendments to the Act in 2003 also introduced new corporate and financial planning requirements that aimed to better align strategic planning with annual planning.

These included the requirement to develop a four-year council plan setting out the strategic objectives of the council, strategies for meeting them and performance indicators for monitoring their achievement. A strategic resource plan underpins the council plan, and identifies the financial and non-financial resources needed to meet the objectives.

Similarly, each council is required to develop an annual budget describing its activities, initiatives and financial requirements for the year. It should also set out how the activities will contribute to achieving the strategic objectives as well as performance measures and targets for a number of key strategic activities.

The terms ‘key strategic activity’ and ‘performance measure’ are not defined in the Act or supporting Local Government (Finance and Reporting) Regulations 2004.

Performance reporting obligations

The Act requires councils to report annually on their performance. Specifically, it requires them to prepare an annual report within three months of the end of the financial year, to provide a copy of this report to the Minister for Local Government, and to make the report publicly available. The Act and regulations require the report to include:

- an acquittal of actual results against the annual financial budget in the form ‘standard’ statements. The format of the standard statement is specified in the Regulations and is independently audited

- a ‘performance’ statement, which acquits actual results against the performance target for each key strategic activity. There is no format specified for the performance statement in the regulations, although they are required to be independently audited

- a report on operations that explains progressive performance against the strategic indicators identified in the four-year council plan. These explanations are not required to be audited.

These important performance reporting obligations were introduced by the 2003 legislative reforms to achieve greater accountability by councils to their communities.

1.2 Previous audit coverage

1.2.1 Performance Reporting in Local Government

Our 2008 audit of Performance Reporting in Local Government examined how well councils had implemented these reforms. Specifically, it assessed whether councils’ publicly reported performance information in their annual reports was useful, and underpinned by a comprehensive and cohesive reporting framework such as policies, guidelines and training.

The audit reviewed the performance statements of all 79 councils and assessed whether the information they contained was relevant, appropriate and fairly presented. It concluded that for most councils reporting had limited relevance to ratepayers, and lacked information about the quality of council services, the outcomes being achieved, and how these related to councils’ strategic objectives. It also found that in most cases, councillors and council staff were not equipped with the knowledge and skills required to fully understand and develop appropriate performance reports, and that policies were either very limited or non-existent.

The audit recommended that all councils critically review and improve their publicly reported performance information, that they document and approve performance reporting policies and standards, and provide councillors and staff with appropriate training. It also recommended that regulations be issued establishing the minimum standards for the form and content of performance statements, however, this has yet to occur.

1.2.2 Local Government Performance Reporting: Turning Principles into Practice

Our 2008 guide Local Government Performance Reporting: Turning Principles into Practice was produced to complement our audit report and assist councils to achieve effective performance reporting.

The guide highlights the key principles of effective performance reporting and provides guidance on their application in the local government context. These principles are summarised in Figure 1A.

Figure 1A

Principles of effective local government performance reporting

Comprehensive

To be comprehensive, indicators should be relevant to council objectives. Objectives should be clearly expressed, measurable, and there should be a clear nexus between objectives and performance indicators. Performance indicators should also cover all critical aspects of objectives and align with services.

Balanced

Performance indicators should cover the time, cost, quantity and quality of service provision, as well as the outcomes of council activity. A single indicator is typically not able to measure each of these aspects, therefore a suite of indicators is usually required to provide balanced performance information.

Appropriate

Performance indicators should be reported with appropriate context to allow community members to interpret results. Targets, trend data and an explanation of the result should be provided to allow members of the community without technical knowledge to draw meaningful conclusions about the performance of council.

Source: Victorian Auditor-General’s Office, Local Government Performance Reporting: Turning Principles into Practice, 2008.

1.2.3 Local Government: Results of the 2010–11 Audits

Our 2011 report Local Government: Results of the 2010–11 Audits performed a high‑level review of 10 council performance statements against the framework set out in our 2008 guide, to assess the adequacy of councils’ actions on performance reporting.

It concluded that limited improvement was evident in the quality of the performance statements produced by councils, and that non-financial performance indicators are of limited relevance to ratepayers and residents. The report further noted that councils continue to adopt a ‘compliance-centric’ approach to performance information, and that they have yet to fully implement previous audit recommendations or to produce performance reports that drive council outcomes and accountability by being relevant and appropriate to stakeholder needs.

1.3 Relevant statewide initiatives

In October 2009, the Essential Services Commission (ESC) received a terms of reference from the Minister for Finance to develop and implement a statewide performance monitoring framework for local government service delivery.

ESC engaged in extensive and in-depth consultation with the sector during the initial development process. In June 2010, ESC released a report that made the following five recommendations for establishing a Victorian Local Government Services Report:

- Features of the report—councils were to report on a set of 17 or 18 service indicators, and between 17 and 20 supporting indicators, subject to applicability, on an annual basis.

- Report integration—councils were to include in their council plans their individual objectives and desired outcomes for the services reported.

- Implementation time lines—a staged implementation process was to be followed with full implementation to be achieved with the release of the 2013 report.

- Enabling legislation—the report was to have been implemented through amendments to the Local Government Act 1989 and the Essential Services Commission Act 2001.

- Other recommendations—consideration was to have been given to:

- undertaking a review of reporting requirements imposed on councils by state agencies

- identifying and including financial indicators of council performance in the report

- providing financial assistance to councils that are financially or resource constrained to assist them in implementing the reporting framework.

