Results of 2018‒19 Audits: Local Government

Overview

The Victorian local government sector consists of 79 councils, 10 regional library corporations and 17 associated entities.

This report provides Parliament with an outline of the results of our financial and performance audits of the entities within the sector, and our observations, for the year ended 30 June 2019. It also provides our assessment of the financial sustainability of the sector at 30 June 2019.

Local Government dashboard

Our dashboard is an interactive visualisation tool summarising the financial statement data for Victoria’s 79 councils.

We grouped councils into five cohorts based on size, demographics and funding:

- metropolitan—predominately urban in character and located within Melbourne’s densely populated urban core

- interface—one of the nine municipalities that form a ring around metropolitan Melbourne

- regional city—urban and partly rural in character

- large shire—a municipality with more than 16 000 inhabitants that is predominantly rural in character

- small shire—a municipality with fewer than 16 000 inhabitants that is predominantly rural in character.

The cohorts are consistent with Local Government Victoria’s classification of council types.

See below for our dashboard instructions.

Click here to download the data for this dashboard.

Dashboard instructions

|

General instructions for all pages |

|

|---|---|

|

The dashboard is easiest to navigate in the full screen view. Click the button at the bottom right of the window. |

⤢ |

|

To access the detailed view for each chart, click on the chart and select the 'Focus Mode' button at the top right of the window. |

|

|

To return to the dashboard from 'Focus Mode', click 'Back to Report' at the top left of the window. |

|

|

Hierarchy |

|

|

The ‘Financial summary’ and ‘Financial composition’ pages have a pre-set hierarchy. This enables the user to drill through the following levels:

To navigate through these levels, click on the chart and the following icons will appear on the top left of the chart:

These buttons allow you to drill up and down each level of the dataset. |

|

|

To drill down one level, click on the 'Go to the next level in the hierarchy' button |

|

|

To drill down all options one level, click on the ‘Expand all down one level in the hierarchy’ button |

|

| To drill up a level, click on the 'Drill up' button |

|

Transmittal letter

Ordered to be published

VICTORIAN GOVERNMENT PRINTER November 2019

PP No 96, Session 2018–19

President

Legislative Council

Parliament House

Melbourne

Speaker

Legislative Assembly

Parliament House

Melbourne

Dear Presiding Officers

Under the provisions of the Audit Act 1994, I transmit my report Results of 2018–19 Audits: Local Government.

Yours faithfully

Andrew Greaves

Auditor-General

27 November 2019

Acronyms

| AASB | Australian Accounting Standards Board |

| CSV | Cladding Safety Victoria |

| DELWP | Department of Environment, Land, Water and Planning |

| DPC | Department of Premier and Cabinet |

| FinPro | Local Government Finance Professionals |

| LGMFR | Local Government Model Financial Report |

| LGPRF | Local Government Performance Reporting Framework |

| LGV | Local Government Victoria |

| VAGO | Victorian Auditor-General's Office |

| VBA | Victorian Building Authority |

Report overview

|

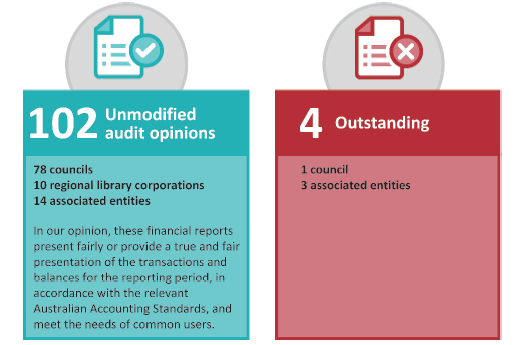

102 Unmodified opinions

Sector reports presented fairly |

|

4 Audit opinions outstanding |

76 council financial reports and performance statements finalised within the statutory reporting deadline |

187 |

|

$240.4 million indicating required improvement over quality assurance procedures for council draft financial statements |

|

127 New medium and high-risk internal control issues |

Overall decline in the last four years, but an increase |

Issues mainly related to:

|

|

|

Councils assessed themselves as being adequately prepared for the incoming accounting standards |

Councils assessed the impact on their financial statements as low |

||

|

Sector-wide developments Combustible cladding |

|

Sector-wide issues Procurement processes |

|

Generally, Victorian councils continue to be financially sound. |

|||

in high-risk issues (14) and number of councils (10)

in high-risk issues (14) and number of councils (10)

Source: VAGO.

Report structure

In this report, we summarise the outcomes of our audits on the financial reports, and performance statements, of the Victorian local government sector for the year ended 30 June 2019.

We also report on key matters arising from our audits and analyse the sector's financial performance. A summary of our recommendations is outlined below.

We carried out the financial audits of these entities under the Audit Act 1994 and Australian Auditing Standards. Each entity pays the cost of its audit.

The cost of preparing this report was $200 000, which is funded by Parliament.

Recommendations

We recommend councils:

1. monitor the impact and progress of Cladding Safety Victoria's rectification works and continue to identify buildings at risk (see Section 1.2)

2. work with the state government to explore sustainable, innovative and longer-term solutions to recyclable waste (see Section 1.2)

3. ensure they have strong frameworks, policies and controls in place for the use of corporate and procurements cards (see Section 3.2)

4. maintain sufficient oversight of activities outsourced to external service providers (see Section 3.2).

We recommend that Local Government Victoria:

5. continues to provide sector-wide guidance, overarching frameworks and policies relating to the incoming Australian Accounting Standards as the sector begins to recognise the impacts of these standards (see Section 3.2)

6. provides further guidance on the presentation requirements of Australian Accounting Standards Board 1052 Disaggregated disclosures to ensure consistency across the sector (see Section 3.2)

7. provides further sector-wide guidance on asset valuations (see Section 3.3).

Submissions and comments received

We have consulted with the Department of Environment, Land, Water and Planning (DELWP) and the entities named in this report, and we considered their views when reaching our conclusions. As required by the Audit Act 1994, we gave a draft copy of this report to those entities and asked for their submissions or comments. We also provided a copy of the report to the Department of Premier and Cabinet (DPC).

The following is a summary of formal responses received. The full responses are included in Appendix A:

- DELWP notes our findings and supports in principal the recommendations in the report—where applicable, we have amended our report based on the submission from DELWP.

- Campaspe Shire Council provided an update on their management letter issues.

1 Sector context

The Victorian local government sector comprises 79 councils, 10 regional library corporations and 17 associated entities. Appendix B lists all these entities.

