Portfolio Departments and Associated Entities: 2015–16 Audit Snapshot

Overview

This report details the outcome of the financial audits of the seven portfolio departments and 207 associated entities for the financial year ending 30 June 2016. We table separate sector-based reports on the financial audit outcomes for the water, local government, public hospitals, tertiary education and university sectors.

This report includes two recommendations; one for portfolio departments and one for the Department of Education & Training.

Portfolio Departments and Associated Entities: 2015–16 Audit Snapshot: Message

Ordered to be published

VICTORIAN GOVERNMENT PRINTER November 2015

PP No 222, Session 2014–16

President

Legislative Council

Parliament House

Melbourne

Speaker

Legislative Assembly

Parliament House

Melbourne

Dear Presiding Officers

Dear Presiding Officers Under the provisions of section 16AB of the Audit Act 1994, I transmit my report Portfolio Departments and Associated Entities: 2015−16 Audit Snapshot.

Yours faithfully

Andrew Greaves

Auditor-General

23 November 2015

Audit overview

This report details the outcome of the financial audits of seven portfolio departments and 207 associated entities for the financial year ending 30 June 2016. We table separate sector-based reports on the financial audit outcomes for the water, local government, public hospital, tertiary education and university sectors.

Conclusion

Financial reporting for the 2015–16 year has improved. The significant issues that resulted in unprecedented modifications of some portfolio departments' 30 June 2015 audit opinions have largely been addressed. In particular, the Department of Education & Training (DET) systematically addressed prior-year audit concerns and now has better financial management and governance practices.

Machinery-of-government (MOG) changes announced in 2014 created the Department of Health & Human Services (DHHS) and the Department of Economic Development, Jobs, Transport & Resources (DEDJTR). Both new departments implemented the MOG changes and are working toward achieving further efficiencies.

Findings

Financial reporting outcomes

We issue an unmodified audit opinion when we determine that a financial report fairly presents the transactions and balances for the reporting period, in accordance with the relevant reporting framework.

We issued unmodified audit opinions on 199 financial reports for 2015–16, including the five Victorian alpine resorts, whose financial years ended on 31 October 2015. Thirteen audits were not finished when we finalised this report. Appendix B lists the portfolio departments and associated entities included in this report and illustrates the outcome of their audit opinions.

We included an 'emphasis of matter' paragraph on 33 of the audit opinions issued. An emphasis of matter paragraph draws a reader's attention to matters within the financial report.

We issued a clear opinion on the 30 June 2016 transactions and balances of both DET and the Department of Treasury & Finance (DTF). Our opinions retained the modifications issued in 2014–15 on school transactions at DET, and on the accounting for East West Link project funds at DTF.

When conducting our audits of portfolio departments, we bring any issues identified to the attention of the secretary and the audit committee through interim and final management letters. During our 2015–16 audits, we raised 52 issues rated high and medium risk. Most high-risk issues related to information technology control weaknesses.

We observed a small improvement in the timeliness of portfolio departments addressing management letter issues. Of the 106 issues raised in 2014–15, 60 have been resolved.

In 2013–14, we outlined a number of serious internal control issues at three of the state's alpine resorts. We followed up management's actions during 2014–15 and identified significant improvements at Lake Mountain and Mount Baw Baw. Falls Creek is in the process of resolving its issues in the current year.

Department of Education & Training

We issued our audit opinion on the DET financial report on 29 September 2016. We were able to give a clear opinion on the transactions and balances as at 30 June 2016.

Our opinion was modified because DET had not resolved the audit matters relating to school transactions that formed part of the disclaimer of audit opinion in 2014–15. We were therefore unable to form an opinion on the comparative numbers for the school transaction lines.

In 2015–16, DET took a new approach to assurance about schools transactions and balances, and we support this new approach. However, it was not practical for DET to retrospectively carry out additional assurance work on the 2014–15 school transactions that are used for comparison in the current financial report.

We did get sufficient and appropriate audit evidence that the comparative property, plant and equipment transactions and balances were materially correct. This was because DET conducted significant investigation and resolution of longstanding problems, and addressed all audit matters.

In 2013–14 and 2014–15, we reported to Parliament that the financial reporting processes at DET were poor. These processes were much better in 2015–16 and we no longer consider DET's financial reporting to be poor.

Machinery-of-government changes

In December 2014, the state government initiated MOG changes which impacted the 2014–15 financial year.

The implementation and governance of the MOG changes were guided by a steering committee at both DHHS and DEDJTR, and overseen by a task force established by the Department of Premier & Cabinet. The steering committees had terms of reference and clear reporting lines, set milestones and reported regularly to senior management and the secretaries.

Despite this, there have been implementation delays at both departments.

Neither DHHS nor DEDJTR conducted a true post-implementation review. Both departments have therefore missed the opportunity to learn from what worked well and to identify areas for improvement.

During our review, we identified that there was no MOG implementation framework to guide Victorian public sector entities. Such frameworks exist in other jurisdictions and they formed the better-practice elements for our review. While we were preparing this report, DTF released a Victorian public sector operating manual on machinery-of-government changes which had been collaboratively prepared by the portfolio departments' chief finance officers and finance deputy secretaries. This is a good initiative that should guide the implementation of any future changes.

Recommendations

1. We recommend that portfolio departments address internal control issues in a timely manner, with emphasis on those risks rated medium and above (see Part 2).

2. We recommend that the Department of Education & Training introduce systems and processes that automate transactions to reduce the volume of cash transactions at schools (see Part 3).

Responses to recommendations

We have consulted with named portfolio departments and agencies, and we considered their views when reaching our audit conclusions. As required by section 16(3) of the Audit Act 1994, we gave a draft copy of this report to those agencies and asked for their submissions or comments.

The following is a summary of those responses. The full responses are included in Appendix A.

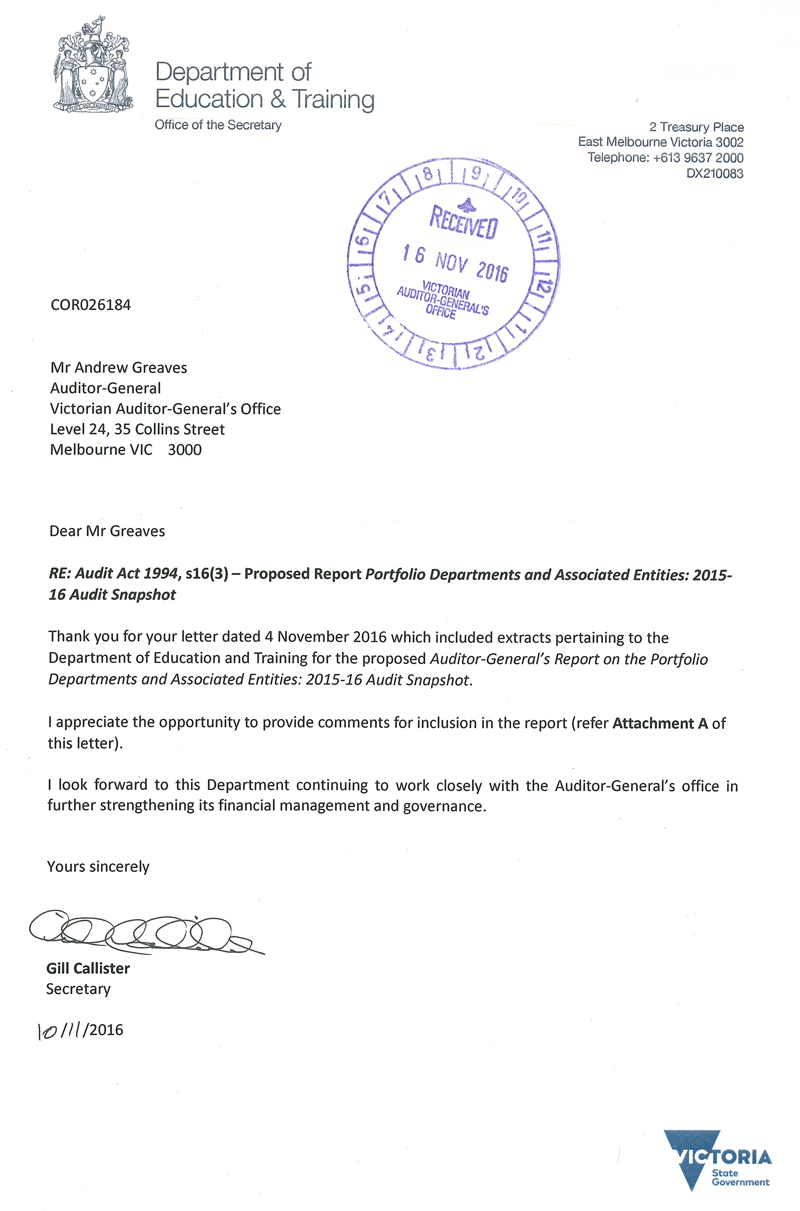

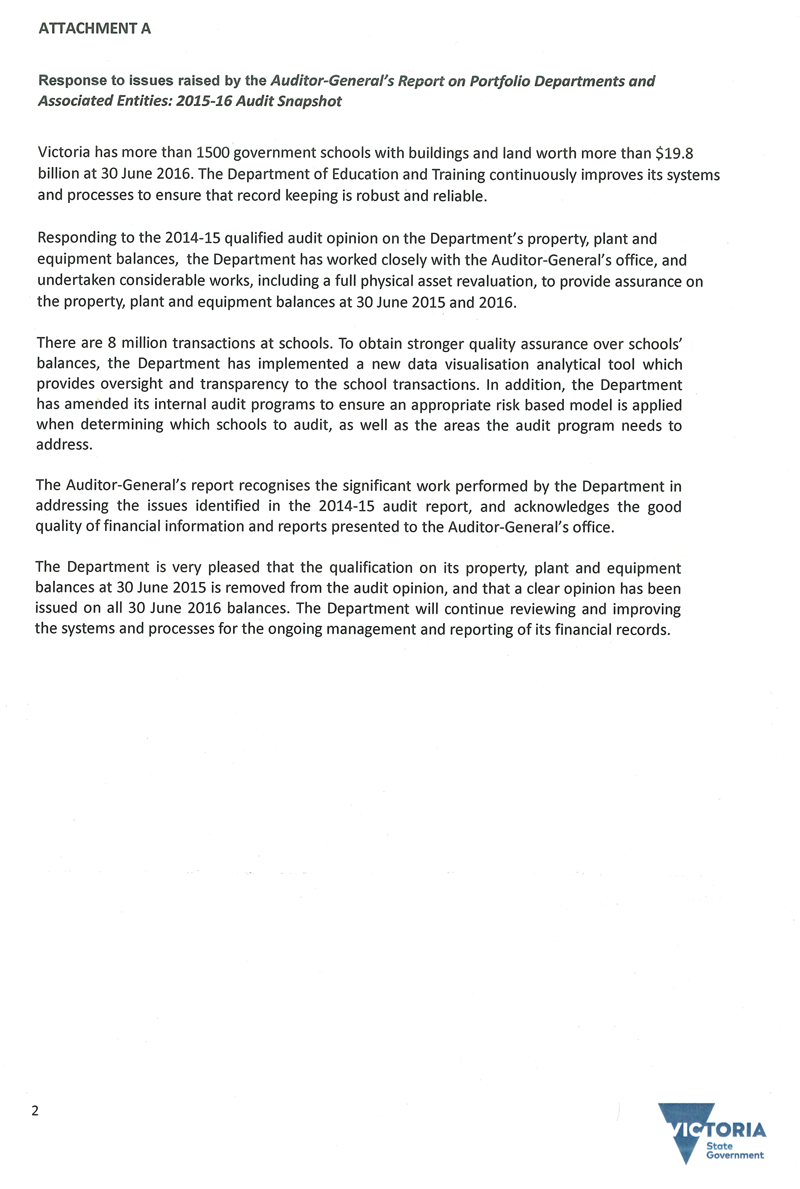

The Secretary of DET outlined the considerable work the department has done on its property, plant and equipment balances, and also on new assurance approaches for school transactions and balances. She is very pleased with the removal of the property, plant and equipment qualification for 30 June 2015 and the clear opinion on all 30 June 2016 balances. The secretary also commits to continue reviewing and improving DET's financial management and reporting.