In January 2011, consistent with the terms of reference and as part of the phased implementation process, ESC released a prototype report. Prepared with the support of 33 councils who volunteered to participate, the Victorian local government pilot services report 2009–10: Report to the Minister for Finance and Minister for Local Government presented ESC and stakeholders with the first opportunity to refine the services report and the underlying reporting processes.

In September 2011, the Minister for Finance, on request from the Minister for Local Government, advised ESC to not proceed with the 2010–11 report indicating the state was focusing on the strategic framework in which advances to performance reporting can take place. Both ministers expressed appreciation to ESC for its work to date.

1.4 Audit objective and scope

1.4.1 Audit objective

The objective of this audit was to assess the effectiveness of existing local government performance reporting arrangements, and the adequacy of statewide initiatives to reform local government performance reporting.

It examined progress since 2008, the issues impeding effective performance reporting in councils, and the merits of alternative performance reporting models for the Victorian local government sector.

1.4.2 Audit scope

The audit was conducted in the Department of Planning and Community Development, the ESC and the following 10 councils:

- Baw Baw Shire Council

- City of Boroondara

- Central Goldfields Shire Council

- Colac Otway Shire

- Horsham Rural City Council

- Indigo Shire Council

- Knox City Council

- Moreland City Council

- Wangaratta Rural City Council

- Wyndham City Council.

1.4.3 Method

The audit was performed in accordance with the Australian Auditing and Assurance Standards.

1.4.4 Cost of the audit

The total cost of the audit was $480 000.

2 Recurring performance challenges in the sector

At a glance

Background

A review of our performance audits of local government between 2000 and 2011 highlighted a range of ongoing performance challenges for councils.

Conclusion

Successive audits since 2000 reveal recurring instances of ineffective planning and budgeting, poor implementation of initiatives, and shortcomings in management oversight and monitoring. Weaknesses in the quality and availability of performance information have reduced councils’ accountability for performance, and have impeded their capacity to address the issues.

Findings

The following recurring themes were identified:

- Poor financial and asset management practices were identified repeatedly, offering little assurance that councils’ long-term financial management is robust.

- A lack of effective policies, planning, monitoring and evaluation, including data quality assurance was identified in multiple audits, reducing assurance that councils are operating efficiently, and in compliance with relevant obligations.

- Inadequate oversight of procurement processes was an ongoing issue, despite similar issues being identified 10 years earlier.

These issues are due in part to deficiencies in the quality and availability of performance information to managers and councillors. This impedes their capacity to take corrective action.

Performance weaknesses also reflect resource constraints at councils, the administrative burden of compliance with state and Commonwealth requirements, and the difficulty of attracting and retaining skilled staff, particularly in regional and rural areas.

2.1 Introduction

Councils play a critical role in managing important community assets and services. Effective and efficient management of these resources is vital for meeting the community’s needs.

Unless assets are well managed, roads, buildings and sports grounds will deteriorate. Similarly, ineffective and/or inefficient services reduce value-for-money and can deprive residents and ratepayers from accessing important services and desired outcomes.

Good performance information helps ratepayers and councils to gain important assurance that these critical functions are being performed well. It also helps them identify inadequate performance, and to initiate timely corrective actions.

Our performance audit program provides a unique opportunity to understand how councils are performing in critical areas. We reviewed past performance audits of local government completed between 2000 and 2011. Our review involved a meta‑analysis of recurring performance issues at councils.

It is important to note that while councils undertake a wide range of activities that can involve elements of good practice, the meta-analysis sought to establish whether there were recurrent challenges, and unresolved issues in local government performance over the period reviewed. We also sought to identify whether poor performance information and reporting was associated with identified performance weaknesses

It should also be noted that the meta-analysis focused on the results of previous audits, and does not relate specifically to the 10 councils included in the current audit.

2.2 Conclusion

Successive audits reveal recurring themes of ineffective planning and budgeting, poor implementation of initiatives and shortcomings in management oversight and monitoring.

These issues are due in part to deficiencies in the quality and availability of performance information to managers and councillors, which has impeded their capacity to take appropriate and timely corrective action, thereby imposing a significant opportunity cost on councils and their communities.

2.3 Recurring performance challenges in the local government sector

Major findings from previous audits that demonstrate recurring performance challenges for councils are summarised in Figure 2A, and detailed further in Appendix A.

Figure 2A

Recurring performance issues for councils

|

Theme |

Summary |

Audits |

|---|---|---|

|

Ineffective planning and budgeting |

|

|

|

||

|

||

|

Business Planning for Major Capital Works and Recurrent Services in Local Government (2011) |

|

|

Inadequate adherence to policies and procedures |

|

|

|

||

|

||

|

||

|

Weaknesses in accountability, oversight and monitoring |

|

|

|

||

|

||

|

||

|

Business Planning for Major Capital Works and Recurrent Services in Local Government (2011) |

Source: Victorian Auditor-General’s Office.

2.4 The role of performance reporting

These performance issues relate to the core of what councils are required by statute to do, specifically:

- strategically plan for the future of the municipal district

- prudently manage finances in consideration of the needs of future generations

- be accountable for decisions and performance.

The recurring nature of the performance issues identified, as evidenced by the audits examined, shows they are an ongoing impediment to councils’ ability to fulfil their statutory obligations. Overcoming these challenges is, therefore, an urgent priority for the local government sector.