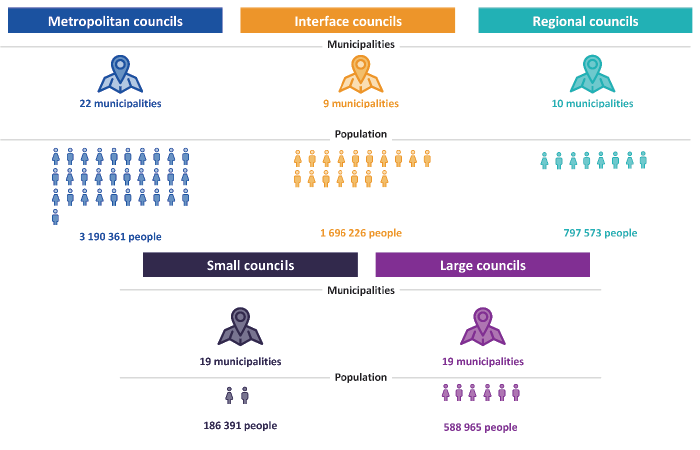

Local Government Victoria (LGV) classifies councils into five Victorian Local Government Comparator Groups. These groups, or cohorts, are determined based on size, demographics, and funding, and are summarised in Figure 1A.

Figure 1A

Council cohorts

Note: Interface councils are the municipalities that surround metropolitan Melbourne, forming the interface between it and regional Victoria.

Source: VAGO, based on Australian Bureau of Statistics, Data by Region, 2017–18.

Councils' principal activities are to maintain the peace, order and good government of each municipal district. They also provide a range of services to local municipalities—as shown in Figure 1B—including maintaining local roads, waste management, delivering family services, and operating aquatic and library facilities.

Figure 1B

Overview of the local government sector

Source: VAGO.

Councils are primarily funded through rates and charges, state and Commonwealth government grants and other contributions. The majority of the sector's assets consist of the infrastructure, property, plant and equipment needed to deliver services to the community. The sector also holds a significant amount of cash and investments, which are used to fund day-to-day activities and long-term capital programs.

Figure 1C summarises key financial balances for the sector.

Figure 1C

Local government sector financial snapshot for the year ended 30 June 2019

Source: VAGO.

1.1 Legislative and reporting framework

Victoria's Constitution recognises local government as one tier of government, with democratically elected councillors governing councils, and a council appointed chief executive officer managing their operations.

Local Government Act 1989

The Local Government Act 1989 establishes the constitutional, electoral, and operational arrangements for local government in Victoria. This includes the roles and responsibilities of councils, elected councillors and council administration. While councils are administered under the Local Government Act 1989, they operate autonomously and are accountable to their ratepayers and residents.

Along with LGV as the responsible government agency providing information, policy advice and support works to councils, councils are also represented in Victoria by:

- the Municipal Association of Victoria, established under the Municipal Associations Act 1907

- Local Government Finance Professionals (FinPro)—an association for people working in local government in Victoria

- the Victorian Local Governance Association—an independent member‑based association supporting councils, councillors, and the community in good governance.

Local Government Bill 2019

The Local Government Bill 2019 was introduced to Parliament on 13 November 2019 and builds on the reforms presented in the previous proposed Local Government Bill 2018, which lapsed before the November 2018 election.

The Bill aims to deliver on the Victorian Government's commitment to create a Local Government Act that introduces a modern framework empowering councils to improve service delivery, focus on deliberative engagement and long-term financial management to support Victoria's councils and their communities.

1.2 Sector developments

Combustible cladding

In response to significant building fires caused by combustible cladding in Melbourne in November 2014 and in London in June 2017, the state government established the Victorian Cladding Taskforce in July 2017. This taskforce investigated the extent of non-compliant external wall cladding on buildings in Victoria, and make recommendations for improvements to protect the public and restore confidence that building and fire safety issues are being addressed appropriately.

Following the release of the interim findings and recommendations by the taskforce in December 2017, the Victorian Building Authority (VBA), on behalf of the state government and with the assistance of councils, undertook a state‑wide audit of residential, multi-unit buildings of three storeys or more likely to have combustible cladding. Four ministerial declarations since February 2018 have given the VBA the functions of the Municipal Building Surveyor for over 300 buildings assessed as higher risk.

The state government established Cladding Safety Victoria (CSV) in July 2019 to oversee a $600 million program of rectification works on class 2 buildings of a higher risk rating across Victoria. CSV will provide support and guidance to owners and occupants of buildings with combustible cladding and aims to reduce risks to an acceptable level.

Councils need to monitor CSV's rectification program and continue to work with the VBA to identify buildings at risk.

Waste and recycling

China's restriction of its intake of foreign waste for recycling in 2018 and the collapse of SKM Recycling in July 2019 have significantly affected kerbside recyclable waste management across the sector.

While some councils found alternative short-term recycling processors, many had no alternative other than to send their recyclable waste to landfill. Public media has estimated this waste at more than 4 500 tonnes per week, across 31 councils.

Diverting recyclable waste to landfill has resulted in councils incurring more costs, which will likely be passed onto ratepayers and residents in the form of waste charges. The full impact of this is yet to be determined, given the expected time lag between councils incurring the costs and recovering them from ratepayers.

|

Administrators are appointed by the Minister for Local Government in instances of serious governance failure to undertake the roles and responsibilities of the council. |

While some councils have resumed recycling following resolution with SKM Recycling's receivers, and the announced purchase of SKM Recycling, councils and the state government need to explore sustainable, innovative and long‑term solutions to recyclable waste.

Governance matters

High standards of governance are fundamental in enabling councils to effectively and efficiently manage the public resources entrusted to them.

While most councils have suitable controls to govern their operations, several recent governance failures have resulted in interventions by the state government through the appointment of administrators or municipal monitors.

Figure 1D summarises the status of councils with recent governance issues.

Figure 1D

Status of governance matters

|

Council |

Description of finding |

|---|---|

|

Ararat Rural City Council |

On 2 May 2019, the Minister for Local Government advised Ararat Rural City Council that he had concluded the municipal monitor's appointment at the council, who had previously been appointed for two years to August 2019. |

|

Central Goldfields Shire Council |

Central Goldfields Shire Council continue to have a state government-appointed panel of administrators oversee its operations. This will remain until the next council general election in October 2020. |

|

Greater Geelong City Council |

The role of the two municipal monitors at Greater Geelong City Council will shift to a 'watching brief' in recognition of progress since their appointment on 7 September 2017 following a Commission of Inquiry. The municipal monitors will be in place until the council's general election in October 2020. |

|

Frankston City Council |

Following an 18-month appointment term ending in June 2019, the municipal monitor at Frankston City Council was extended to 19 September 2019, upon the appointment of a new chief executive officer. |

|

South Gippsland Shire Council |

The municipal monitor, appointed to South Gippsland Shire Council by the state government from 18 June 2018 to 4 April 2019, provided his final report to the Minister for Local Government about the council's governance processes and practices on 21 March 2019. The Minister for Local Government subsequently appointed a Commission of Inquiry, which provided its report to the Minister on 13 June 2019. The council was subsequently dismissed on 22 June 2019 under the Local Government (South Gippsland Shire Council) Act 2019. The state government appointed a panel of three administrators to operate the council from 24 July 2019 until the next general election for the council in 2021. |

Source: VAGO.

|

Municipal monitors monitor and advise council on governance processes and practices. They report and provide an update on council improvement actions to the Minister for Local Government. |

Governance failures impede a council's ability to maintain strong internal controls that safeguard assets, promote accountability and increase efficiency. Several reports discussing procurement risks, fraud and corruption across the sector have recently been published, including:

- the Independent Broad-based Anti-corruption Commission's Special report on corruption risks associated with procurement in local government (September 2019)

- the Tasmanian Audit Office's Procurement in Local Government (September 2019)

- the Office of the Auditor General for Western Australia's Fraud Prevention in Local Government (August 2019)

- VAGO's Fraud and Corruption Control—Local Government (June 2019).