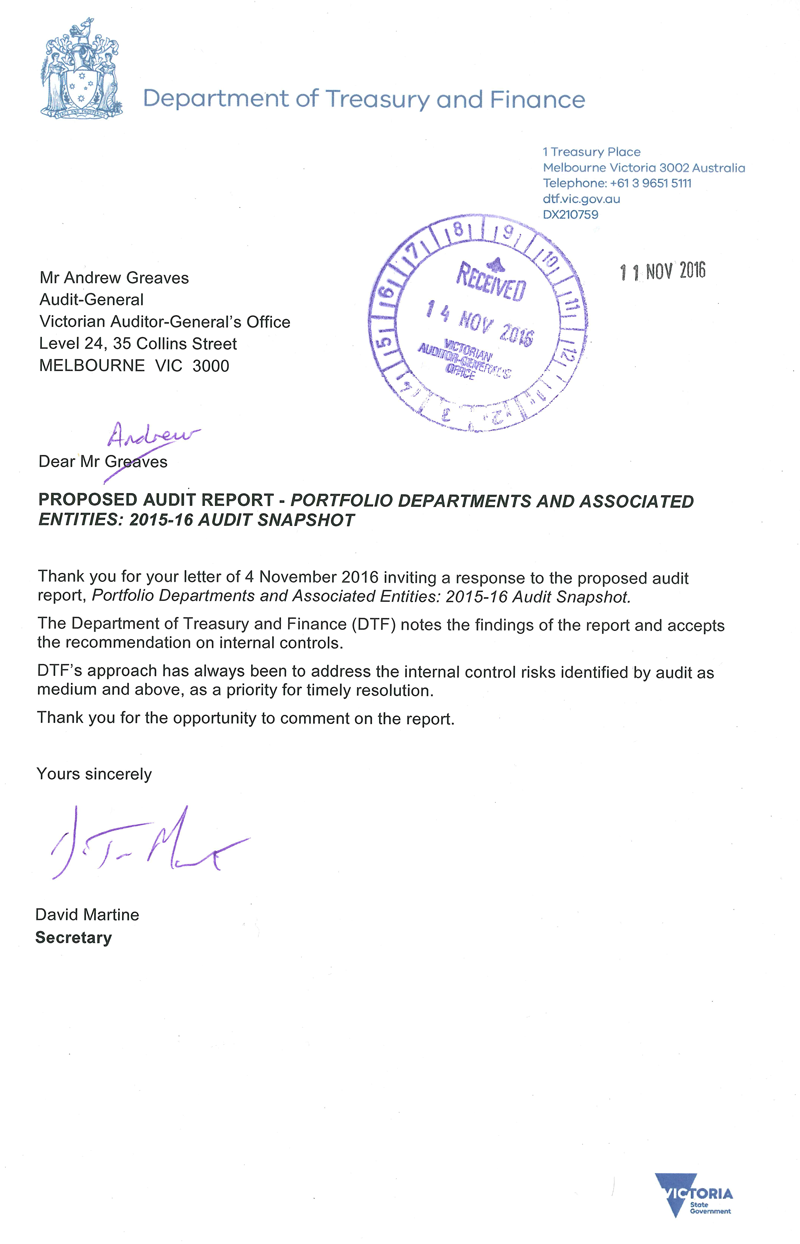

The Secretary of DTF noted the findings and accepted the recommendation to address internal control issues on a timely basis.

1 Context

This report presents the findings of the 2015–16 financial audits of the seven portfolio departments and the 207 associated entities that are not included in our other audit snapshot reports. In Appendix B, we detail the entities covered in this report.

All these entities report in accordance with the Australian Accounting Standards. The Financial Management Act 1994 and the Corporations Act 2001 are themost common reporting frameworks the entities use.

We carried out the financial audits of these entities in accordance with the Australian Auditing Standards. Figure 1A outlines the structure of this report.

Figure 1A

Report structure

Part |

Description |

|---|---|

2: Results of audits |

Provides an overview on the results of financial audits and the internal control issues observed at portfolio departments, and updates the observations made at the alpine resorts. |

3: Department of Education & Training |

Provides information on the outcome of the 2015–16 financial audit of the Department of Education & Training and an update on progress addressing financial reporting issues identified in previous years. |

4. Machinery-of-government changes |

Discusses the policies, implementation and oversight of machinery-of-government changes at two portfolio departments, which came into effect on 1 January 2015. |

Financial sustainability

In previous reports, we have analysed the financial sustainability of the associated entities covered by this report. We have conducted that assessment using four financial sustainability indicators that flag short- and long-term risks.

Our results of this financial sustainability assessment have been the same year on year with no observed change. The systemic challenge for self-funding entities is making enough of a surplus to renew their assets and fund new assets, and this long‑term risk is always flagged. However, the current government funding structure allocates capital money across portfolios strategically, based on need, and not annually at the pace of depreciation. While this funding structure is in place, the financial sustainability results for self-funding entities will remain the same.

Consequently, this report includes the calculations for financial sustainability in Appendix D but we have not include a Part analysing the trends from the financial sustainability calculations. In the future, we will revisit our approach, assessing what financial sustainability risks may exist in associated entities.

Our audits

The financial audits of the 214 entities included in this report were undertaken under section 15 of the Audit Act 1994 and Australian Auditing Standards. The cost of these audits is paid for by each entity. The results of these audits were used in preparing this report. The cost of preparing this report was $205 000, which is funded by Parliament.

2 Results of audits

In this Part, we outline the audit opinions issued on the 2015–16 financial statements of the portfolio departments and associated entities. We also summarise the number of issues raised and reported to portfolio departments during the course of our audits. We make particular mention of how the alpine resorts have addressed significant issues previously reported.

2.1 Audit opinions on financial reports

Independent audit opinions provide reasonable assurance that the information reported in financial statements is reliable and accurate. An unmodified audit opinion confirms that the financial statements fairly present the transactions and balances for the reporting period, in accordance with the requirements of applicable Australian Accounting Standards and any applicable legislation—such as the Financial Management Act 1994 or the Corporations Act 2001.

We issued unmodified audit opinions on 199 financial reports finalised for 2015–16. At the time we prepared this report, we have yet to finish 13 audits.

2.1.1 Modified audit opinions

We issue modified audit opinions when we conclude that the financial report includes a material misstatement or where we cannot get sufficient audit evidence, or the right audit evidence, to conclude that the financial report has no material misstatements.

We provided a clear audit opinion on the financial performance and position of the Department of Education & Training (DET) and the Department of Treasury & Finance (DTF) at 30 June 2016. However, we included a modified opinion on the 2014–15 comparative disclosures for DET relating to school transactions and for DTF relating to East West Link project funds.

We explain our reasons for modifying the DTF audit opinion in the Auditor‑General's Report on the Annual Financial Report of the State of Victoria, 2015–16.

In Part 3 of this report, we discuss further our reasons for modifying the DET audit opinion.

2.1.2 Emphasis of matter

Without qualifying a financial report, we may include an emphasis of matter (EOM) paragraph that highlights a particular aspect of the report that we consider fundamental to understanding how the report was prepared. For example, we will note when a financial report has been prepared using a special‑purpose framework to meet specific users' information needs rather than general users' needs.

In 2015–16, we issued 26 audit opinions on special-purpose financial reports for entities within the scope of this report. Our EOM paragraphs drew attention to the special-purpose framework adopted in preparing these financial reports.

A further seven audit opinions contained an EOM for other reasons, detailed in Figure 2A.

Figure 2A

Audit opinions issued with an EOM paragraph

Entity |

Reason for the EOM |

|---|---|

Lake Mountain Alpine Resort Management Board

|

The EOM drew attention to the Premier's decision to merge Lake Mountain and Mount Baw Baw into a new entity, the Small Alpine Resort Management Board, in 2016. It is not certain whether these two alpine resorts will continue to be separate reporting entities. |

Rural Finance Corporation of Victoria |

The EOM drew attention to the financial report being prepared on a going-concern basis, even though the corporation was abolished on 30 June 2016. |

State Electricity Commission of Victoria |

The EOM drew attention to an agreement to supply electricity to the Portland aluminium smelter, expiring on 31 October 2016, which affects the commission's functions and responsibilities. |

State Library of Victoria Foundation |

The EOM drew attention to the financial report being prepared on a liquidation basis because the foundation was being wound up. |

Tourism Victoria |

The EOM drew attention to the Premier's decision to transfer the tourism marketing functions of Tourism Victoria to Visit Victoria Limited on 1 July 2016. |

Victoria Major Events Company Limited |

The EOM drew attention to the financial report being prepared on a going-concern basis, despite material uncertainty that the company would continue to exist. |

Source: VAGO.

2.2 Internal control in portfolio departments

Internal controls at the seven portfolio departments, to the extent that we reviewed them as part of our financial audits, continue to be reasonable for maintaining the reliability of external financial reporting.

Nevertheless, we reported a number of control weaknesses to departmental audit committees and secretaries during the course of our 2015–16 audits.

In 2015–16, we identified and reported 52 internal control issues at portfolio departments rated as high or medium risk. Figure 2B shows these issues by area and risk rating, excluding issues rated as low risk. The definition for each risk rating is detailed in Appendix C.

Figure 2B

Reported issues by area and risk rating in 2015–16

Risk rating of issue |

||||

|---|---|---|---|---|

Area of issue |

Extreme |

High |

Medium |

Total |

Cash and investments |

– |

– |

2 |

2 |

Commitments |

– |

– |

3 |

3 |

Financial reporting |

– |

– |

7 |

7 |

Fixed assets |

– |

– |

9 |

9 |

Information systems |

– |

10 |

7 |

17 |

Payroll and employee benefits provision |

– |

1 |

2 |

3 |

Revenue and grant funding |

– |

1 |

4 |

5 |

Other |

– |

1 |

5 |

6 |

Total |

– |

13 |

39 |

52 |

Note: This figure excludes low-risk issues.

Source: VAGO.

2.2.1 Information systems controls

We continue to raise high-risk information technology (IT) issues in the areas of management and oversight of outsourced IT functions, password management, disaster recovery and business continuity planning. Our Financial Systems Controls Report: 2015–16 tabled in parliament in November 2016, discusses in detail a number of these IT issues.

Given that portfolio departments rely on the effective functioning of IT systems, these internal control weaknesses increase the risk of fraud and financial statement errors occurring and not being detected.

2.2.2 Accuracy controls

A number of portfolio departments had deficiencies in both asset management and reconciliations prepared to support the numbers in the financial report. We observed that reconciliations are neither timely nor accurate at some portfolio departments, and the review of general journals processed is not always adequate. Both these issues can mean that inaccurate information or errors are not identified and resolved before the preparation of the financial report.

2.2.3 Status of prior-period control issues

We monitor the status of internal control issues reported in prior years, to track whether the control weaknesses we identify have been addressed. Figure 2C illustrates that management teams within the portfolio departments have resolved 57 per cent of all issues raised. This is a small improvement on last year, which indicates that portfolio departments have paid some attention to addressing the issues we raised.