Several factors have caused the problems. Ongoing resource constraints, the burden of complying with state and Commonwealth requirements, and the difficulty of attracting and retaining skilled staff, all affect councils’ capacity to address performance issues in a timely way. These factors are compounded in some regional and rural areas where declining rate bases, ageing populations and natural disasters create further challenges.

In addition to these influences, poor performance information also contributes to the sector’s lack of progress in overcoming performance challenges. Councils’ understanding of the efficiency and effectiveness of their activities, and the extent to which they are compliant with relevant legislation is essential if they are to address performance challenges.

Though councils produce large volumes of information for internal and external audiences, both our current and 2008 audits of performance reporting by councils have found that this reporting often lacks information about the timeliness, cost, quantity or quality of council services, and therefore does not adequately position councils to overcome these deficiencies.

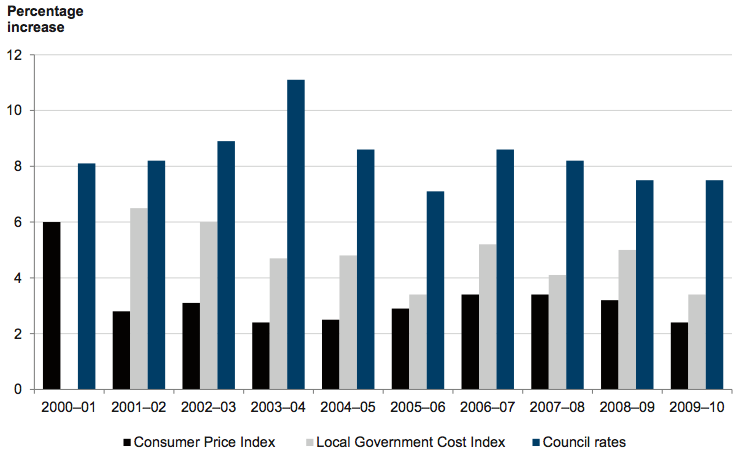

Understanding the efficiency and effectiveness of operations is essential for councils to make prudent resourcing decisions, for assuring the equitable distribution of rates, and for justifying these decisions to the community. Rate increases are an issue of considerable concern to communities. As Figure 2B illustrates, the average percentage annual increase in rates exceeded both the Local Government Cost Index (LGCI) and the Consumer Price Index (CPI) across all councils between 2000 and 2010. Each council and its community need specific diagnostic performance data to understand its rating circumstances and where opportunities for improvements may lie.

Figure 2B

Average annual increases in the Consumer Price Index, the Local Government Cost Index and council rates between 2000 and 2010

Source: Victorian Auditor-General’s Office based on information supplied by the Municipal Association of Victoria.

Important differences between the Consumer Price Index and the Local Government Cost Index

Research by the Municipal Association of Victoria (MAV) indicates that local government expenses are different to household expenses. CPI measures price movements in a standard basket of common household goods and services. However, MAV reports that a ‘basket’ of common council services is primarily affected by the growth in construction, material and wage costs, not CPI.

Specifically, the expenses of staff and contractors to deliver human-based services; including staff and materials needed to construct, maintain and upgrade assets and infrastructure means that local government costs are more affected by the Average Weekly Earnings and Roads Construction and Maintenance indexes than CPI.

In this context, MAV advises that council costs are substantially different to a basket of common household goods and services. Accordingly, MAV’s LGCI uses a combination of established indices that reflect average wages, construction and materials costs that best represent councils’ spending profile.

As Figure 2B illustrates the LGCI typically increases, on average, by around 1 per cent above CPI each year.

Factors influencing annual rate increases

It is important to note that annual rate increases can be influenced by a range of cost pressures impacting on a council’s budget, some of which may be beyond a council’s direct control. For example, some rate increases may be necessary to maintain an acceptable level of asset renewal to minimise the funding impact on future generations.

Similarly, rate increases may also be needed to mitigate external factors, such as the impacts of declining funding from other levels of government, growth in demand for some services, expanding council responsibilities, increased regulations, and growing state levies that are passed on through rates. It should also be noted that increases in the number of new households, particularly in growth areas, can also be an important driver of increases in the total rates levied

Importance of sound performance information

It is important to recognise that some rate increases may be necessary to renew assets or complete essential works. However, gaps in performance information mean that councils may not be able to adequately pursue internal efficiency improvements which can alleviate the need for significant rate increases.

Furthermore, performance information that is comprehensive and underpinned by rigorous short-, medium- and long-term planning can help councils justify resourcing decisions, including rate increases, to communities.

Overcoming the recurring performance issues identified through this meta-analysis depends in part on the availability of quality performance information for diagnosis and continuous improvement. As Part 3 of this report illustrates, such information is currently lacking in the sector.

3 Performance reporting by local government

At a glance

Background

Effective performance reporting by councils is a prerequisite for being accountable to local residents and ratepayers. Our 2008 audit Performance Reporting in Local Government found that for most councils, reporting had limited relevance to ratepayers and it recommended that they critically review and improve their performance information.

Conclusion

Local government performance reporting practices remain inadequate. While some examined councils had improved aspects of their reporting since 2008, none had developed indicators that adequately measured the impact of services and the achievement of objectives.