We further analyse the sector's procurement practices in Section 3.2.

2 Results of audits

This Part summarises the results of our financial report and performance statement audits, including observations about internal controls for the sector, for the year ended 30 June 2019. Appendix B lists all the entities covered by this report and the date and nature of audit opinions issued.

2.1 Conclusion

The financial reports and performance statements of all the entities in the local government sector that we audited were found to be reliable.

At the date of this report's publication, the financial audits of one council— West Wimmera Shire Council—and three associated entities—Regional Landfill Clayton South Joint Venture, Regent Management Company Pty Ltd, and Procurement Australia—have not been completed.

2.2 Financial report audit opinions

We carried out our financial audits in accordance with Australian Auditing Standards. Figure 2A summarises the financial report audit opinions we issued, highlighting that, overall, the sector's financial reports are accurate and reliable.

Figure 2A

Financial report audit opinions issued for the year ended 30 June 2019

Source: VAGO.

|

The financial report is prepared in line with relevant Australian Accounting Standards and applicable legislation. It shows the financial performance and position of the entity. |

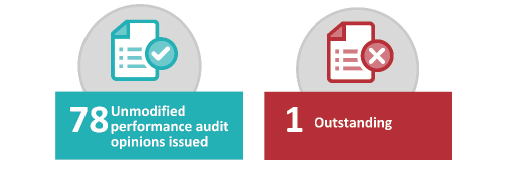

2.3 Performance statement audit opinions

We carried out our audits of performance statements in accordance with the Local Government Performance Reporting Framework (LGPRF).

Figure 2B summarises the performance statement audit opinions we issued.

Figure 2B

Local government sector performance statement audit opinions issued for the year ended 30 June 2019

Source: VAGO.

|

The performance statement outlines council performance in accordance with indicators prescribed by the Local Government (Planning and Reporting) Regulations 2014. |

Thematic errors and inconsistencies in performance statements

Our audits of the sector's performance statements identified accuracy and completeness errors mostly relating to:

- statutory planning—council planning decisions upheld by the Victorian Civil and Administrative Tribunal, with decisions incorrectly included or excluded from the relevant reporting period

- food safety—critical and major non-compliance outcome notifications, where calculations were based on the financial year, rather than the calendar year per the LGPRF

- workforce turnover—resignations and terminations compared to average staff, where non-permanent employees were incorrectly included in the indicator, and permanent or terminated employees incorrectly calculated.

These errors were mostly due to incorrectly using and classifying data, due to a lack of robust quality review processes when preparing performance statements.

We also identified inconsistencies in the approach taken for the unrestricted cash indicator—some councils incorrectly included term deposits with a maturity date over three months as unrestricted cash.

Where we identified material errors, we required councils to amend their indicators and statements.

Councils should ensure there are appropriate preparation, and independent quality review processes over the performance indicators, as they are key measures of council transparency, accountability and performance.

Local Government Performance Reporting Framework

Based on previous VAGO recommendations, the Minister for Local Government approved the Strategic Directions Paper 2018–21 in February 2019 to introduce mandatory performance reporting to strengthen and improve the transparency and availability of performance information about councils.

Our performance audit Reporting on Local Government Performance—tabled in Parliament on 23 May 2019—assessed if the LGPRF communicated performance information that is relevant, timely, accurate and easy to understand for councils and the community. It examined how councils use the LGPRF to improve their performance and if councils' other performance activities, such as reporting on strategic objectives and benchmarking, are effective.

The report made 11 recommendations—five to DELWP and six to councils—and concluded that the LGPRF:

- along with other internally generated data, is not being sufficiently used by councils to understand their performance and communicate it to their community or inform their decisions

- lacks good outcome measures, with data reported inconsistently between councils and some reported data being unreliable

- has not achieved the aim of reducing the reporting burden on councils.

2.4 Financial reporting quality

The timeliness of the published financial reports and the accuracy of draft reports presented for audit are important and interrelated quality attributes of financial reporting.

Generally, councils implemented effective processes and procedures to prepare their financial reports and presented accurate draft reports for audit.

Timeliness

|

The Local Government Act 1989 requires councils to submit their audited financial reports and performance statements to the Minister for Local Government by 30 September each year. |

Timely financial reporting is a critical element of an entity's accountability to users of the financial statements. The later financial reports are produced after year end, the less useful they become. We measure timeliness by the time taken after year-end for each council to finalise their financial reports.

As shown in Figure 2C, 76 councils met the statutory deadline of 30 September 2019 (79 in 2018).

Figure 2C

Timeliness of financial reporting by councils

Source: VAGO.

Northern Grampians Shire Council and West Wimmera Shire Council did not meet the original statutory deadline. They sought, and received, extensions from the Minister for Local Government.

Yarriambiack Shire Council made an application to the Minister for Local Government for an extension to the statutory deadline. This application was made after the statutory deadline and therefore not considered, and the council advised accordingly.

In all three cases, the delay was primarily due to issues encountered with reporting of property, plant and equipment values.

Accuracy

|

Material errors are significant misstatements or omissions of information that may influence a user's decision‑making. |

Accurate financial reports do not contain material errors and reliably record an entity's financial performance and position. Material errors identified during the audit must be corrected before we can issue a clear opinion. Errors that are not corrected reduce the accuracy and clarity of the final financial report.

We identified 187 financial statement errors across the 79 councils, totalling $240.4 million (2017–18: 155 financial statement errors, totalling $307.7 million). Figure 2D summarises the most common errors we found during our audits.

Figure 2D

Common errors identified

|

Dollar errors |

Common errors we found included:

|

|

Disclosure errors |

Common financial statement disclosure errors we found related to:

|

Source: VAGO.

2.5 Internal control observations

|

Internal controls help entities meet their objectives reliably and cost effectively, comply with relevant legislation and also decrease the risk of fraud and error. |

In our annual audits, we consider the internal controls relevant to a council's financial and performance reporting. We also assess whether councils have managed the risk that their reports will not be complete or accurate.

To the extent that we considered them, councils' internal controls were adequate to ensure reliable financial and performance reporting. However, we identified some weaknesses, which are summarised below.

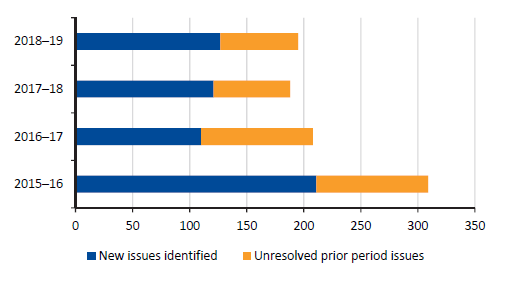

We identified 127 new medium and high-risk internal control issues during our 2018–19 audits (121 in 2017–18). Figure 2E shows that the number of new issues identified in 2018–19, while slightly higher than in 2017–18, has decreased over the last four years.