Resolving these internal control deficiencies in a timely way minimises risks related to erroneous or fraudulent transactions in the financial statements.

Figure 2C

Prior periods internal control deficiencies—resolution status by risk

Risk rating of issue |

||||

|---|---|---|---|---|

Area of issue |

Extreme |

High |

Medium |

Total |

Ongoing |

– |

24 |

22 |

46 |

Completed |

5 |

29 |

26 |

60 |

Total |

5 |

53 |

48 |

106 |

Note: This figure excludes low-risk issues.

Source: VAGO.

Portfolio departments have resolved all extreme issues reported in prior years or they have taken sufficient action to downgrade the risk at the conclusion of the 30 June 2016 financial audits.

2.3 Alpine resorts

In 2013–14, we identified and reported a number of concerning deficiencies in the monitoring, oversight and accountability of finances at Lake Mountain, Mount Baw Baw and Falls Creek alpine resorts. All three resorts had outsourced their finance function in that year but had failed to implement robust oversight and monitoring of this outsourced function.

Figure 2D summarises the significant issues common to these three alpine resorts.

Figure 2D

Issues reported during the 2013–14 audits of the alpine resorts

Issue area |

Lake Mountain |

Mount Baw Baw |

Falls Creek |

|---|---|---|---|

Lack of oversight of outsourcing arrangements |

● | ● | ● |

Poor cash flow management |

● | ||

Noncompliance with legislation |

● | ● | ● |

Internal control environment deficiencies |

● | ● | ● |

Lack of preparedness for financial year-end |

● | ● | ● |

Source: VAGO.

Our 2014–15 financial audits identified significant improvements at Lake Mountain and Mount Baw Baw, where issues we raised have now been addressed.

Falls Creek is in the process of resolving the issues we reported. In particular, this resort has decided to take its finance function back from an outsourced provider, and it is putting in place the systems and controls to make this change from 2017.

3 Department of Education & Training

In last year's Portfolio Departments and Associated Entities: 2014–15 Audit Snapshot report to Parliament, we highlighted that the Department of Education & Training's (DET) financial reporting processes were poor.

We qualified the 2013–14 and 2014–15 financial statements of DET and its predecessor:

- In 2013–14, we disagreed with DET's treatment of a $1.58 billion economic obsolescence adjustment that reduced the carrying value of school buildings. We also determined that a $2.15 billion reclassification of school building impairment was incorrectly recorded as a fair-value adjustment inconsistent with the requirements of the accounting standards.

- In 2014–15, we issued a disclaimer of audit opinion on the department's financial statements because DET was unable to give us sufficient and appropriate evidence about property, plant and equipment transactions and balances, and schools-related transactions and balances, on which we could rely to form our audit opinion.

In this Part, we outline the audit opinion issued on the 2015–16 financial statements, the reasons for the opinion and the progress DET has made to address our previous recommendations.

3.1 Conclusion

DET has worked systematically to address audit concerns and the issues that led to modifications in previous audit opinions. It has improved record-keeping and internal controls. DET has better financial management and governance practices, but it can still make further improvements.

3.2 Audit opinion for 30 June 2016

We issued our audit opinion on 29 September 2016. We were able to give a clear opinion on the transactions and balances as at 30 June 2016.

In this year's opinion, we retained the modification for the 2014–15 comparative balances for schools transactions, but we were satisfied that the comparatives for property, plant and equipment were fairly stated.

During 2015–16, DET strengthened its approach to assurance about schools transactions and balances. However, it was not practical for DET to retrospectively carry out additional assurance work on the 2014–15 school transactions that are used for comparison in the current financial report.

3.2.1 School transactions and balances

DET's financial report consolidates the transactions and balances of 1 544 state government schools which, taken together, are material to DET's financial report.

Schools maintain their own financial records using a common software system from which DET extracts data for the financial report. DET's challenge in this large, devolved system is obtaining sufficient assurance that schools' financial information is complete and accurate.

During 2015–16, DET introduced four assurance activities for school transactions and balances:

- a data analytics tool that compares and contrasts individual school revenue and expense transactions to identify outliers, which DET can then investigate

- audit testing at schools based on a predetermined audit program aimed at assurance gaps that the data analytics tool could not address

- a set of internal audit reviews targeting audit testing at areas and schools considered to be higher risk of not having adequate financial management oversight

- attestations made by all school principals about the compliance, controls, completeness, accuracy and cut-off applied to school transactions and balances.

DET designed its assurance activities, when taken together, to provide it with sufficient and appropriate evidence. We concluded this year that we could rely on most of the components of school's balances, apart from the completeness of school revenue. Evidence that school revenue was complete was neither sufficient nor appropriate.

Schools continue to be paid in cash by some parents for things such as uniforms, before- and after-school care, excursions, camps, supplies, levies and canteens–21 per cent of school receipts are cash.

DET's evidence indicate that schools lack adequate controls over cash-based revenue transactions, and school auditors could not verify that schools recorded all their revenue. The nature of these transactions is such that no audit testing can be done to gain assurance because the lack of controls means that there is no document trail to audit. This inherent risk with cash-based transactions is difficult to overcome.

Despite these problems, we concluded that it is unlikely that any cash-based revenue that is not recorded or is misappropriated would be material to DET's statements.

3.2.2 Property, plant and equipment

Since 2012–13, we have identified and reported to DET significant weaknesses in its records and method of recording property, plant and equipment. The compounding effect of DET not addressing these issues meant that, at 30 June 2015, the asset register was not a reliable record.

During 2015–16, DET has worked to address all matters we raised and has acted on all our recommendations. Specifically, DET has:

- fully revalued all land and buildings, and completely and accurately updated the asset register

- reconciled property, plant and equipment movements and largely substantiated each movement with supporting evidence and schedules

- worked through each component of work-in-progress and cleared out erroneous transactions

- reviewed the transactions expensed as repairs and maintenance to identify those that should be capitalised

- revised asset policies and corrected the accounting treatment of assets held for sale.

As a result of this work, as reported in Note 1U of its financial statements, DET made the following adjustments:

- a decrease of $4.2 million in intangible assets

- a decrease of $99.4 million in property, plant and equipment

- an increase of $61.8 million in accumulated surplus

- a decrease of $165.4 million in the asset revaluation reserve.

DET had a complete and accurate asset register to support the 30 June 2016 financial report. The evidence available in 2015–16 allowed us to conclude that the numbers reported for 30 June 2015 also were not materially misstated. This is a significant achievement and we commend DET on its substantial actions.

In Note 1U of DET's 30 June 2016 financial statements, DET concludes that it was neither practical nor reasonable to restate previous years' financial report amounts because:

- of the large volume of property, plant and equipment transactions

- the problems continued over many years

- of a lack of supporting documents and evidence.

We agree with this assessment and support DET's focus on having the right systems and processes in place so that the register will remain complete and accurate in the future.

3.3 Addressing audit recommendations

After issuing a disclaimer of audit opinion, we wrote a detailed final management letter to DET at the end of the 2014–15 financial audit. That letter listed 17 issues that we rated as being of extreme, high or medium risk. We included recommendations that suggested ways for DET to resolve each problem. Figure 3A includes a summary of these problems in the financial reporting categories.

Figure 3A

Issues in DET's management letter, 2014–15

Risk rating of issue |

||||

|---|---|---|---|---|

Area of issue |

Extreme |

High |

Medium |

Total |

Assets |

1 |

– |

– |

1 |

Expenditure / accounts payable |

– |

1 |

– |

1 |

Financial reporting |

1 |

1 |

– |

2 |

Governance |

1 |

1 |

– |

2 |

Information technology controls |

– |

3 |

– |

3 |

Payroll |

– |

– |

3 |

3 |

Schools |

1 |

4 |

– |

5 |

Total |

4 |

10 |

3 |

17 |

Source: VAGO.

During the 2015–16 reporting cycle, DET has carried out a project to systematically address all of the 17 management letter points. A steering committee oversaw this project. DET's Portfolio Audit and Risk Committee has monitored the project's progress closely.

Of the 17 issues from 2015–16:

- eight have now been resolved and closed

- two remain open but action has been taken and the issue is expected to be resolved within the next 12 months

- five remain open and require DET's attention.

For a further two, we will assess DET's progress as part of our 2016–17 audit.

This shows that DET is serious in addressing longstanding problems that we raised.

3.4 Financial reporting

We reported to Parliament that the financial reporting processes at DET were poor in 2013–14 and 2014–15. The reporting process for 2015–16 was much better, and we no longer consider DET's financial reporting to be poor.

In 2015–16, we received timely financial statements that were supported by schedules and evidence. DET confirmed the quality of the financial information before giving it to us. This improved the timing and the outcome for the 2015–16 financial audit and financial report.

4 Machinery-of-government changes

Machinery-of-government (MOG) changes amend the administrative structure of government agencies. They can be small changes—such as the transfer of a function from one entity to another—or significant changes—such as the creation or discontinuation of a portfolio department.

In December 2014, MOG changes abolished two departments and merged their activities into existing departments. An Order in Council was issued under the Public Administration Act 2004 to enact these changes and rename a number of other portfolio departments, with the changes taking effect from 1 January 2015.

In this Part, we have reviewed how the MOG changes were put in place at the Department of Health & Human Services (DHHS) and the Department of Economic Development, Jobs, Transport & Resources (DEDJTR).

4.1 Conclusion

Both DHHS and DEDJTR were able to implement MOG changes, and they are working toward achieving further efficiencies.

The changes were implemented without a Victorian government framework in place. Since then, one has been developed and it should guide future change.

4.2 Machinery-of-government change management

Large-scale MOG changes can have widespread impacts. They can impact staff and control frameworks, potentially increasing the risk of erroneous transactions, internal control breakdowns, loss of corporate knowledge and fraud. Therefore, strong controls and change processes should be in place to make sure that agencies can implement MOG changes effectively and efficiently.

In 2014–15, there was no framework to guide MOG changes in Victoria. The Australian Public Service Commission (APSC) had issued a framework—Implementing Machinery of Government Changes—and the Queensland Government and United Kingdom's Cabinet had developed similar documents, including specific checklists and better-practice guides, to assist entities in implementing change.

Figure 4A outlines the key elements of a MOG implementation framework, drawing from the APSC, Queensland and United Kingdom guides. We used these better‑practice elements to assess the implementation of MOG changes at DHHS and DEDJTR.

Figure 4A

Key elements of an effective MOG implementation framework

|

Timing |

Key elements |

|---|---|

|

Pre-implementation |

|

|

Implementation |

|

|

Governance |

|

|

Communication |

|

|

Post-implementation |

|

Source: Australian Public Service Commission, Implementing Machinery of Government Changes(2013); UK Cabinet Office, Machinery of Government Guidance (2015); Queensland Audit Office, Managing Machinery of Government Changes (2015); State Services Authority, 'Appendix: Machinery of Government Changes' in Serving as secretary: a guide for public sector leaders, (2012); VAGO.

In May 2016, a committee made up of eight members of the Parliament of Victoria tabled a report, Inquiry into machinery of government changes. This report looked at the cost and effectiveness of MOG changes, and recommended that guidelines be developed to enable clear and consistent reporting of the costs and benefits of MOG changes. We have not duplicated this work in our report.

The Department of Treasury & Finance released a copy of the Victorian public sector operating manual on machinery‑of-government changes, which was prepared by the portfolio departments' chief finance officers and finance deputy secretaries in collaboration.