Findings

Key issues compromising the effectiveness of performance reporting at councils are:

- poorly expressed objectives that cannot be effectively measured

- indicators that do not comprehensively cover all aspects of councils’ objectives and key strategic activities

- indicators that do not provide balanced information about the quality, efficiency and outcomes of council services

- a lack of adequate policies for performance reporting

- poor alignment between strategic and service level objectives

- limited training for councillors and staff in performance measurement and management.

Recommendations

All councils should:

- review their strategic and service objectives to assure they are clearly expressed, measurable and aligned

- critically review the performance information in their annual reports to assure it is relevant, balanced, appropriate and clearly aligned with their objectives.

3.1 Introduction

Effective performance reporting by councils is critical for enabling residents and ratepayers to properly hold councils to account for their performance. It is also important for evaluating and improving the performance of essential municipal services and functions.

The Local Government Act 1989 sets out the compulsory reporting requirements for all councils. These include:

- a council plan, which sets out the council’s objectives, and strategies for achieving them

- an annual budget, consisting of standard financial statements and details of the key strategic activities and initiatives to be funded that financial year

- an annual report of council operations for the financial year, including audited financial and performance statements.

Our 2008 audit Performance Reporting in Local Government concluded that reporting had limited relevance to ratepayers for most councils, and that it lacked information about service quality and outcomes, including how these relate to councils’ strategic objectives. The audit recommended councils critically review their performance reporting to make it relevant, appropriate and easily understood by communities.

Our 2008 guide Local Government Performance Reporting: Turning Principles into Practice was subsequently produced to assist councils to improve their performance reporting. It highlights the key principles of effective performance reporting. Reports should be:

- comprehensive—performance indicators should be relevant to all critical aspects of council objectives, which in turn should be clearly expressed and measureable. There should be a clear nexus between objectives, indicators and services

- balanced—councils should have a balanced suite of indicators that cover all important dimensions of performance such as efficiency, quality and outcomes

- appropriate—indicators should be reported with appropriate context such as targets, trends, and explanations to enable proper interpretation of results and meaningful conclusions about performance to be drawn.

This Part of the report examines progress since 2008, and whether the performance reporting practices of selected councils meet the above principles.

3.2 Conclusion

Performance reporting by councils remains inadequate. While limited improvements were evident at the examined councils since 2008, none had fully developed a set of indicators that adequately measured the impact of services and the achievement of objectives.

A lack of clarity around councils’ objectives, combined with critical gaps in reporting on the outcomes and efficiency of their services, impede meaningful reporting by councils and reduce their accountability.

These shortcomings also mean that progress to date has not been sufficient to fully address the information needs of residents and ratepayers, to drive continuous improvement, and achieve satisfactory performance reporting.

3.3 Adequacy of performance reporting

Improvements to aspects of performance reporting practices since 2008 were evident at all 10 examined councils. However, these were limited and further action is required to establish the conditions necessary for effective performance reporting.

Notable improvements to performance reporting practices included:

- aligning performance information with councils’ strategic objectives—at all councils

- refining performance information to be more balanced—at Boroondara and Knox

- strengthening service planning processes to improve accountability for service outcomes in relation to strategic objectives—at Moreland and Knox

- introducing new electronic reporting systems that link day-to-day activities with strategic objectives—at Colac Otway.

Several councils also actively participated in the Essential Services Commission’s (ESC) work to develop a performance reporting and benchmarking framework for local government, further demonstrating their commitment to improving performance reporting. These are encouraging developments. However, the following key issues continue to compromise the effectiveness of performance reporting at councils:

- poorly expressed objectives that cannot be effectively measured

- indicators that do not comprehensively cover all aspects of councils’ objectives and key strategic activities

- indicators that do not provide balanced information about quality, efficiency and outcomes

- a lack of adequate policies for performance reporting

- limited training for councillors and staff in performance measurement and management.

These issues were evident at all examined councils demonstrating they have yet to fully implement previous audit recommendations and to produce performance reports that adequately meet stakeholder needs.

3.3.1 Comprehensiveness of performance reporting

None of the examined councils comprehensively reported on their performance, either because their objectives were not clear enough, or because existing performance indicators did not adequately demonstrate their achievement.

Clarity of objectives

Effective performance reporting requires well-expressed objectives that clearly articulate the outcomes a council is seeking to achieve. We found that poor expression of objectives compromised the effectiveness of performance reporting at all councils. This applied to the majority of objectives at Baw Baw, Central Goldfields, Horsham, Indigo, Moreland, and Wangaratta.

Figure 3A identifies a sample of strategic objectives from each examined council, and highlights issues of expression which make it difficult to report on their achievement.

Figure 3A

Sample of council objectives that limit comprehensive reporting

|

Council |

Objective |

Issue |

|---|---|---|

|

Baw Baw |

Baw Baw Shire will advocate for community members to have access to a range of local opportunities for education, learning, skills development at all levels, and learnings respond to the changing needs of local employers. |

Contains multiple dimensions. Comprehensive achievement of this objective could not be easily demonstrated as it would require indicators for advocacy, access to education opportunities at different levels, and alignment of education opportunities with local employers’ needs. |

|

Boroondara |

We will proactively manage the ongoing maintenance and development of council’s assets and facilities to meet our communities current and future needs. |

Unclear outcome. Contains multiple dimensions. Comprehensive achievement of this objective would require measurement of several components, including ‘proactive management’, and the extent to which management meets current and future community needs, which is not clearly defined. |

|

Central Goldfields |

Building an engaged, connected and inclusive community in which we take pride; and embracing education as the key for advancement. |