The number of unresolved prior year issues has also steadily reduced over the last four years. This indicates that councils are actively addressing their control deficiencies. While an improvement, councils should continue to address outstanding issues within recommended and agreed time frames.

We have not analysed low-risk internal control issues in this report, because they are minor issues or opportunities to improve. In Appendix C we provide the risk rating definitions applied to the issues we report in our audit management letters.

Figure 2E

Number of new and unresolved prior year management letter issues in the local government sector for the years ended 30 June, 2016 to 2019

Source: VAGO.

High-risk rated issues

New issues raised in 2018–19

We identified 14 new, high-risk issues at 10 councils in 2018–19 (compared to nine new, high-risk issues across six councils in 2017–18). Thirteen of these 14 issues remain open at the following councils:

- Ballarat City Council

- Central Goldfields Shire Council

- Greater Geelong City Council

- Hepburn Shire Council

- Horsham Rural City Council

- Mildura Rural City Council

- South Gippsland Shire Council

- Strathbogie Shire Council

- Warrnambool City Council.

The high-risk rated internal control issues identified in 2018–19 primarily relate to:

- asset management and valuation processes (46 per cent of all issues raised)

- procurement processes, including the use of corporate cards and vendor master file changes (15 per cent of all issues raised).

We discuss these key issues in further detail in Part 3.

Unresolved prior year, high-risk issues

In 2017–18, we reported 14 unresolved high-risk rated issues. Our follow up of these issues in 2018–19 indicated that councils continue to work through implementation plans to resolve them, with six remaining unresolved at 30 June 2019.

Figure 2F summarises the high-risk rated internal control issues identified in prior years that remain unresolved.

Figure 2F

Unresolved high-risk rated issues from prior years

|

Council |

Description of finding |

|---|---|

|

Campaspe Shire Council |

Campaspe Shire Council did not undertake a valuation of assets in 2018–19—which was originally scheduled to be completed in 2017–18—for bridges, drainage assets, footpaths and cycle ways. Roads were scheduled for a valuation assessment in 2016–17. No condition or impairment assessments were completed for any of these assets in 2018–19. Management acknowledge this issue remains unresolved and have committed to completing a full unit rate and condition assessment for these asset classes in 2019–20. |

|

Central Goldfields Shire Council |

Prior to 30 June 2019, Central Goldfields Shire Council last performed a valuation for its land and building assets in 2014. While it completed a valuation of land and buildings at 30 June 2019, several assets controlled by the council were not included in the valuation. Management have committed to revaluing these assets in 2019–20. |

|

Gannawarra Shire Council |

Gannawarra Shire Council did not complete a fair value assessment over asset classes not revalued at 30 June 2019, consistent with practices in 2017–18. Management continue to work to resolve this issue and an update on the progress will be followed up in 2019–20. |

|

South Gippsland Shire Council |

Performance reporting preparation process issues were previously raised at South Gippsland Shire Council. These issues included non-compliance with the LGPRF, as well as errors in performance statement indicator data and the performance statement template. Management have made some progress in addressing this issue by updating systems and processes, implementing quarterly checks and educating new staff to improve the quality and accuracy of data captured. The risk rating of this issue was escalated in 2018–19, as it had not been fully resolved. |

|

Towong Shire Council |

Towong Shire Council did not appropriately document the fair value assessment of their infrastructure, property, plant and equipment assets. Further, the council did not complete an impairment assessment for their assets. Management have revised their rectification plans to June 2020 from June 2019 due to internal staff changes. |

|

West Wimmera Shire Council |

West Wimmera Shire Council did not have a detailed fixed asset register at 30 June 2017 that identified individual assets such as bridges, road segments and drainage assets. As the audit is still outstanding, an update on the progress of this issue will be followed up in 2019–20. |

Source: VAGO.

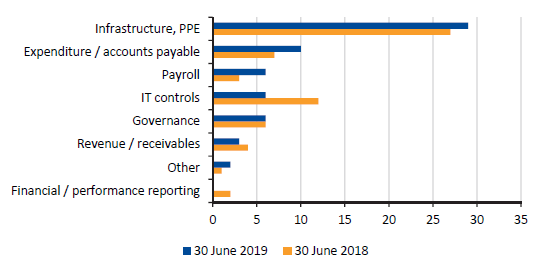

Medium-risk rated issues

New issues raised in 2018–19

Of the 113 new, medium-risk issues identified in 2018–19 (112 newly identified issues in 2017–18), 60 per cent related to infrastructure, property, plant and equipment, payroll and expenditure systems. Issues generally included:

- lack of fair value assessments being adequately completed for all infrastructure, property, plant and equipment, and inconsistencies and weaknesses in asset valuation process (see Section 3.3)

- poor controls relating to procurement practices (see Section 3.2)

- lack of segregation of duties within the payroll function.

Timely and adequate rectification of control weaknesses will reduce the risk of:

- material misstatements to the presentation of infrastructure, property, plant and equipment balances in council financial statements, and non‑compliance with the Local Government Better Practice Guidance materials

- unauthorised procurement of goods and services

- misappropriation of assets

- fraudulent behaviour.

Unresolved prior year, medium-risk issues

There were 62 unresolved medium-risk issues at 30 June 2019 (62 at 30 June 2018), demonstrating that councils continue to address their control deficiencies.

Figure 2G shows the types of issues raised in prior years that are still unresolved, noting that these issues are consistent with the problematic areas previously reported on.

Figure 2G

Unresolved medium-risk rated prior year issues at 30 June 2019 and 30 June 2018, by area

Note: PPE = property, plant and equipment.

Source: VAGO.

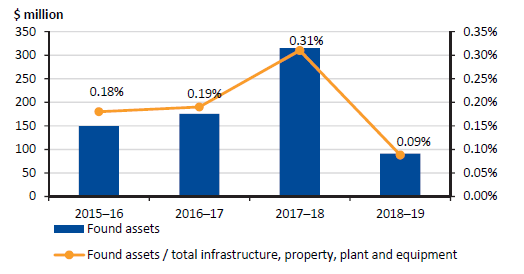

2.6 Found assets

|

Found assets are assets that have not previously been valued or included in the entity's financial report when they should have been, because the entity was not aware of their existence. |

Across the sector, councils continue to identify found assets, albeit significantly fewer than in previous years. This is symptomatic of many issues, including:

- poor data accuracy in asset management systems

- a lack of regular and timely communication between asset management and finance teams

- poor communication between councils and other Victorian public sector entities where there is uncertainty about the ownership of assets

- councils not assessing and recording assets in a timely manner.

Figure 2H summarises the sector's found assets since 2015–16.

Figure 2H

Found assets as a percentage of total infrastructure, property, plant, and equipment over the last four years

Source: VAGO.