4.3 Pre-implementation and governance

As part of the implementation and coordination of the 2014 MOG changes, the Department of Premier & Cabinet established a whole-of-government task force. The task force members were senior representatives from the affected portfolio departments who acted as the central point of contact and coordinated the resolution of issues on behalf of their respective portfolio departments.

The purpose of the task force was to:

- oversee the MOG changes and ensure consistent implementation among the portfolio departments and continuity of business and service delivery

- arbitrate any unresolved issues to an agreed outcome

- communicate a clear and consistent message across the Victorian public sector.

In addition to having representatives on the whole-of-government taskforce, both DHHS and DEDJTR established their own steering committees to oversee and take responsibility for implementing MOG changes.

Both departments established clear reporting lines and decision-making authority and documented these in the steering committee terms of reference.

The steering committees were led by departmental deputy secretaries and supported by various subcommittees which focused on identifying implementation issues and making the changes. All subcommittees kept an action log and produced status reports so that the steering committees could monitor progress.

The steering committees had milestones and key deliverables. They considered the risks of not achieving these milestones and put in place mitigation plans where required.

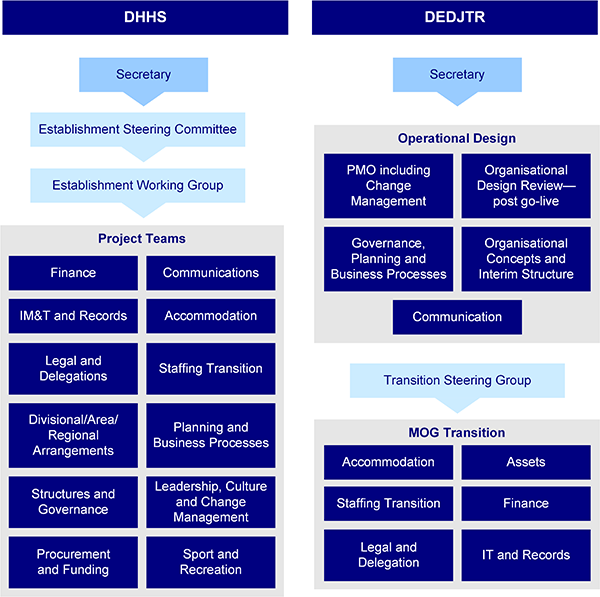

Figure 4B outlines the structure of the steering committees and subcommittees.

Figure 4B

DHHS and DEDJTR steering and subcommittee structure

Note: IM&T = information management and technology; PMO = project management office.

Source: VAGO.

We reviewed the project status reports of both the Establishment Steering Committee and Transition Steering Group. Neither report demonstrated that the groups had reported progress, milestones and achievements to the relevant ministers.

The subcommittees of DHHS and DEDJTR did not have minutes of all meetings held. This made it difficult for us to see the complete trail of decisions and actions. The absence of minutes for all meetings means the records are not complete and not all information is available for post-implementation evaluations.

Source:

4.4 Implementation

To implement the MOG changes, both DHHS and DEDJTR completed project plans that looked at structure, workforce, governance and accommodation.

DHHS undertook a structural review that assessed divisions, duplicate positions, optimal placement of staff and outcomes. Leading on from this review, each director was responsible for implementing restructures within their teams by mapping full-time equivalent staff numbers with business and divisional requirements. All changes were endorsed by the responsible deputy secretary.

DHHS engaged a consultant to review the former Department of Health and Department of Human Services' financial delegations and DHHS's draft delegations against best-practice principles and the practices used in other Victorian portfolio departments. The review examined the actual expenditure patterns of the two former departments to determine business needs, and the results were used as a basis for the new delegations model.

Similarly, DEDJTR engaged a consultant to review its capabilities and functions, and to develop proposed organisational structures for the new department. The consultant reviewed the existing staffing profile and analysed the organisation and functions. This identified potential to integrate functions such as programs, grants, financial management, information technology and human resources. Recommendations from the report were made to the secretary and presented to the executive board.

4.4.1 Implementation delays

While the plans for the steering committee and subcommittees included review and standardisation of delegations and policies, we found that duplicate financial policies existed at both DHHS and DEDJTR, which may mean that staff are using inconsistent practices, policies and processes.

DEDJTR is currently operating two separate general ledgers, with integration not expected to occur until July 2017. This increases the time, cost, complexity and risk for producing accurate and complete financial information. DEDJTR is also currently operating under a number of separate IT systems and processes.

Amalgamating the systems used by the former Department of Health and Department of Human Services for managing service agreements did not occur until mid-2016. As a consequence, manual amalgamation and reconciliation of information was required, increasing the risk of errors.

DHHS did not complete and endorse a consolidated strategic risk profile until May 2016. As a result, the new department did not have a shared understanding of risk for the first 18 months of operation.

4.5 Communication

Ensuring adequate communication to staff about MOG changes and implementation processes increases staff engagement and confidence. This in turn helps to develop a transparent culture within the new department.

Departmental secretaries and deputy secretaries at DHHS and DEDJTR kept staff informed throughout the MOG implementation process. They also encouraged staff participation and input, by emailing detailed information on governance, structure and procedural progress. Both DHHS and DEDJTR updated staff on MOG changes through staff bulletins, intranet pages, and team and divisional briefings.

DEDJTR created a MOG transition information section on its intranet as a communication tool. This section included organisational change reports, projects for business and strategic transition planning, time lines, frequently asked questions and answers, and impacts of the transition to the new structure.

DHHS established a MOG communication plan that outlined the communication approach, target audiences and key staff messages. As part of this communication plan, it produced a question-and-answer fact sheet and regular establishment updates for staff, outlining key information about the new department and general information about staff impacts and changes to processes and procedures.

Staff at DHHS were invited to be involved in the MOG change process through a focus group called 'Creating our culture together'. The aim of these sessions was to promote staff discussion and involvement in setting the new department values.

4.6 Post-implementation

A post-implementation review should be the final action of a MOG steering committee, to ensure that all required change has been made and to document any key lessons for the next time a significant change program occurs.

DHHS and DEDJTR have not conducted any formal post-implementation evaluations specifically about the MOG change process.

DHHS completed an Establishment Project Closure report that outlined the project governance, including responsibilities, the structure and members of the steering and working groups, the key projects that had been delivered, and any outstanding project activities passed into business units for completion. It also had a final project status report.

DEDJTR undertook an internal audit on its internal control framework in May 2016. The results of the report recommended that DEDJTR adopt a uniform approach for its financial systems, processes and procedures.

Appendix A Audit Act 1994 section 16—submissions and comments

We have consulted with named portfolio departments and agencies, and we considered their views when reaching our audit conclusions. As required by section 16(3) of the Audit Act 1994, we gave relevant extracts of this report to those agencies and asked for their submissions or comments.

Responsibility for the accuracy, fairness and balance of those comments rests solely with the agency head.

Full responses from the Department of Treasury & Finance and the Department of Education & Training are included in this Appendix.

RESPONSE provided by the Secretary, Department of Treasury & Finance

RESPONSE provided by the Secretary, Department of Education & Training

RESPONSE provided by the Secretary, Department of Education & Training – continued

Appendix B. Audit opinions issued

Figure B1 shows the list of portfolio departments and associated entities named in this report and illustrates the outcome of their audit opinions.