Contains multiple dimensions. Comprehensive achievement of this objective could not be easily demonstrated as it would require indicators for engagement, connection, inclusion and pride. The meaning of terms such as ‘key for advancement’ is not clear, and therefore achievement cannot be easily measured. |

|

Colac Otway |

Council will engage, plan and make decisions about land use and development that takes into account the regulatory role of Council, its diverse geography, social, community, economic and environmental impacts for current and future generations. |

This objective does not clearly convey an outcome council is seeking, but rather the manner in which council will perform a specific function. This does not allow for assessment of performance. |

|

Horsham |

Governance and Business Excellence: Excel in communication, consultation, governance, leadership and responsible use of resources. |

Multiple dimensions. Comprehensive achievement of this objective could not be easily demonstrated, as it would require indicators that convey information about excellence in communication, consultation, governance, leadership and responsible use of resources. It is also unclear what is meant by ‘excellence’ in this context, and therefore it is not possible to interpret whether it has been achieved. |

|

Indigo |

Enhance our communications. |

This objective relates to activities, and does not clearly convey an outcome council is seeking. |

|

Knox |

To provide real travel choice and reduce inequalities in access to transport opportunities in Knox by advocating for and facilitating improvements in transport infrastructure and services. |

Multiple dimensions. Comprehensive measurement of the extent to which this objective has been achieved would require indicators of travel choice, equity of access, advocacy, and infrastructure and service improvements. |

|

Moreland |

Ensure provision of appropriate aged services. |

This objective relates to council activities, and does not clearly convey the outcome council is seeking. The term ‘appropriate’ is not defined, and therefore it is not possible to determine whether it has been achieved. |

|

Wangaratta |

Provide for a diverse range of arts, cultural and heritage experiences and opportunities utilising a variety of approaches and pathways. |

Unclear and multiple components. It is not clear what is meant by ‘a diverse range of arts, cultural and heritage experiences and opportunities’, or ‘a variety of approaches and pathways’. It is therefore not possible to interpret whether this objective has been achieved. |

|

Wyndham |

Enhance the potential for developing Wyndham’s competitive strength, attracting a diversity of increased employment opportunities for local residents. |

Unclear and multiple components. Comprehensive measurement of this objective would require definition of terms and indicators that relate to competitive strength, diversity of employment opportunities and availability of employment opportunities. |

Source: Victorian Auditor-General’s Office.

Unclear objectives create a significant impediment to effective performance reporting as they obscure rather than clarify the specific outcomes a council is seeking. In effect, this situation reduces transparency and accountability for performance because ratepayers cannot easily understand the objectives, and their achievement cannot be easily measured and determined.

Some councils advised that when their objectives are read in conjunction with their related strategies, their desired outcomes become clearer, which allows for measurement. They further advised that through measuring council’s progress towards achieving these strategies, it is possible to understand if outcomes have been achieved.

We acknowledge that strategies are valuable for the purposes of describing the activities council will perform in pursuit of its objectives. However, if objectives are not clearly specified at the outset their achievement cannot be transparently assessed based on the implementation of related strategies.

Setting clear and measurable objectives is a critical prerequisite for effective performance reporting. Adopting the completion of ‘strategies’ as de facto indicators of their achievement can have the undesirable effect of masking inadequate performance against objectives if these strategies do not comprehensively address the outcomes sought.

This cannot be detected easily if outcomes are not clearly specified, which reduces transparency and accountability for performance. There is also a risk that actual performance against objectives will be misrepresented under these circumstances by reference to strategies that do not fully address objectives.

This situation has the further undesirable effect of reversing the program logic that should be inherent in any good performance measurement and assessment framework. Specifically, it permits lower level strategies and activities to define the outcome and its achievement, rather than enabling the adequacy and success of strategies to be assessed with reference to a clearly defined outcome in the first instance.

Therefore, in order to reliably assess councils’ performance, comprehensive performance indicators directly linked to clearly specified objectives are needed.

Comprehensiveness of indicators

Performance indicators at all 10 examined councils were either not sufficiently comprehensive or relevant to measure the achievement of objectives. Boroondara, Knox and Wyndham had the most comprehensive indicators of the councils examined. However, the lack of clarity of some of their objectives meant that there was insufficient assurance that indicators adequately addressed all relevant aspects of performance.

Figure 3B highlights issues affecting the comprehensiveness of performance indicators at a sample of the councils examined.

Figure 3B

Issues affecting the comprehensiveness of selected performance indicators

|

Council |

Objective |

Performance Indicators |

Issues |

|---|---|---|---|

|

Baw Baw |

Baw Baw Shire will advocate for community members to have access to a range of local opportunities for education, learning, skills development at all levels, and learnings respond to the changing needs of local employers. |

Activity rate of active registered library borrowers within the Baw Baw located libraries. Percentage of three and four year olds enrolled in pre-school. |

Indicators do not address multiple aspects of the objective, including advocacy, availability of education options and the extent to which these meet local business needs. |

|

Colac Otway |

Council will engage, plan and make decisions about land use and development that takes into account the regulatory role of Council, its diverse geography, social, community, economic and environmental impacts for current and future generations. |

Achievement of council commitments and key actions (100). Building permits processed within statutory timeframes. Planning permits processed within statutory time frames. |

Indicators do not address several aspects of the objective, including engagement, or the social, community, economic and environmental impacts of land use planning and development activities. |

|

Wangaratta |

Provide for a diverse range of arts, cultural and heritage experiences and opportunities utilising a variety of approaches and pathways. |

Number of exhibits provided (22). Community Satisfaction Survey – Community Engagement (63%). |

These indicators do not demonstrate diversity in the range of arts, cultural and heritage experiences offered by the Shire, nor ‘approaches or pathways’. The second indicator has no relationship to the objective. |

Source: Victorian Auditor-General’s Office.