3 Focus areas at a glance

In this Part, we summarise some key themes currently affecting the sector and comment on the results of the information we obtained and observed during our audits.

We asked all 79 councils to complete a self-assessment, and collated their responses on their current processes and systems in respect to:

- preparedness for new Australian Accounting Standards

- procurement

- outsourced service providers.

This Part further analyses ongoing issues relating to asset management and asset valuations that were raised in previous years' reports.

3.1 Conclusion

Overall, most councils assessed themselves as being adequately prepared for the incoming accounting standards and concluded that the expected impact was minimal.

The sector continues to experience internal control weaknesses surrounding procurement practices, asset management and valuation processes, and with management oversight and monitoring of its outsourced service providers.

3.2 Focus area highlights

Preparedness for new Australian Accounting Standards

A suite of significant changes to accounting standards will impact the local government sector's financial reporting for the financial year ending 30 June 2020.

These standards include:

- AASB 15 Revenue from Contracts with Customers

- AASB 1058 Income for Not-for-profit Entities

- AASB 16 Leases.

The majority of councils stated that they have a plan to implement the new accounting standards and had communicated this plan to key operational stakeholders.

However, most councils also assessed that there were improvements to be made in the communication of issues, impacts and progress updates relating to the implementation of the standards to those charged with governance and Audit and Risk Committees.

Figure 3A summarises the sector's self-assessment of their preparedness for the incoming accounting standards.

Figure 3A

Results of councils' activities in preparation for incoming Australian Accounting Standards

Source: VAGO.

Councils had varying results in determining the impact of the incoming accounting standards on their financial statements, accounting policies and key internal controls. The sector's self-assessment concluded that:

- the majority of councils believe there will not be an impact, or, if there is an impact, it will be immaterial

- while the impact to the financial statements is likely to be minimal, most councils identified there would be changes to underlying controls, data collection and processes

- the incoming accounting standards would have minimal impact on existing software, with the majority of councils relying on spreadsheets or expecting to easily modify existing software.

Almost all councils stated they relied on LGV-delivered webinars or FinPro training and forums for their information, training and research about the incoming accounting standards. Almost half of councils also relied on their auditors for information.

In light of these responses, and the significant reliance on FinPro and LGV by councils, we recommend LGV continue to provide sector-wide guidance and develop overarching frameworks and policies to address the key impacts relating to the incoming accounting standards, and to ensure consistent application.

AASB 1052 Disaggregated disclosures

|

LGV publishes the Local Government Model Financial Report annually to assist councils in preparing annual financial statements in accordance with Australian Accounting Standards and the Local Government Act 1989. |

The 2018–19 Local Government Model Financial Report (LGMFR) reintroduced a separate note to the financial report in accordance with AASB 1052 Disaggregated disclosures, requiring councils to disclose:

- the nature and objectives of each broad function of the council

- the carrying amount of assets that are reliably attributable to each function

- the income and expense attributable to each function, with grant funding separately disclosed.

Councils were typically able to disaggregate their financial data and present this disaggregated information in line with the requirements of the LGMFR. However, we recommend councils continue to scrutinise the disaggregation of their financial data to better reflect the functions and activities of their council, and that LGV provide further guidance on the presentation requirements in line with the accounting standards to ensure consistency across the sector.

Procurement

|

The primary function of procurement is to cost‑effectively and efficiently acquire the goods and materials required by an organisation to provide services to their customers. |

Procurement policies

All 79 councils stated they had a procurement policy in place, and 68 councils stated that they had an up-to-date policy in 2018–19.

Forty-one councils identified at least one breach in their procurement policy during the year. Six councils reported more than 10 individual breaches of their procurement policy in 2018–19. Breaches in council procurement policies included:

- tender process not undertaken when supplier spend exceeds council determined threshold—11 per cent of councils did not have systems and processes in place to monitor supplier spend and ensure it is within the prescribed thresholds

- staff self-approving their own invoices or purchase orders—22 per cent of councils stated staff could approve their own invoices, and staff could approve their own purchase orders at 29 per cent of councils

- purchase orders raised subsequent to the receipt of the invoice—however, 71 per cent of councils stated they had a monitoring process over purchase orders raised after invoice date.

Vendor master file changes and user access rights

Figure 3B summarises the strengths and weaknesses, based on council self‑assessments, in respect to the vendor master file change processes and management of user access rights for procurement.

Figure 3B

Strengths and weaknesses relating to vendor master file changes and user access rights

|

|

Strengths

|

|

|

Weaknesses

|

Source: VAGO.

Corporate cards

Councils stated that, on average, they had 76 corporate or procurement cards in operation. The number of cards in use varied from none to 256. This number did not necessarily correlate to the size of the council.

Seventy councils advised that they had an approval process in place for corporate and procurement card transactions in a formal documented policy.

Seventy-six councils confirmed that they have monitoring controls implemented to ensure policy compliance—in the form of reconciliations, approval of transactions, review of monthly statements and audits. Thirty-five councils also confirmed that there had been instances of non-compliance with their internal policy in 2018–19.

Our performance audit Fraud and Corruption Control—Local Government—tabled in Parliament on 19 June 2019—assessed whether local councils' fraud and corruption controls were well designed and operating as intended, focusing on expenditure and processes relating to a variety of areas, including corporate card use.

The report made 12 recommendations, including for councils to:

- review their corporate card policies

- improve controls to ensure only allocated cardholders use the cards and ensure appropriate segregation of duties over expenditure approvals exist

- document and develop formalised reporting over the use of credit cards, and to incorporate, where appropriate, data analytics to identify anomalies.

Given the high risk of misappropriation of assets and fraudulent behaviour surrounding corporate and procurements cards, councils need to ensure they have robust frameworks and policies in place to control their use. Councils also need to ensure they conduct an appropriate level of oversight, review and monitoring to reduce associated risks.

Outsourced service providers

Where an entity outsources aspects of its operations to external providers, management must have appropriate oversight of the financial activities undertaken externally if they are to have an effective internal control and financial reporting process.

Forty-nine councils stated they had outsourced services that directly impacted their financial reporting or internal control processes. These services include:

- cash collections from various sources, including carparks and leisure centres

- issuing parking infringements and debt collection

- information systems support

- aquatic and leisure centre management.

Only nine of the 49 councils that had outsourced arrangements stated they had formal policies in place. Forty-three councils concluded they had appropriate processes and controls in place to monitor the performance of their external providers, mostly documented in formal service agreements.

|

An assurance report provides details on the description, design and operating effectiveness of controls at a service organisation for use by user entities, where it relates to financial reporting. |

However, councils indicated that less than a quarter of these service agreements stipulated that the external provider needed to provide them an assurance report on the adequacy and functioning of their internal controls, as it relates to financial reporting. In the absence of an assurance report, councils need to obtain oversight and comfort over the functioning of internal controls at the external provider through other means. Councils are generally not obtaining this oversight or comfort, which creates a financial risk.