Figure B1

Audit opinions issued by portfolio department

Entity |

Clear audit opinion issued |

Auditor‑General's report signed |

|---|---|---|

Department of Economic Development, Jobs, Transport & Resources |

Y |

2 Sep 16 |

Agriculture Victoria Services Pty Ltd |

Y |

25 Aug 16 |

Australian Centre for the Moving Image |

Y |

2 Sep 16 |

Australian Grand Prix Corporation |

Y |

6 Sep 16 |

Australian Synchrotron Holding Company |

Not signed yet |

|

Dairy Food Safety Victoria |

Y |

24 Aug 16 |

Docklands Studios Melbourne Pty Ltd |

Y |

30 Aug 16 |

Emerald Tourist Railway Board |

Y |

2 Sep 16 |

Energy Safe Victoria |

Y |

31 Aug 16 |

Fed Square Pty Ltd |

Y |

8 Sep 16 |

Film Victoria |

Y |

25 Aug 16 |

Game Management Authority |

Y |

28 Oct 16 |

Geelong Performing Arts Centre Trust |

Y |

29 Aug 16 |

Greater Sunraysia Pest Free Area Industry Development Committee |

Not signed yet |

|

Library Board of Victoria |

Y |

29 Aug 16 |

Melbourne and Olympic Parks Trust |

Y |

2 Sep 16 |

Melbourne Convention and Exhibition Trust |

Y |

25 Aug 16 |

Melbourne Cricket Ground Trust |

Y |

30 Jun 16 |

Melbourne Market Authority |

Y |

8 Sep 16 |

Melbourne Port Lessor Pty Ltd |

Not signed yet |

|

Melbourne Recital Centre |

Y |

2 Sep 16 |

Murray Valley Wine Grape Industry Development Committee |

Y |

31 Aug 16 |

Museums Board of Victoria |

Y |

31 Aug 16 |

National Gallery of Victoria, Council of Trustees |

Y |

25 Aug 16 |

Northern Victorian Fresh Tomato Industry Development Committee |

Not signed yet |

|

Phytogene Pty Ltd |

Y |

29 Aug 16 |

Port of Hastings Development Authority |

Y |

31 Aug 16 |

Port of Melbourne Corporation |

Y |

26 Oct 16 |

Port of Melbourne Operations Pty Ltd |

Not signed yet |

|

PrimeSafe |

Y |

31 Aug 16 |

Public Transport Development Authority |

Y |

23 Sep 16 |

Recreational Fishing Licence Trust Account |

Y (EOM) |

30 Aug 16 |

Roads Corporation |

Y |

6 Sep 16 |

Rolling Stock (Victoria VL) Pty Ltd |

Y |

24 Aug 16 |

Rolling Stock (VL 1) Pty Ltd |

Y |

24 Aug 16 |

Rolling Stock (VL 2) Pty Ltd |

Y |

24 Aug 16 |

Rolling Stock (VL 3) Pty Ltd |

Y |

24 Aug 16 |

Rolling Stock Holdings (Victoria) Pty Ltd |

Y |

24 Aug 16 |

State Library of Victoria Foundation |

Y (EOM) |

31 Aug 16 |

Taxi Services Commission |

Y |

26 Sep 16 |

Tourism Victoria |

Y (EOM) |

18 Oct 16 |

Urban Renewal Authority Victoria (Places Victoria) |

Y |

19 Aug 16 |

V/Line Corporation |

Y |

24 Aug 16 |

V/Line Pty Ltd |

Y |

24 Aug 16 |

Veterinary Practitioners Registration Board of Victoria |

Y |

8 Sep 16 |

VicForests |

Y |

3 Oct 16 |

Victorian Arts Centre Trust |

Y |

29 Aug 16 |

Victorian Major Events Company Limited |

Y (EOM) |

12 Sep 16 |

Victorian Rail Track |

Y |

15 Sep 16 |

Victorian Regional Channels Authority |

Y |

1 Sep 16 |

Victorian Strawberry Industry Development Committee |

Y |

8 Sep 16 |

Department of Education & Training |

N |

29 Sep 16 |

Adult Multicultural Education Service Australia |

Y |

23 Aug 16 |

Adult, Community and Further Education Board |

Y |

26 Aug 16 |

Victorian Curriculum and Assessment Authority |

Y |

5 Sep 16 |

Victorian Institute of Teaching |

Y |

19 Aug 16 |

Victorian Registration and Qualifications Authority |

Y |

26 Aug 16 |

VET Development Centre Ltd |

Y |

23 Mar 16 |

Department of Environment, Land, Water & Planning |

Y |

16 Sep 16 |

Alpine Resorts Co-ordinating Council |

Y |

6 Oct 16 |

Architects' Registration Board of Victoria |

Y |

22 Sep 16 |

Barwon South West Waste and Resource Recovery Group |

Y |

23 Sep 16 |

Corangamite Catchment Management Authority |

Y |

20 Sep 16 |

Dhelkunya Dja Land Management Board |

Y |

27 Sep 16 |

East Gippsland Catchment Management Authority |

Y |

31 Aug 16 |

Environment Protection Authority |

Y |

29 Aug 16 |

Falls Creek Alpine Resort Management Board |

Y |

29 Apr 16 |

Gippsland Waste and Resource Recovery Group |

Y |

29 Sep 16 |

Glenelg Hopkins Catchment Management Authority |

Y |

22 Aug 16 |

Goulburn Broken Catchment Management Authority |

Y |

30 Aug 16 |

Goulburn Valley Waste and Resource Recovery Group |

Y |

15 Sep 16 |

Grampians Central Waste and Resource Recovery Group |

Y |

22 Sep 16 |

Gunaikurnai Traditional Owner Land Management |

Y |

26 Sep 16 |

Heritage Council of Victoria |

Y |

21 Sep 16 |

Lake Mountain Alpine Resort Management Board |

Y (EOM) |

14 Jan 16 |

Loddon Mallee Waste and Resource Recovery Group |

Y |

30 Aug 16 |

Mallee Catchment Management Authority |

Y |

29 Aug 16 |

MAPS Group Limited |

Not signed yet |

|

Metropolitan Planning Authority |

Y |

22 Sep 16 |

Metropolitan Waste and Resource Recovery Group |

Y |

22 Sep 16 |

Mount Baw Baw Alpine Resort Management Board |

Y (EOM) |

22 Jan 16 |

Mount Buller and Mount Stirling Alpine Resort Management Board |

Y |

22 Dec 15 |

Mount Hotham Alpine Resort Management Board |

Y |

18 Dec 15 |

North Central Catchment Management Authority |

Y |

2 Sep 16 |

North East Catchment Management Authority |

Y |

24 Aug 16 |

North East Waste and Resource Recovery Group |

Y |

15 Sep 16 |

Office for the Commissioner for Environmental Sustainability |

Y |

23 Sep 16 |

Parks Victoria |

Y |

18 Aug 16 |

Phillip Island Nature Parks |

Y |

5 Sep 16 |

Port Phillip and Westernport Catchment Management Authority |

Y |

18 Aug 16 |

Royal Botanic Gardens Board |

Y |

22 Aug 16 |

Smart Water Fund |

Not signed yet |

|

Surveyors Registration Board of Victoria |

Y |

29 Sep 16 |

Sustainability Victoria |

Y |

29 Aug 16 |

Trust for Nature (Victoria) |

Y |

14 Sep 16 |

Victorian Building Authority |

Y |

12 Sep 16 |

Victorian Environmental Water Holder |

Y |

22 Sep 16 |

Victorian Plantations Corporation |

Y |

18 Oct 16 |

West Gippsland Catchment Management Authority |

Y |

22 Aug 16 |

Wimmera Catchment Management Authority |

Y |

16 Aug 16 |

Yorta Yorta Traditional Owner Land Management Board |

Y |

17 Oct 16 |

Zoological Parks and Gardens Board |

Y |

6 Sep 16 |

Department of Health & Human Services |

Y |

23 Sep 16 |

Ambulance Victoria |

Y |

12 Aug 16 |

Ballarat General Cemeteries Trust |

Y |

2 Sep 16 |

Bendigo Cemeteries Trust |

Y |

24 Aug 16 |

Geelong Cemeteries Trust |

Y |

24 Aug 16 |

Gippsland Health Alliance |

Y |

30 Aug 16 |

Grampians Rural Health Alliance |

Y |

25 Aug 16 |

Health Purchasing Victoria |

Y |

23 Aug 16 |

Hume Rural Health Alliance |

Y |

22 Sep 16 |

LMHA Network Limited |

Not signed yet |

|

Loddon Mallee Rural Health Alliance |

Y |

28 Jul 16 |

Mildura Cemetery Trust |

Y |

9 Sep 16 |

Southern Metropolitan Cemeteries Trust |

Y |

4 Aug 16 |

South West Alliance of Rural Health |

Y |

26 Sep 16 |

State Sport Centres Trust |

Y |

26 Sep 16 |

The Greater Metropolitan Cemeteries Trust |

Y |

24 Aug 16 |

Victoria Comprehensive Cancer Centre |

Y |

19 Aug 16 |

Victorian Assisted Reproductive Treatment Authority |

Y |

9 Sep 16 |

Victorian Comprehensive Cancer Centre Ltd |

Y |

19 Aug 16 |

Victorian Health Promotion Foundation |

Y |

25 Aug 16 |

Victorian Institute of Forensic Mental Health |

Y |

13 Sep 16 |

Victorian Institute of Sport Limited |

Y |

8 Sep 16 |

Victorian Institute of Sport Trust |

Y |

8 Sep 16 |

Victorian Pharmacy Authority |

Y |

29 Aug 16 |

Victorian State Pool Account |

Y (EOM) |

4 Aug 16 |

Department of Justice & Regulation |

Y |

11 Oct 16 |

Country Fire Authority |

Y |

21 Oct 16 |

Court Services Victoria |

Y |

6 Oct 16 |

Emergency Services Telecommunications Authority |

Y |

30 Aug 16 |

Greyhound Racing Victoria |

Y |

1 Sep 16 |

Harness Racing Victoria |

Y |

16 Sep 16 |

HRV Management Limited |

Y |

16 Sep 16 |

Judicial College of Victoria |

Y |

11 Oct 16 |

Legal Practitioners Liability Committee |

Y |

9 Sep 16 |

Legal Services Board |

Y |

19 Aug 16 |

Legal Services Commissioner |

Y |

19 Aug 16 |

Melton Entertainment Trust |

Y |

16 Sep 16 |

Metropolitan Fire and Emergency Services Board |

Y |

19 Aug 16 |

Office of Public Prosecutions |

Y |

18 Oct 16 |

Professional Standards Council of Victoria |

Y |

29 Sep 16 |

Residential Tenancies Bond Authority |

Y |

11 Oct 16 |

Sentencing Advisory Council |

Y |

6 Oct 16 |

VFM Emerging Markets Trust |

Y (EOM) |

15 Sep 16 |

VFM Global Small Companies Trust |

Y (EOM) |

15 Sep 16 |

VFMC Balanced Fund |

Y (EOM) |

15 Sep 16 |

VFMC Capital Stable Fund |

Y (EOM) |

15 Sep 16 |

VFMC Cash Trust |

Y (EOM) |

15 Sep 16 |

VFMC Enhanced Cash Trust |

Y (EOM) |

15 Sep 16 |

VFMC Equity Trust 1 |

Y (EOM) |

15 Sep 16 |

VFMC Equity Trust 2 |

Y (EOM) |

15 Sep 16 |

VFMC ESSS Private Equity Trust 2004 |

Y (EOM) |

15 Sep 16 |

VFMC ESSS Private Equity Trust 2006 |

Y (EOM) |

15 Sep 16 |

VFMC ESSS Private Equity Trust 2007 |

Y (EOM) |

15 Sep 16 |

VFMC Fixed Income Trust |

Y (EOM) |

15 Sep 16 |

VFMC Growth Fund |

Y (EOM) |

15 Sep 16 |

VFMC Inflation Linked Bond Trust |

Y (EOM) |

15 Sep 16 |

VFMC Insurance Strategies Trust |

Y (EOM) |

15 Sep 16 |

VFMC International Equity Trust 1 |

Y (EOM) |

15 Sep 16 |

VFMC International Equity Trust 2 |

Y (EOM) |

15 Sep 16 |

VFMC Investment Trust I |

Y (EOM) |

15 Sep 16 |

VFMC Investment Trust II |

Not signed yet |

|

VFMC Investment Trust IV |

Not signed yet |

|

VFMC Opportunistic Strategies Trust |

Not signed yet |

|

VFMC Yield Optimised Dividend Accumulator Trust |

Y (EOM) |

15 Sep 16 |

Victoria Police |

Y |

29 Sep 16 |

Victoria State Emergency Service Authority |

Y |

21 Sep 16 |

Victorian Commission for Gambling and Liquor Regulation |

Y |

5 Oct 16 |

Victorian Equal Opportunity and Human Rights Commission |

Y |

11 Oct 16 |

Victorian Institute of Forensic Medicine |

Y |

10 Oct 16 |

Victorian Law Reforms Commission |

Y |

29 Sep 16 |

Victorian Legal Aid |

Y |

22 Aug 16 |

Victorian Responsible Gambling Foundation |

Y |

29 Sep 16 |

Victorian Traditional Owners Fund Limited |

Not signed yet |

|

Victorian Traditional Owners Trust |

Not signed yet |

|

Department of Premier & Cabinet |

Y |

12 Sept 16 |

Accident Compensation Conciliation Service |

Y |

16 Aug 16 |

Independent Broad-based Anti-corruption Commission |

Y |

5 Sep 16 |

Infrastructure Victoria |

Y |

26 Sep 16 |

Commissioner for Privacy and Data Protection |

Y |

21 Sep 16 |

Office of the Ombudsman |

Y |

16 Sep 16 |

Queen Victoria Women's Centre Trust |

Y |

18 Aug 16 |

Shrine of Remembrance Trustees |

Y |

2 Sep 16 |

Victorian Electoral Commission |

Y |

30 Aug 16 |

Victorian Inspectorate |

Y |

26 Aug 16 |

Victorian Public Sector Commission |

Y |

23 Sep 16 |

Victorian Veterans Council |

Y |

27 Sep 16 |

Department of Treasury & Finance |

N |

10 Oct 16 |

CenlTex |

Y |

28 Oct 16 |

Emergency Services Superannuation Board |

Y |

29 Aug 16 |

Emergency Services Superannuation Scheme |

Y |

29 Aug 16 |

Essential Services Commission |

Y |

21 Sep 16 |

InveST Funds |

Y |

29 Aug 16 |

Residential Independence Pty Ltd |

Y |

21 Sep 16 |

Residential Independence Trust |

Y |

21 Sep 16 |

Residents' Trust Fund |

Y (EOM) |

29 Aug 16 |

Rural Finance Corporation of Victoria |

Y (EOM) |

27 Sep 16 |

State Electricity Commission of Victoria |

Y (EOM) |

16 Sep 16 |

State Trustees Limited Australia Foundation |

Y (EOM) |

29 Aug 16 |

State Trustees Limited Australia Foundation Open Fund |

Y (EOM) |

29 Aug 16 |

State Trustees Common Funds |

Y |

29 Aug 16 |

State Trustees Limited |

Y |

26 Aug 16 |

STL Financial Services Limited |

Y |

29 Aug 16 |

Transport Accident Commission |

Y |

26 Sep 16 |

Treasury Corporation of Victoria |

Y |

18 Aug 16 |

Victorian Funds Management Corporation |

Y |

24 Aug 16 |

VITS Languagelink |

Y |

16 Sep 16 |

Victorian Managed Insurance Authority |

Y |

31 Aug 16 |

Victorian WorkCover Authority |

Y |

31 Aug 16 |

Audits by invitation |

|

|

Australian Health Practitioner Regulation Agency |

Y |

30 Aug 16 |

Health Professional Councils Authority |

Y (EOM) |

28 Sep 16 |

Senior Master of the Supreme Court |

Y (EOM) |

26 Aug 16 |

Parliament of Victoria |

Y |

23 Aug 16 |

Note: EOM = emphasis of matter.