Gaps in performance reporting

A further issue affecting the comprehensiveness of performance reporting at Horsham, Knox, Moreland and Wyndham was the fact that not all of their strategic performance indicators were reported in their annual reports.

The Local Government (Finance and Reporting) Regulations 2004 require councils to provide a statement on outcomes in their annual reports in relation to their strategic indicators.

However, Horsham’s 2010–11 annual report includes results for only half of its strategic indicators. Similarly, Moreland reported on 35 per cent of its strategic indicators in the same year, and Knox reported on only a quarter.

Knox and Moreland advised that gaps in their reporting were due to the staging and timing of their initiatives reflecting the fact that their strategic objectives are to be achieved over a four-year period. Consequently, they advised it is not always possible or appropriate to report outcomes against all strategic indicators annually. Similarly, Wyndham advised that all of its strategic indicators will be reported on over the four‑year period.

While the staging of initiatives can obviously affect the availability of performance information, this does not negate councils’ statutory obligation to provide a statement of performance against its strategic indicators. Rather than simply omitting an indicator, such a statement should include an explanation of why the results for any strategic indicator are not yet available or reported. This is essential for achieving transparency and accountability for performance.

We found that, although these councils are approaching the last year of their four-year council plans, a notable proportion of indicators have never been reported on—30 per cent at Moreland and 40 per cent at Knox. Though some of these indicators are to be achieved by 2012, reporting interim progress is important to understanding whether a council is on track to achieve the target. In the absence of this information, residents and ratepayers cannot form an accurate and complete picture of council performance.

Limited relevance of performance indicators

The comprehensiveness of councils’ performance reporting was further limited in some cases by an over-reliance on general community satisfaction survey results. As these general indicators lack a clear nexus with specific council objectives they are of limited relevance.

This was the case at Indigo and Wangaratta, where community satisfaction survey results were the main indicators used to assess the achievement of objectives.

Our 2008 report Performance Reporting in Local Government noted that community satisfaction results are important performance metrics for councils. However, they can only provide general measures that do not correlate closely with any particular council activity, or necessarily align with any one objective. They can also be affected by factors outside of a council's direct control and influence that may not relate to the quality of services or effectiveness of the council.

Using a general measure to evaluate a specific activity or set of activities, particularly one based on public perception, is therefore problematic. The lack of specificity in performance data limits its usefulness as a tool for continuous improvement.

3.3.2 Balance of performance indicators

It is unlikely that a single indicator will adequately capture all aspects of performance. Our 2008 guide highlighted that better practice performance reporting consists of a balanced suite of indicators covering the dimensions of output efficiency, output quality and outcome effectiveness.

Some councils have improved the balance of their performance information since 2008. However, they still lack adequate indicators for measuring the efficiency and outcomes of all their key activities.

Improved balance at Boroondara and Knox

Better practice was evident at Boroondara and Knox. Both councils had developed indicators that measured the quality, efficiency, and to a limited extent, the effectiveness of some of their activities.

Each council had reviewed and improved their performance indicators since 2008, taking into account our better practice guidelines. Both also provided useful context for all indicators to support interpretation of their performance, typically through specifying targets and in some instances, reporting trends. Boroondara provides further context for some of its indicators by benchmarking against other councils.

These initiatives are encouraging, but further improvement is needed to achieve a fully balanced suite of indicators.

Boroondara’s indicators are more balanced overall, but require further development to achieve a more complete picture of the effectiveness and efficiency of all council operations. Specifically, while some outcome indicators have been developed they do not yet address most strategic objectives or adequately cover all key strategic activities.

Boroondara provides useful information about the effectiveness and efficiency of services in its best value reports. Making greater use of these metrics when assessing and reporting on the achievement of objectives and key strategic activities in its annual report, would further integrate and strengthen Boroondara’s performance reporting.

Similarly, Knox has developed outcome indicators for all of its strategic objectives. However, they are broad and general in nature and lack any direct nexus between council services and key strategic activities.

For example, outcome indicators against the objective ‘To improve the health and wellbeing of the Knox community’ are:

- population health for men and women to be equal to or greater than the state average (self-assessed)

- a trend over time showing reduction in the overall crime rate.

These indicators measure broad outcomes that the council contributes to, but does not directly control. The direct nexus between the desired outcome and the contributing council services/activity is not immediately clear. It is not possible, therefore, based on these metrics to directly ascertain the impact and adequacy of the council’s related actions.

Outcome indicators, particularly program effectiveness indicators, should provide information on the extent to which council objectives have been achieved as a result of funded activities. This remains a critical gap in the performance information of all councils.

Limited balance of performance indicators

Comparatively less ‘balance’ was evident in the suite of indicators used by Baw Baw, Colac Otway, Horsham, Moreland and Wyndham. These councils had only a limited number of indicators of outcomes, or of the quality and efficiency of their services.