Collection of outstanding parking infringements by Fines Victoria

For 2018–19, no councils obtained an assurance report from any external providers of outsourced service arrangements with a financial impact. This is particularly concerning, given many councils outsource the collection and follow up of outstanding parking infringements to Fines Victoria.

While councils obtained written representation from Fines Victoria at 30 June 2019 on the adequacy of their internal control processes as it relates to financial reporting, the delays in relation to outstanding debt collections further demonstrate the need for councils to maintain sufficient oversight over the internal control processes at outsourced service providers.

3.3 Asset management and valuation process

The sector recognised an asset revaluation decrement of $45.3 million in 2018–19 ($7.0 billion increment in 2017–18), against an infrastructure, property, plant, and equipment asset base of $103.3 billion at 30 June 2019 ($102.1 billion at 30 June 2018). This decrement was mainly driven by a reduction of around $1.5 billion in land values, offset by a $1.4 billion increase in infrastructure values.

Figure 3C summarises the valuation movement in the asset classes in 2018–19 compared to the prior year.

Figure 3C

Asset revaluation movement in 2018–19 and 2017–18

|

Asset class |

2018–19 |

2017–18 |

|---|---|---|

|

Land |

↓ $1.5 billion |

↑$5.6 billion |

|

Buildings |

↑$69.7 million |

↑$162.5 million |

|

Infrastructure |

↑$1.4 billion |

↑$1.2 billion |

|

Other |

↑$11.8 million |

↑2.9 million |

|

Total |

↓ $45.3 million |

↑ $7.0 billion |

Source: VAGO.

Against this overall decrement, the sector undertook asset renewal and upgrades of $2.7 billion ($2.2 billion in 2017–18) compared to $1.6 billion ($1.5 billion in 2017–18) of depreciation and amortisation expenses— demonstrating continued positive capital replacement, in line with previous years.

In our review of infrastructure, property, plant and equipment—and the revaluation process within the sector—we continue to identify issues mainly relating to:

- fair value assessments of many asset classes not being undertaken with sufficient regularity

- inconsistencies across the sector in the application and appropriate documentation of the condition assessment process for infrastructure assets, including:

- a lack of key metrics and indicators in determining the condition of infrastructure assets and the resulting impact on fair value and remaining asset useful life

- inadequate regularity of condition assessments, with some infrastructure asset classes never having had a condition assessment performed

- poor communication between asset management teams and finance staff, and a lack of sufficient oversight of the condition assessment process by management

- individual asset components within an asset class measured inconsistently with the entire asset class, which is not in accordance with Australian Accounting Standards

- delays in the timing of capitalisation for completed capital works in progress projects—resulting in understatement of depreciation expenses

- a lack of robust and sufficiently regular impairment assessments over all infrastructure, property, plant and equipment asset classes

- ongoing found assets, albeit there has been a significant improvement across the sector in 2018–19 (see Section 2.6).

These key issues persist across the sector. Councils, with the guidance of LGV, need to prioritise improving their asset management frameworks, policies, and processes to ensure infrastructure, property, plant and equipment balances disclosed in the financial statements are complete and accurate. This is particularly important given the management of these assets represents a key function of the council for providing services to the community.

4 Financial outcomes and sustainability

In this Part, we summarise the financial performance and position of all Victorian councils for the year ended 30 June 2019 and comment on their financial sustainability.

Appendix D lists our financial sustainability indicators and risk assessment criteria. We publish the detailed data for each council from 2014–15 to 2018–19 on our website, as part of our interactive data dashboard.

4.1 Conclusion

Generally, Victorian councils continue to be financially sound.

At 30 June 2019, most councils—particularly metropolitan councils—continue to demonstrate strong financial performance, positive operating results, strong liquidity ratios and low debt levels.

While the sector demonstrates relatively weaker long-term financial sustainability, the relevant indicators still represent a strong financial position.

4.2 Overview

Figure 4A summarises the sector's seven financial sustainability risk indicators at 30 June 2019, by cohort.

Figure 4A

Financial sustainability risk indictors by cohort, 30 June 2019

|

Indicator |

Average across councils for year ended 30 June 2019 |

||||||

|---|---|---|---|---|---|---|---|

|

All councils |

Metro |

Interface |

Regional |

Large |

Small |

||

|

Profitability indicators |

|||||||

|

Net result margin |

per cent |

17.26% |

13.51% |

34.32% |

19.34% |

15.80% |

13.90% |

|

Adjusted underlying result |

per cent |

4.25% |

9.09% |

5.49% |

2.43% |

1.98% |

1.29% |

|

Financing indicators |

|||||||

|

Liquidity |

ratio |

3.20 |

2.71 |

3.66 |

3.77 |

3.10 |

3.77 |

|

Internal financing |

per cent |

159% |

223% |

133% |

136% |

135% |

134% |

|

Indebtedness |

per cent |

17.82% |

10.45% |

17.38% |

32.07% |

22.53% |

14.34% |

|

Asset renewal and maintenance indicators |

|||||||

|

Capital replacement |

ratio |

1.55 |

1.87 |

2.19 |

1.48 |

1.33 |

1.14 |

|

Renewal gap |

ratio |

1.16 |

1.22 |

1.09 |

0.95 |

1.22 |

1.18 |

Key: ● = high risk, ● = medium risk, ● = low risk.

Note: We used draft 30 June 2019 figures for West Wimmera Shire Council as it has not finalised its financial report at the date of this report's publication.

Source: VAGO.

4.3 Financial performance highlights

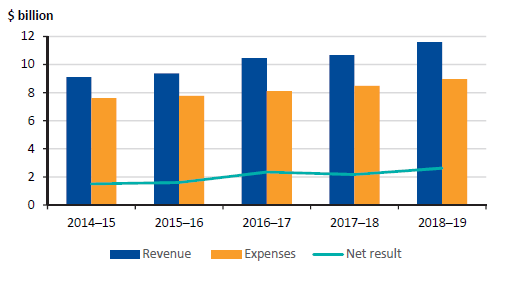

In 2018–19, Victorian councils generated $11.6 billion in revenue, against expenditure of $9.0 billion—generating a net surplus of $2.6 billion.

Figure 4B shows that the sector's revenues and expenses have consistently increased since 2014–15. Total revenue has grown by approximately 6 per cent compounded annually, while expenses have increased by approximately 4 per cent compounded annually, over the same time period.

Figure 4B

Financial performance of the sector, 2014–15 to 2018–19

Source: VAGO.

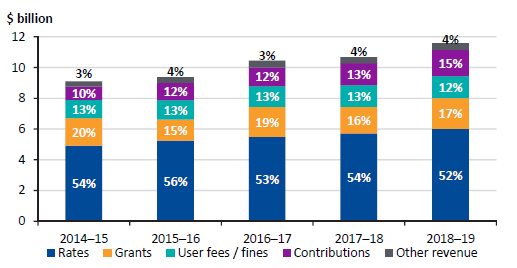

While revenue has increased consistently since 2014–15, its composition has changed slightly—most notably since the introduction of rate capping on 1 July 2016.