Source: VAGO.

Appendix C. Management letter risk ratings

Figure C1 shows the risk ratings applied to the points we raise in management letters during an audit.

Figure C1

Risk definitions applied to issues reported in audit management letters

Rating |

Definition |

Management action required |

|---|---|---|

Extreme |

The issue represents:

|

Requires immediate management intervention with a detailed action plan to be implemented within one month. Requires executive management to correct the material misstatement in the financial report as a matter of urgency to avoid a modified audit opinion. |

High |

The issue represents:

|

Requires prompt management intervention with a detailed action plan implemented within two months. Requires executive management to correct the material misstatement in the financial report to avoid a modified audit opinion. |

Medium |

The issue represents:

|

Requires management intervention with a detailed action plan implemented within three to six months. |

Low |

The issue represents:

|

Requires management intervention with a detailed action plan implemented within six to 12 months. |

Source: VAGO.

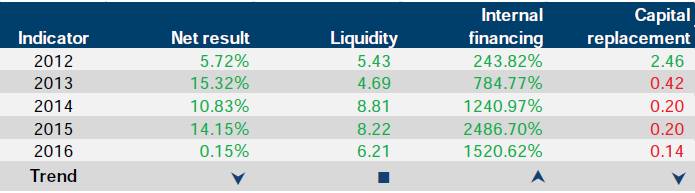

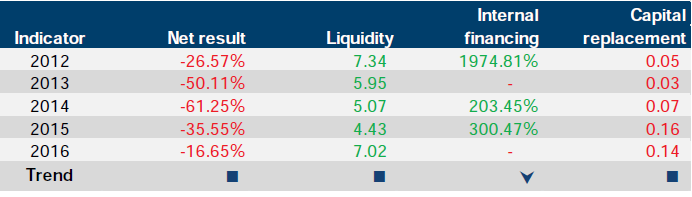

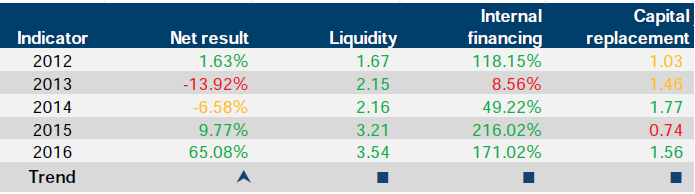

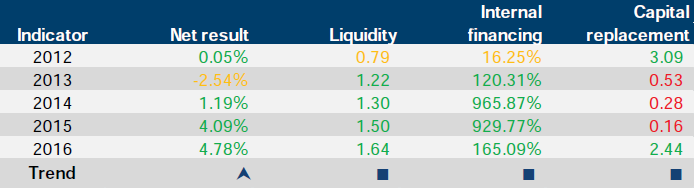

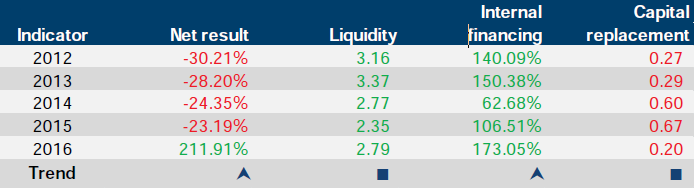

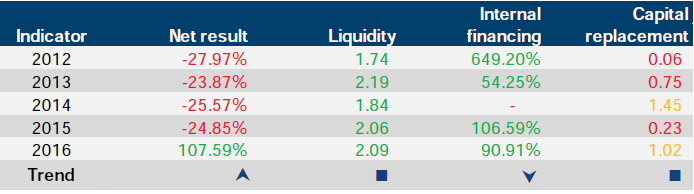

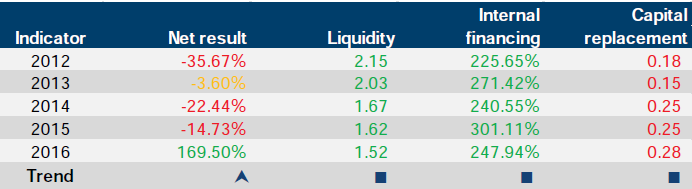

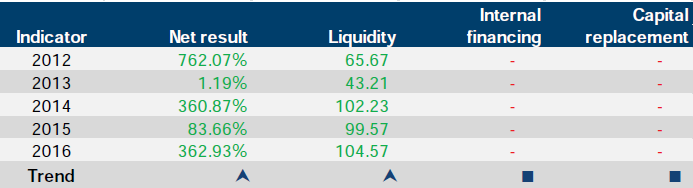

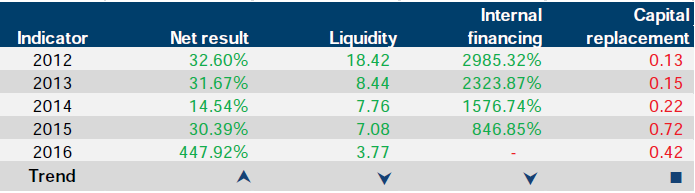

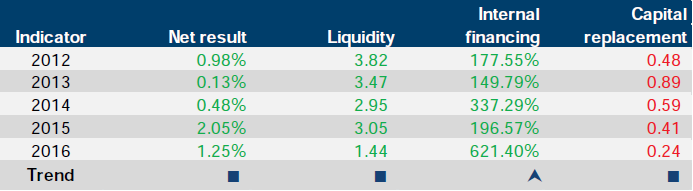

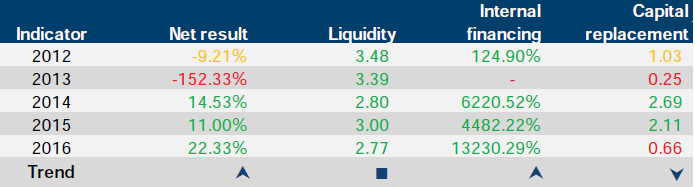

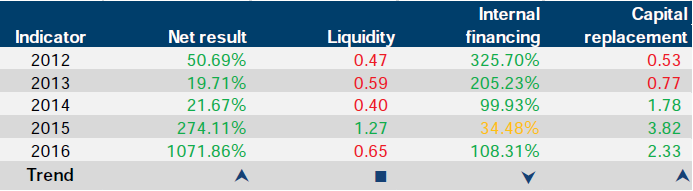

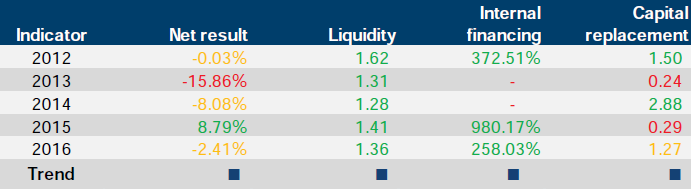

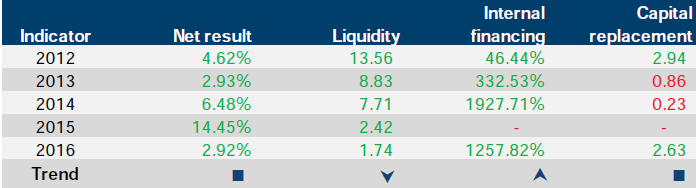

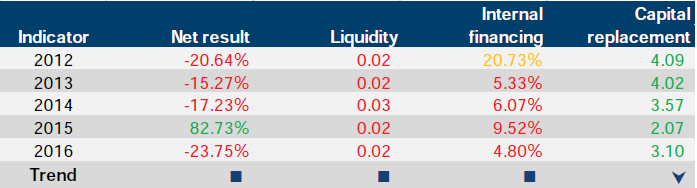

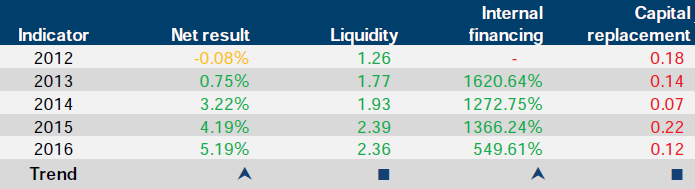

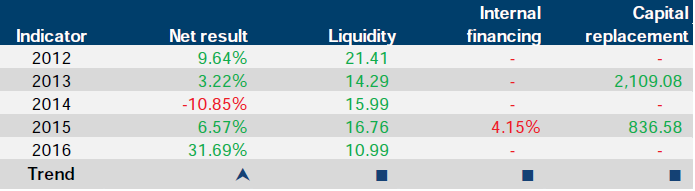

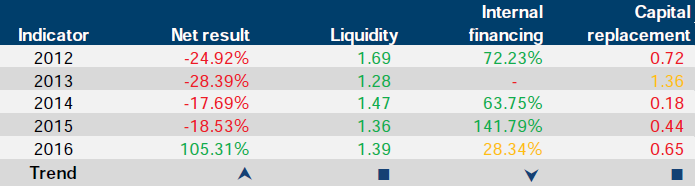

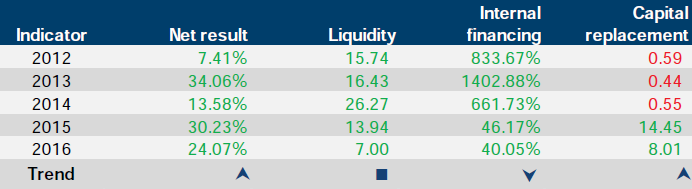

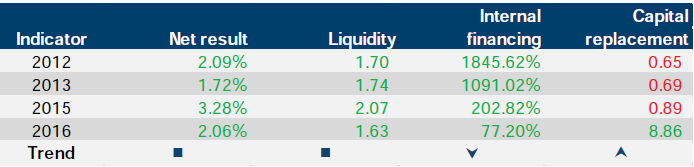

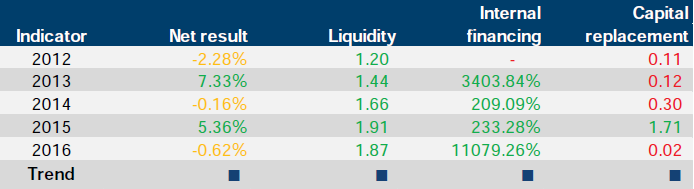

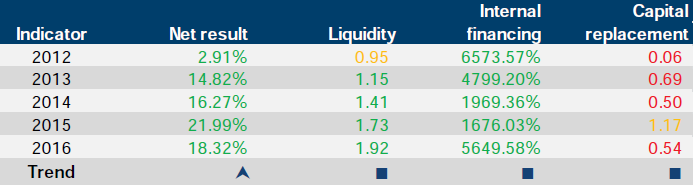

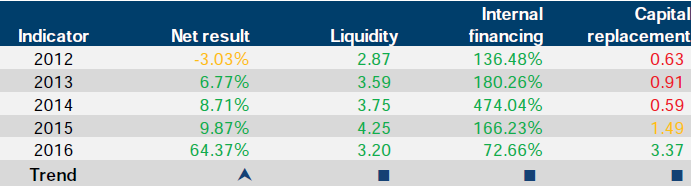

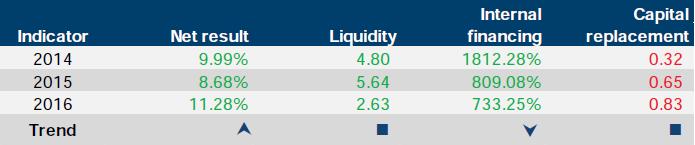

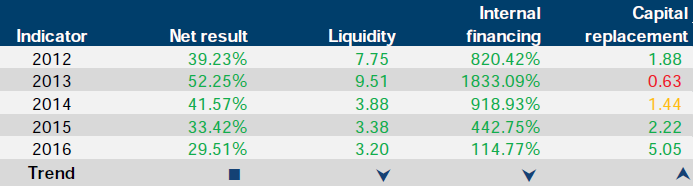

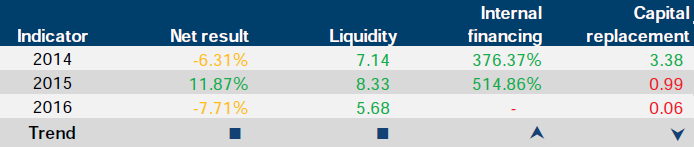

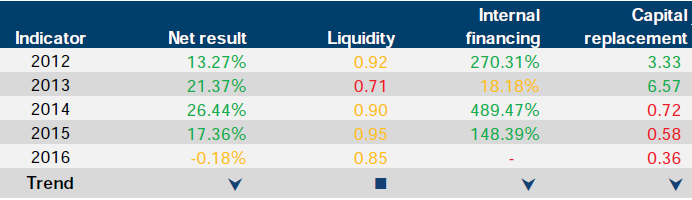

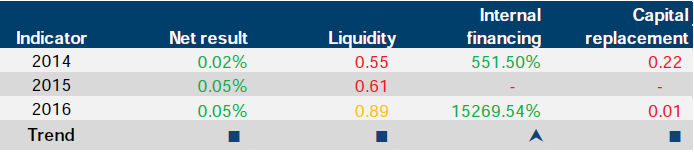

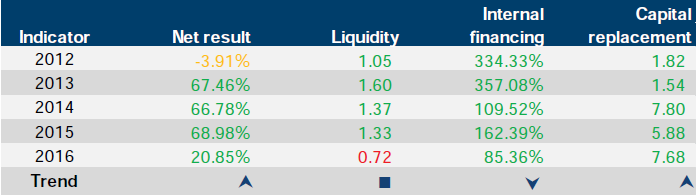

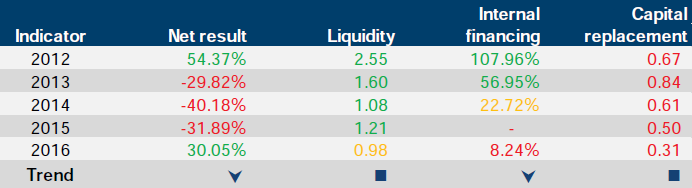

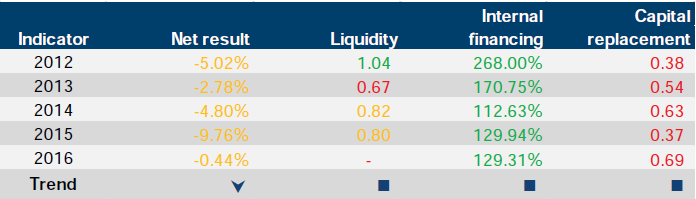

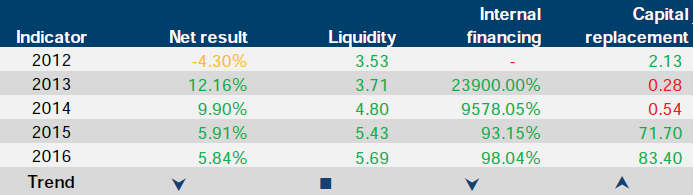

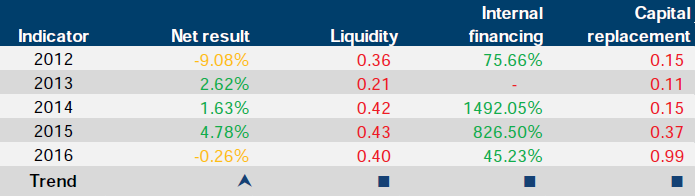

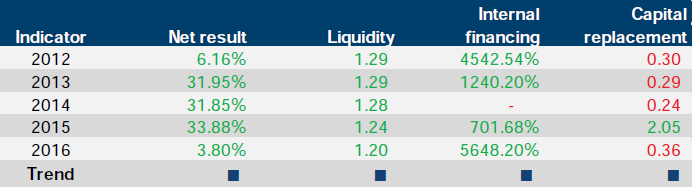

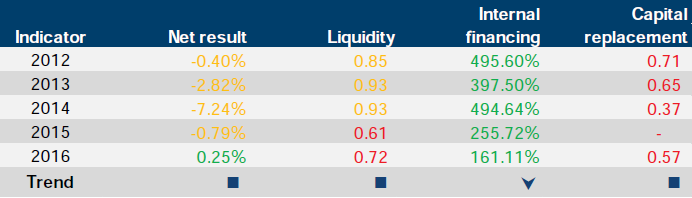

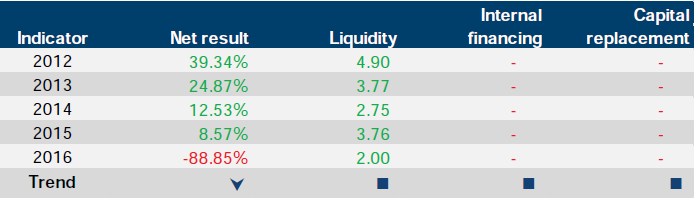

Appendix D. Financial sustainability risk indicators

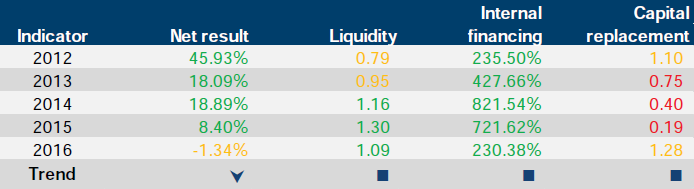

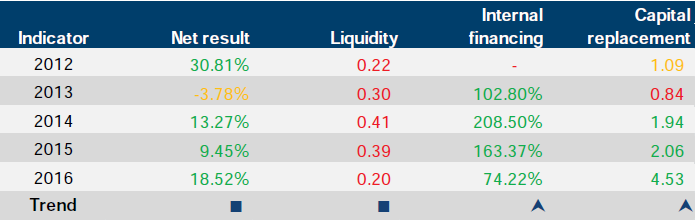

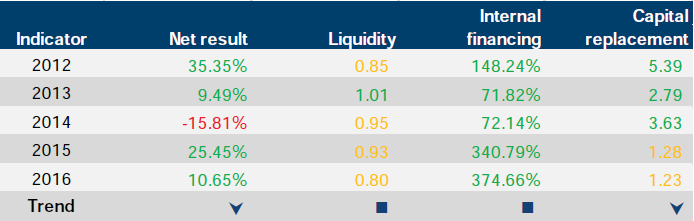

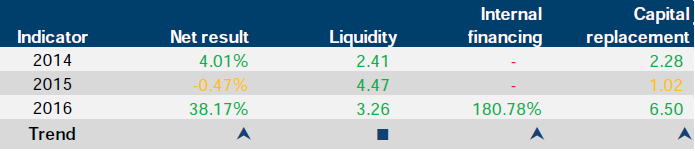

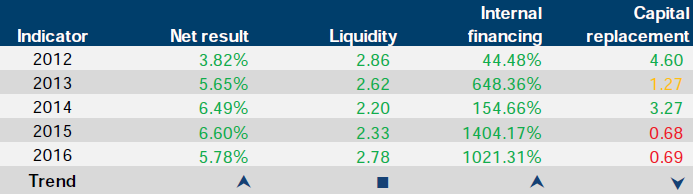

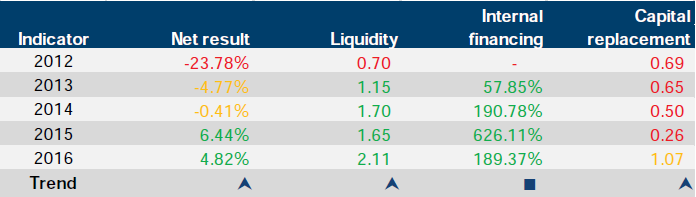

Figure D1 shows the financial sustainability indicators for self-funded entities. These indicators should be considered collectively, and are more useful when assessed over time as part of a trend analysis.

Figure D1

Financial sustainability risk indicators

|

Indicator |

Formula |

Description |

|---|---|---|

|

Net result (%) |

Net result / Total revenue |