Central Goldfields, Indigo and Wangaratta had the least balanced set of indicators of all the examined councils, with their reporting focusing mainly on the implementation of activities or community satisfaction survey results.

Encouragingly, all councils were committed to further improving the balance of their performance indicators. Knox and Moreland had initiated reviews of their service planning processes designed to improve the linkages between objectives, service activities and related performance information.

3.3.3 Appropriateness

Some councils have improved the appropriateness of their performance information since 2008 by including valuable context to assist the interpretation of performance reporting. Key improvements include:

- setting targets for all indicators associated with both key strategic activities and strategic objectives—at Boroondara, Colac Otway, Horsham, Indigo, Knox, Moreland and Wangaratta

- reporting trends in performance over time—at Boroondara, Colac Otway, Indigo, Knox, Moreland, Wangaratta, Wyndham

- benchmarking results of some indicators against other councils—at Boroondara, Colac Otway, Indigo and Knox

- explaining the variance of results from targets—at Baw Baw, Boroondara, Colac Otway, Horsham, Indigo, Knox, Moreland, Wangaratta and Wyndham.

These are positive developments, however, the quality of contextual information varied. At Colac Otway, Horsham and Knox, explanations of variance did not always provide enough detail to make sense of the result.

Further, the use of trend data and benchmarking was inconsistent and limited across all councils. Specifically, none of the councils that reported trend data did so for all strategic indicators and key strategic activities where relevant. Additionally, benchmarking against other councils was also limited.

At Indigo and Knox, community satisfaction survey indicators and community strength indicators were the only benchmarked indicators, and at Boroondara and Colac Otway, only a single indicator was benchmarked against other councils. Councils highlighted that limited benchmarking by them to date reflected their expectation that ESC’s reporting framework would have addressed this.

3.3.4 Other issues limiting the effectiveness of performance reporting

All examined councils had yet to establish internal policies governing the content, standards and quality assurance arrangements for performance reporting, indicating little improvement on this issue since 2008.

Encouragingly, some progress was evident at Knox which had produced guidelines for staff on developing meaningful performance indicators. Knox also provides training to staff on developing indicators, and works with councillors to develop suitable indicators at key stages during the planning cycle.

Despite this, there was a lack of focused training for councillors on performance indicators and reporting at all councils examined. While Boroondara and Knox briefed councillors at key points during the planning process, there was no dedicated training to build councillors’ understanding of effective performance indicators and reports.

The absence of reporting frameworks, underpinned by approved policies, clear standards, and training for councillors and staff, presents a significant obstacle to improving the effectiveness of council performance reporting.

Linkages between service delivery and strategic objectives

A further issue limiting the adequacy of performance reporting at most examined councils was the lack of clear linkages between service delivery performance and strategic objectives.

Only Boroondara and Moreland had established satisfactory linkages. Both councils had service plans in place with explicit links to strategic objectives including relevant performance indicators.

While Colac Otway, Horsham, Indigo and Wyndham had business plans connecting services to strategic objectives, none had developed adequate indicators for assessing impact. Only Wyndham’s plan included performance indicators. However, these were activity focused and thus had limited capacity to offer insights into the impact of services on strategic objectives.

Similarly Baw Baw, Central Goldfields, Knox and Wangaratta had yet to establish service plans for all their services that included performance indicators with a clear nexus to council objectives. The impact of all of their services on objectives therefore cannot be transparently assessed.

Knox intends to develop plans and indicators for all of its services as part of its current service review project.

Effectiveness of other reports

Councils typically produce a range of other reports for internal and external audiences including quarterly reports, monthly expenditure reports, capital works reports and local newsletters. Many are available to the public via council websites, and are an important way for councils to report to their communities about their activities.

However, we found that they typically use the same limited indicators as those in the annual report, which focus mainly on activities rather than outcomes. Therefore, they are not yet comprehensive enough to allow residents to understand how well council objectives are being met.

3.3.5 Challenges to improving performance reporting

Councils advised that a number of challenges impeded their ability to improve performance reporting since 2008.

Resource constraints

Smaller councils in regional and rural areas highlighted resource constraints as a major challenge to developing more comprehensive, balanced and appropriate performance indicators. They indicated that without dedicated planning and reporting resources, the administrative effort required to review and reform performance reporting would draw resources away from council service delivery.

Understandably, councils are reluctant to do this. However, the need to monitor and report on the efficiency and effectiveness of service delivery is particularly important in resource constrained councils to optimise value, minimise wastage, and enable early identification and resolution of emerging issues.

Perceived lack of support from the state

Some councils expressed the view that, with the exception of ESC’s framework, there has been little support from the state to improve council performance reporting.

While our 2008 audit recommended that the Department of Planning and Community Development (DPCD) issue minimum standards on the form and content of council performance statements, this has yet to occur. The results of the current audit indicate that the absence of such standards is a factor contributing to the ongoing variation in the quality of performance information reported by councils.

DPCD indicated that it is working on initiatives for local government that will include efforts to improve performance reporting. These initiatives are currently at an early stage of development.

ESC’s now discontinued performance reporting framework was the main statewide initiative to support councils to improve their performance reporting since 2008. Councils advised that participating in this initiative absorbed considerable administrative effort, which diverted resources away from internal efforts to reform performance reporting.

DPCD and councils also indicated they refrained from introducing parallel improvement initiatives during this period, preferring instead to wait until ESC’s work was completed so they could assess the implications.