Figure 4C highlights the slight reduction in the proportion of the sector's revenue generated by rates since 2016–17. Councils have mostly offset this reduction through an increased reliance on contributions. There has also been a slight reduction since 2014–15 of user fees and fines—as a proportion of total revenue—which suggests the sector is targeting revenue from sources outside of ratepayers and service users.

Figure 4C

Revenue composition for the sector, 2014–15 to 2018–19

Source: VAGO.

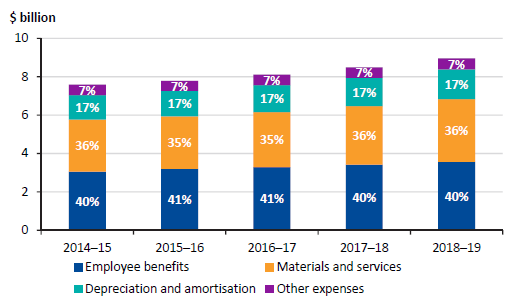

Conversely, Figure 4D highlights that the composition of expenditure has not changed significantly since 2014–15.

Figure 4D

Expense composition for the sector, 2014–15 to 2018–19

Source: VAGO.

Profitability indicators

Our review of profitability indicators assesses the ability of councils to fund their operations from their surpluses. Consistent surpluses ensure the continued operation of services and satisfaction of community needs.

While impacted by the introduction of rate capping and an increase in waste and recycling costs, the sector as a whole continues to generate a surplus from operations, as highlighted by Figures 4A and 4B.

Metropolitan councils continue to report consistently strong adjusted underlying results. In contrast, regional, large and small councils experience more fluctuation in their results—with 33 per cent of these councils experiencing a negative result for 2018–19 (31 per cent in 2017–18).

Figure 4E shows the adjusted underlying result by cohort over the last five years.

Figure 4E

Adjusted underlying surplus analysis by cohort, 2014–15 to 2018–19

Source: VAGO.

4.4 Financial position highlights

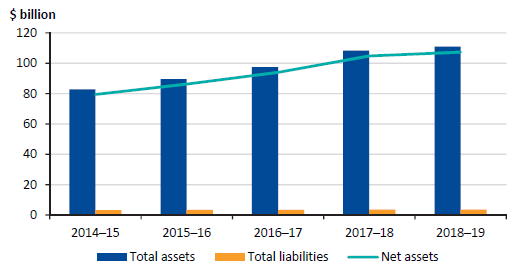

Net assets held by the sector increased to $107.3 billion in 2018–19 from $104.9 billion in 2017–18.

Figure 4F highlights that the sector has steadily increased its net asset position over the last five years. Metropolitan councils hold 50 per cent of total assets (52 per cent in 2017–18).

Figure 4F

Total assets, total liabilities and net assets for the sector, 2014–15 to 2018–19

Source: VAGO.

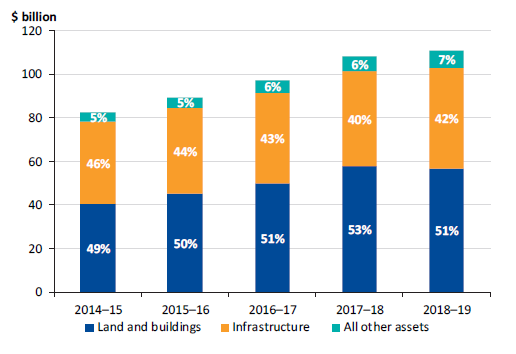

Figure 4G illustrates that the sector's assets mostly comprise land, buildings and infrastructure, which are used to deliver services to the community. Given their community service nature, these assets do not generate income, nor are they easily sold to fund operational requirements. These assets also require significant expenditure to maintain their service capacity to the community. Accordingly, they require significant monitoring, oversight and investment by the sector to ensure they meet community needs in the long term.

Figure 4G

Composition of total assets for the sector, 2014–15 to 2018–19

Source: VAGO.

Financing indicators

Our review of the sector's financing indicators assesses the ability of councils to repay short-term liabilities, fund capital expenditure from operating cashflows, and repay borrowings. Councils need to monitor their cash position to ensure they can meet their obligations as they fall due.

Liquidity

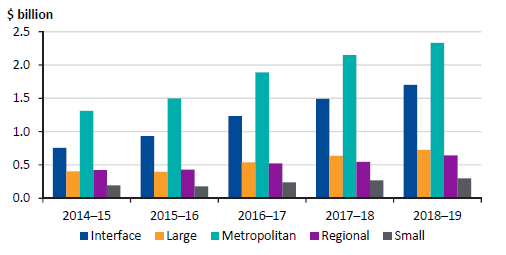

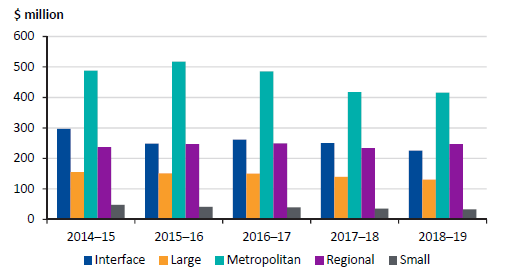

The sector continues to maintain a strong liquidity position—with $5.7 billion held in cash at 30 June 2019 ($5.1 billion at 30 June 2018). The majority of this cash is either set aside for future intended capital works or is restricted by a contract with an external party. Figures 4H and 4I show the results of the liquidity indicator, and the total cash and term deposits reported by councils by cohort over the last five years.

Figure 4H

Liquidity analysis by cohort, 2014–15 to 2018–19

Source: VAGO.

Figure 4I

Cash and term deposit balances by cohort, 2014–15 to 2018–19

Source: VAGO.

Internal financing

|

AASB 15 Revenue from Contracts with Customers and AASB 1058 Income of Not-for-Profit Entities may affect the internal financing indicator from 2019–20 onwards as councils will need to reassess the period in which they recognise revenue. |

Councils receive a large portion of Commonwealth grant funding towards the end of the financial year, impacting the underlying result and, ultimately, the internal financing indicator. The overall sector result for 2018–19 of 159 per cent is consistent with previous years (145 per cent for 2017–18).

Figure 4J shows the results of the internal financing indicator by cohort over the last five years.

Figure 4J

Internal financing indicator analysis by cohort, 2014–15 to 2018–19

Source: VAGO.

Indebtedness

The sector continues to hold low levels of debt, evidenced by borrowing costs accounting for 0.5 per cent of total revenue and 1 per cent of rates and charges for 2018–19 (0.5 per cent and 1 per cent respectively for 2017–18).

Due to their major infrastructure plans, metropolitan and interface councils hold the majority of debt within the sector, at 61 per cent of total debt held at 30 June 2019 (62 per cent at 30 June 2018).

Figures 4K and 4L show the results of the indebtedness indicator, and the total borrowings reported by cohort, over the last five years.

Figure 4K

Indebtedness indicator analysis by cohort, 2014–15 to 2018–19

Source: VAGO.