A positive result indicates a surplus, and the larger the percentage, the stronger the result. A negative result indicates a deficit. Operating deficits cannot be sustained in the long term. Net result and total revenue is obtained from the comprehensive operating statement. |

|

Liquidity (ratio) |

Current assets / Current liabilities |

This measures the ability to pay existing liabilities in the next 12 months. A ratio of one or more means there are more cash and liquid assets than short-term liabilities. |

|

Internal financing (%) |

Net operating cash flow / Net capital expenditure |

This measures the ability of an entity to finance capital works from generated cash flow. The higher the percentage, the greater the ability for the entity to finance capital works from their own funds. Net operating cash flows and net capital expenditure are obtained from the cash flow statement. |

|

Capital replacement (ratio) |

Cash outflows for property, plant and equipment / Depreciation |

Comparison of the rate of spending on infrastructure with its depreciation. Ratios higher than 1:1 indicate that spending is faster than the depreciating rate. This is a long-term indicator, as capital expenditure can be deferred in the short term if there are insufficient funds available from operations, and borrowing is not an option. Cash outflows for infrastructure are taken from the cash flow statement. Depreciation is taken from the comprehensive operating statement. |

Source: VAGO.

Financial sustainability risk assessment criteria

The financial sustainability risk of each self-funded entity has been assessed using the criteria outlined in Figure D2.

Figure D2

Financial sustainability risk indicators—risk assessment criteria

|

Risk |

Net result |

Liquidity |

Internal financing |

Capital replacement |

|---|---|---|---|---|

|

High |

Negative 10% or less |

Less than 0.75 |

Less than 10% |

Less than 1.0 |

|

Medium |

Negative 10%–0% |

0.75–1.0 |

10–35% |

1.0–1.5 |

|

Low |

More than 0% |

More than 1.0 |

More than 35% |

More than 1.5 |

Source: VAGO.

Financial sustainability risk analysis results

The financial sustainability risk for each self-funded entity, for each of the years 2012 to 2016 are shown in Figures D3 to D53.

The following trend analysis has been applied to the results for each self-funded entity:

Department of Economic Development, Jobs, Transport & Resources

Figure D3

Financial sustainability risk indicator results for Agriculture Victoria Services Pty Ltd at 30 June

Source: VAGO.

Figure D4

Financial sustainability risk indicator results for Dairy Food Safety Victoria at 30 June

Source: VAGO.

Figure D5

Financial sustainability risk indicator results for Docklands Studios Melbourne Pty Ltd at 30 June

Source: VAGO.

Figure D6

Financial sustainability risk indicator results for Emerald Tourist Railway Board at 30 June

Source: VAGO.

Figure D7

Financial sustainability risk indicator results for Energy Safe Victoria at 30 June

Source: VAGO.

Figure D8

Financial sustainability risk indicator results for Fed Square Pty Ltd at 30 June

Source: VAGO.

Figure D9

Financial sustainability risk indicator results for Geelong Performing Arts Centre Trust at 30 June

Source: VAGO.

Figure D10

Financial sustainability risk indicator results for Melbourne and Olympic Parks Trust at 30 June

Source: VAGO.