Lack of engagement by councillors and communities

Some councils advised that improvements to performance reporting have not been prioritised because councillors are focused on delivering key projects, and on meeting the immediate needs of their communities. As a result, the administrative arrangements for measuring council’s performance tend to be afforded lower priority.

They also advised that a further related challenge is that residents usually seek information about activities that directly impact upon them, and are less interested in wider performance information that conforms to better practice principles.

While these are recognised as substantial challenges, they nevertheless need to be addressed so councils can demonstrate their acquittal of statutory obligations to use their resources efficiently and effectively in accordance with best value principles.

A lack of comprehensive, balanced and appropriate performance information means that councillors and residents cannot be assured that priority actions and ongoing services are being delivered in a timely, efficient and effective manner, or that strategic objectives are being achieved.

The various issues identified in this Part are largely consistent with those of our 2008 audit. Therefore, our previous recommendations to councils to improve their performance reporting practices remain relevant in the current context.

Recommendations

- All councils should:

- review their strategic and service objectives to assure they are clearly expressed, measurable and aligned

- critically review the performance information in their annual reports to assure it is relevant, balanced, appropriate and clearly aligned with their objectives

- document and approve performance reporting policies and standards

- provide training for councillors and staff on effective performance measurement, management and reporting.

-

The Department of Planning and Community Development should seek the approval of the Minister for Local Government to develop regulations establishing minimum standards for the form and content of performance statements.

4 Proposed framework for local government performance reporting

At a glance

Background

Recurring performance challenges in the sector highlight a need for work on a statewide performance reporting framework to continue. This section of the report proposes a holistic performance reporting framework for councils that is capable of implementation without adding unnecessarily to their reporting burden.

Conclusion

The Essential Services Commission’s early work to develop a local government performance reporting framework offers valuable insights into what is required to achieve a robust framework.

The Report on Government Services (RoGS), produced by a Productivity Commission Secretariat for the Steering Committee for the Review of Government Services, sets out a well-established performance reporting framework that is highly suited to local government. Further developing council performance reporting based on this model will require considerable work in consultation with the sector.

Findings

- Holistic performance reporting by councils requires a focus on both financial and non-financial performance.

- As a minimum, data on financial performance should convey critical information to enable assessment of the financial management and sustainability of a council.

- Non-financial performance reporting should at a minimum cover the effectiveness and efficiency of service delivery taking into account such factors as equity, access, service quality and cost-effectiveness.

- The RoGS framework sets out a clear conceptual model for reporting on non‑financial performance that provides a pathway for developing a sound local government performance reporting and benchmarking framework.

Recommendation

The local government sector should adopt the proposed local government performance reporting framework and associated implementation strategy.

4.1 Introduction

Performance reporting in the Victorian local government sector is mainly limited to reporting on activities and outputs. Important information about outcomes, quality, equity, access and cost-effectiveness are often missing from councils’ annual reports.

To be effective, council performance reporting should provide a holistic picture of performance to stakeholders. It should provide them with critical data to enable assessment of both service delivery performance and the financial management and sustainability of councils.

Achieving meaningful comparative council performance reporting is a significant challenge. Councils are complex organisations that manage significant infrastructure and deliver a diverse range of services to their communities. These characteristics, including differences among local communities, mean that achieving meaningful, holistic performance reporting is not a straightforward task.

In October 2009, the Essential Services Commission (ESC) was directed by the Minister for Finance to develop and implement a performance assessment and benchmarking regime for councils. ESC consulted extensively with councils and released a prototype report in January 2011 before ceasing work on its framework in September 2011 at the minister’s direction.

Recurring performance challenges in the sector strongly indicate that work towards an appropriate local government performance reporting framework should continue. This section of the report proposes an approach for further developing such a framework based on proven models, and which builds upon the insights from ESC’s work.

4.2 Conclusion

ESC’s early work yielded valuable insights into the actions needed to develop a robust performance reporting framework.

The Report on Government Services (RoGS), produced by a Productivity Commission Secretariat for the Steering Committee for the Review of Government Services, sets out a well-established performance reporting framework for government service provision that is highly suited to the Victorian local government sector.

RoGS identifies a useful framework for assessing service outputs and outcomes against objectives. However, the necessary indicators, data sets and quality assurance arrangements are not yet in place at councils.

These gaps pose a significant barrier to effective performance reporting by councils.

4.3 Purpose and architecture of proposed performance reporting framework

This section of the report proposes a comparative performance reporting framework for local government that is outcome focused, based on established models, and capable of implementation without unnecessarily increasing the reporting burden on councils. It is important for the proposed framework to be developed in consultation with the local government sector. Its purpose and architecture are outlined below.

4.3.1 Purpose of proposed framework

The national Steering Committee for the Review of Government Service Provision highlights the importance and benefits of comparative measurement in RoGS.

Specifically, it points out that better performance information improves accountability and contributes to the wellbeing of all citizens by driving better service provision. It also notes that it permits assessment of whether policies are being effectively and efficiently implemented, and whether services are reaching those people for whom they are intended.

Focusing on outputs and outcomes also helps to shift the focus from the level of resources provided to the efficiency and effectiveness with which those resources are used. Meaningful comparative performance reporting also helps to build a repository of balanced, credible information that can assist in:

- verifying high performance and identifying agencies/services that are successful

- enabling agencies to learn from peers that are delivering higher quality and/or more cost effective services

- generating additional incentives for agencies to improve performance.