Figure D11

Financial sustainability risk indicator results for Melbourne Convention and Exhibition Trust at 30 June

Source: VAGO.

Figure D12

Financial sustainability risk indicator results for Melbourne Cricket Ground Trust at 30 June

Source: VAGO.

Figure D13

Financial sustainability risk indicator results for Melbourne Market Authority at 30 June

Source: VAGO.

Figure D14

Financial sustainability risk indicator results for Melbourne Recital Centre at 30 June

Source: VAGO.

Figure D15

Financial sustainability risk indicator results for Murray Valley Wine Grape Industry Development Committee at 30 June

Source: VAGO.

Figure D16

Financial sustainability risk indicator results for Urban Renewal Authority Victoria (Places Victoria) at 30 June

Source: VAGO.

Figure D17

Financial sustainability risk indicator results for Port of Melbourne Corporation at 30 June

Source: VAGO.

Figure D18

Financial sustainability risk indicator results for PrimeSafe at 30 June

Source: VAGO.

Figure D19

Financial sustainability risk indicator results for Veterinary Practitioners Registration Board of Victoria at 30 June

Source: VAGO.

Figure D20

Financial sustainability risk indicator results for Vic Rail Track at 30 June

Source: VAGO.

Figure D21

Financial sustainability risk indicator results for VicForests at 30 June

Source: VAGO.

Figure D22

Financial sustainability risk indicator results for Victorian Strawberry Industry Development Committee at 30 June

Source: VAGO.

Figure D23

Financial sustainability risk indicator results for Victorian Arts Centre Trust at 30 June

Source: VAGO.

Figure D24

Financial sustainability risk indicator results for Victorian Regional Channels Authority at 30 June

Source: VAGO.

Department of Education & Training

Figure D25

Financial sustainability risk indicator results for Adult Multicultural Education Services Australia at 30 June

Note: The 2012 and 2013 years represent a 12-month 31 December year end, with 2015 and 2016 representing an 18-month and 12-month 30 June year end respectively.

Figure D26

Financial sustainability risk indicator results for Victorian Institute of Teaching at 30 June

Source: VAGO.

Department of Environment, Land, Water & Planning

Figure D27

Financial sustainability risk indicator results for Architects Registration Board of Victoria at 30 June

Source: VAGO.

Figure D28

Financial sustainability risk indicator results for Heritage Council of Victoria at 30 June

Source: VAGO.

Figure D29

Financial sustainability risk indicator results for Phillip Island Nature Parks at 30 June

Source: VAGO.

Figure D30

Financial sustainability risk indicator results for Victorian Building Authority at 30 June

Note: The Victorian Building Authority was not mandated for audit by the VAGO until the 2014 financial year.

Source: VAGO.

Figure D31

Financial sustainability risk indicator results for Zoological Parks and Gardens Board at 30 June

Source: VAGO.

Department of Health & Human Services

Figure D32

Financial sustainability risk indicator results for Ballarat General Cemeteries Trust at 30 June

Source: VAGO.

Figure D33

Financial sustainability risk indicator results for Bendigo Cemeteries Trust at 30 June

Source: VAGO.

Figure D34

Financial sustainability risk indicator results for Geelong Cemeteries Trust at 30 June

Source: VAGO.

Figure D35

Financial sustainability risk indicator results for Gippsland Health Alliance at 30 June

Note: The Gippsland Health Alliance was not mandated for audit by VAGO until the 2014 financial year.

Source: VAGO.

Figure D36

Financial sustainability risk indicator results for Grampians Rural Health Alliance at 30 June

Note: The Grampians Rural Health Alliance was not mandated for audit by VAGO until the 2014 financial year.

Source: VAGO.

Figure D37

Financial sustainability risk indicator results for The Greater Metropolitan Cemeteries Trust at 30 June

Source: VAGO.

Figure D38

Financial sustainability risk indicator results for Hume Rural Health Alliance at 30 June

Note: The Hume Rural Health Alliance was not mandated for audit by VAGO until the 2014 financial year.

Source: VAGO.

Figure D39

Financial sustainability risk indicator results for Loddon Mallee Rural Health Alliance at 30 June

Note: The Loddon Mallee Rural Health Alliance was not mandated for audit by VAGO until the 2014 financial year.

Source: VAGO.

Figure D40

Financial sustainability risk indicator results for Mildura Cemetery Trust at 30 June

Source: VAGO.

Figure D41

Financial sustainability risk indicator results for South West Alliance of Rural Health at 30 June

Note: The South West Alliance of Rural Health was not mandated for audit by VAGO until the 2014 financial year.

Source: VAGO.

Figure D42

Financial sustainability risk indicator results for Southern Metropolitan Cemeteries Trust at 30 June

Source: VAGO.

Figure D43

Financial sustainability risk indicator results for State Sport Centres Trust at 30 June

Source: VAGO.

Figure D44

Financial sustainability risk indicator results for Victorian Pharmacy Authority at 30 June

Source: VAGO.

Department of Justice & Regulation

Figure D45

Financial sustainability risk indicator results for Emergency Services Telecommunications Authority at 30 June

Source: VAGO.

Figure D46

Financial sustainability risk indicator results for Greyhound Racing Victoria at 30 June

Source: VAGO.

Figure D47

Financial sustainability risk indicator results for Harness Racing Victoria at 30 June

Source: VAGO.

Figure D48

Financial sustainability risk indicator results for Legal Services Board at 30 June

Source: VAGO.

Figure D49

Financial sustainability risk indicator results for Melton Entertainment Trust at 30 June

Source: VAGO.

Figure D50

Financial sustainability risk indicator results for Professional Standards Council of Victoria at 30 June

Source: VAGO.

Figure D51

Financial sustainability risk indicator results for Victorian Traditional Owners Trust at 30 June

Note: At the date of publication, the 30 June 2016 financial statements had not been signed.

Source: VAGO.

Figure D52

Financial sustainability risk indicator results for VITS Languagelink at 30 June

Source: VAGO.

Department of Treasury & Finance

Figure D53

Financial sustainability risk indicator results for CenITex at 30 June

Source: VAGO.

Appendix E. Glossary

Accountability

Responsibility of public entities to achieve their objectives in reliability of financial reporting, effectiveness and efficiency of operations, compliance with applicable laws, and reporting to interested parties.

Adverse opinion

An audit opinion expressed if the auditor has sufficient appropriate audit evidence and concludes that misstatements, individually and in aggregate, are both material and pervasive in the financial report.

Asset

An item or resource controlled by an entity that will be used to generate future economic benefits.

See also current asset, intangible asset and non-current asset.

Audit Act 1994

Victorian legislation establishing the Auditor-General's operating powers and responsibilities and detailing the nature and scope of audits that the Auditor-General may carry out.

Audit opinion

A written expression, within a specified framework, indicating the auditor's overall conclusion about a financial (or performance) report based on audit evidence.

See also modified opinion and unmodified opinion.

Capital expenditure

Money an entity spends on:

- new physical assets, including buildings, infrastructure, plant and equipment

- renewing existing physical assets to extend the service potential or life of the asset.

Corporations Act 2001

Commonwealth legislation governing corporations, including their financial reporting framework.

Current asset

An asset that will be sold or realised within 12 months of the end of the financial year being reported on, such as term deposits maturing in three months or stock items available for sale.

Current liability

A liability that will be settled within 12 months of the end of the financial year being reported on, such as payment of a creditor for services provided to the entity.

Deficit

When total expenditure is more than total revenue.

Depreciation

Systematic allocation of the value of an asset over its expected useful life, recorded as an expense.

Disclaimer of opinion

Conclusion expressed if the auditor is unable to obtain sufficient appropriate audit evidence on which to base an audit opinion, and the auditor concludes that the possible effects on the financial (or performance) report of undetected misstatements, if any, could be both material and pervasive.

Emphasis of matter

A paragraph included in an audit opinion that refers to a matter appropriately presented or disclosed in the financial report that, in the auditor's judgement, is of such importance that it is fundamental to users' understanding of the financial report.

Entity

A corporate or unincorporated body that has a public function to exercise on behalf of the state or is wholly owned by the state, including departments, statutory authorities, statutory corporations and government business enterprises.

Expense

The outflow of assets or the depletion of assets an entity controls during the financial year, including expenditure and the depreciation of physical assets. An expense can also be the incurrence of liabilities during the financial year, such as increases to a provision.

Financial Management Act 1994

Victorian legislation governing public sector entities, as determined by the Minister for Finance, including their financial reporting framework.

Financial report

A document reporting the financial outcome and position of an entity for a financial year, which contains an entity's financial statements, including a comprehensive income statement, a balance sheet, a cash flow statement, a comprehensive statement of equity and notes.

Financial sustainability

An entity's ability to manage financial resources so it can meet its current and future spending commitments, while maintaining assets in the condition required to provide services.

Financial year

A period of 12 months for which a financial report is prepared, which may be a different period to the calendar year.

Governance

The control arrangements used to govern and monitor an entity's activities to achieve its strategic and operational goals.

Impairment (loss)

The amount by which the value of an entity's asset exceeds its recoverable value.

Intangible asset

An identifiable non-financial asset, controlled by an entity, that cannot be physically seen, such as software licences or a patent.

Internal audit

A function of an entity's governance framework that examines and reports to management on the effectiveness of the entity's risk management, internal control and governance processes.

Internal control

A method of directing, monitoring and measuring an entity's resources and processes to prevent and detect error and fraud.

Investment

The expenditure of funds intended to result in medium- to long-term service and/or financial benefits arising from the development and/or use of infrastructure assets by either the public or private sectors.

Issues

Weaknesses or other concerns in the governance structure of an entity identified during a financial audit, which are reported to the entity in a management letter.

Liability

A present obligation of the entity arising from past events, the settlement of which is expected to result in an outflow of assets from the entity.

See also current liability and non-current liability.

Management letter

A letter the auditor writes to the governing body, the audit committee and management of an entity outlining issues identified during the financial audit.

Material error or adjustment

An error that may result in the omission or misstatement of information, which could influence the economic decision of users taken on the basis of the financial statements.

Modified opinion

The auditor's expressed qualified opinion, adverse opinion or disclaimer of opinion.

Net result

The value that an entity has earned or lost over the stated period (usually a financial year), calculated by subtracting an entity's total expenses from the total revenue for that period.

Non-current asset

An asset that will be sold or realised later than 12 months after the end of the financial year being reported on, such as investments with a maturity date of two years or physical assets the entity holds for long-term use.

Non-current liability

A liability that will be settled later than 12 months after the end of the financial year being reported on, such as repayments on a five-year loan that are not due in the next 12 months.

Qualified audit opinion

An opinion issued when the auditor concludes that an unqualified opinion cannot be expressed because of:

- disagreement with those charged with governance or

- conflict between applicable financial reporting frameworks or

- limitation of scope.

A qualified opinion is considered to be unqualified except for the effects of the matter to which the qualification relates.

Revaluation

The restatement of a value of non-current assets at a particular point in time.

Revenue

Inflows of funds or other assets or savings in outflows of service potential, or future economic benefits in the form of increases in assets or reductions in liabilities of an entity, other than those relating to contributions by owners, that result in an increase in equity during the reporting period.

Risk

The chance of a negative or positive impact on the objectives, outputs or outcomes of an entity.

Risk register

A tool an entity uses to help identify, monitor and mitigate risks. The register may appear in the form of a plot graph or a table.

Self-funding entities

Entities that generate most of their revenue from their operations, rather than from government funding.

Unmodified opinion

The audit opinion that the auditor expresses when concluding that the financial (or performance) report is prepared, in all material respects, in keeping with the applicable reporting framework.