Figure 4L

Borrowings balance by cohort, 2014–15 to 2018–19

Source: VAGO.

Asset renewal and maintenance indicators

|

Councils need to effectively and efficiently maintain and renew their infrastructure, property, plant, and equipment to service their communities and meet public demand. |

Our review of the asset renewal and maintenance indicators assesses the adequacy of council spending on infrastructure, property, plant and equipment.

Capital replacement

Despite significant rising sector costs and fluctuating adjusted underlying results—due to rising waste and recycling costs and the impact of rate capping—councils have still prioritised meeting the long-term needs of their communities through capital expenditure, as indicated by the capital replacement ratios across all cohorts being above one.

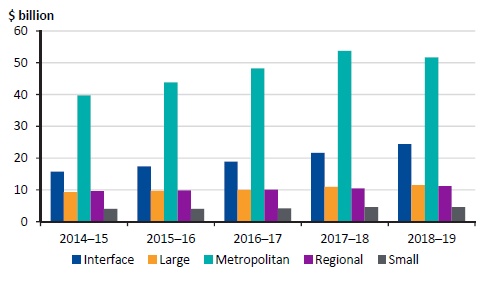

Figures 4M and 4N show the results of the capital replacement indicator, and the total infrastructure, property, plant and equipment reported by councils by cohort over the last five years.

Figure 4M

Capital replacement indicator analysis by cohort, 2014–15 to 2018–19

Source: VAGO.

Figure 4N

Infrastructure, property, plant and equipment balance by cohort, 2014–15 to 2018–19

Source: VAGO.

The disparity in capital replacement and maintenance between metropolitan and interface councils compared to their regional, large and small council counterparts continues. This arises from differences in population growth, the demand for infrastructure by their municipalities, and available resources.

While fluctuating adjusted underlying results by regional, large and small councils impact their ability to plan in the long-term, they still need to implement strategies to continue to service community needs.

Renewal gap

The renewal gap indicator supports a continual prioritisation of asset renewal and maintenance by councils—consistent with the capital replacement indicator. Regional councils have a renewal gap indicator of 0.95, indicating spending on existing assets is slower than depreciation.

Figure 4O shows the results of the renewal gap indicator across the sector for the last five years.

Figure 4O

Renewal gap indicator analysis by cohort, 2014–15 to 2018–19

Source: VAGO.

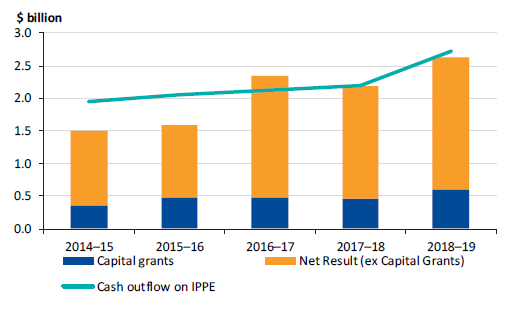

Capital spending

During the year ended 30 June 2019, the sector spent $2.7 billion in total on new assets ($2.2 billion in 2017–18). This investment was largely driven by the surpluses generated for the year and is largely consistent with historic trends. While councils receive capital grants from various sources, these grants are not significant compared to the sector's capital spend. This highlights the importance of councils generating sufficient surpluses to fund long-term service needs, so as to not rely on borrowed funds.

Figure 4P outlines the difference between capital grants and other profit sources, against total capital expenditure.

Figure 4P

Capital spending analysis, 2014–15 to 2018–19

Note: IPPE = infrastructure, property, plant and equipment.

Source: VAGO.

Appendix A. Submissions and comments

We have consulted with DELWP and the entities named in this report, and we considered their views when reaching our conclusions. As required by the Audit Act 1994, we gave a draft copy of this report, or relevant extracts, to those entities and asked for their submissions and comments. We also provided a copy of the report to DPC.

Responsibility for the accuracy, fairness and balance of those comments rests solely with the agency head.

Responses were received as follows:

- DELWP

- Campaspe Shire Council

RESPONSE provided by the Secretary, DELWP

RESPONSE provided by the Chief Executive Officer, Campaspe Shire Council

Appendix B. Audit opinions

Figure B1 lists the entities included in this report. It details the type of audit opinion for their 30 June 2019 financial reports and performance statements, and the date it was issued to each entity.

Figure B1

Audit opinions issued for the local government sector for the year ended 30 June 2019

|

Entity |

Financial report |

Performance statement |

||

|---|---|---|---|---|

|

Clear audit opinion issued |

Audit opinion signed date |

Clear audit opinion issued |

Audit opinion signed date |

|

|

Metropolitan |

||||

|

Banyule City Council |

✔ |

18 Sep 2019 |

✔ |

18 Sep 2019 |

|

Bayside City Council |

✔ |

26 Sep 2019 |

✔ |

26 Sep 2019 |

|

Boroondara City Council |

✔ |

12 Sep 2019 |

✔ |

12 Sep 2019 |

|

Brimbank City Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

|

City of Monash |

✔ |

17 Sep 2019 |

✔ |

17 Sep 2019 |

|

Darebin City Council |

✔ |

15 Sep 2019 |

✔ |

15 Sep 2019 |

|

Frankston City Council |

✔ |

28 Sep 2019 |

✔ |

28 Sep 2019 |

|

✔ |

22 Aug 2019 |

n/a |

n/a |

|

Glen Eira City Council |

✔ |

6 Sep 2019 |

✔ |

6 Sep 2019 |

|

Greater Dandenong City Council |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

✔ |

5 Sep 2019 |

n/a |

n/a |

|

Hobsons Bay City Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

|

Kingston City Council |

✔ |

30 Aug 2019 |

✔ |

30 Aug 2019 |

|

Knox City Council |

✔ |

25 Sep 2019 |

✔ |

25 Sep 2019 |

|

Manningham City Council |

✔ |

19 Sep 2019 |

✔ |

19 Sep 2019 |

|

Maribyrnong City Council |

✔ |

18 Sep 2019 |

✔ |

18 Sep 2018 |

|

Maroondah City Council |

✔ |

29 Aug 2019 |

✔ |

29 Aug 2019 |

|

Melbourne City Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

|

✔ |

13 Sep 2019 |

n/a |

n/a |

|

✔ |

9 Oct 2019 |

n/a |

n/a |

|

n/a |

Outstanding |

n/a |

n/a |

|

Moonee Valley City Council |

P |

26 Sep 2019 |

✔ |

26 Sep 2019 |

|

Moreland City Council |

✔ |

18 Sep 2019 |

✔ |

18 Sep 2019 |

|

Port Phillip City Council |

✔ |

12 Sep 2019 |

✔ |

12 Sep 2019 |

Figure B1

Audit opinions issued for the local government sector for the year ended 30 June 2019—continued

|

Entity |

Financial report |

Performance statement |

||

|---|---|---|---|---|

|

Clear audit opinion issued |

Audit opinion signed date |

Clear audit opinion issued |

Audit opinion signed date |

|

|

Metropolitan—continued |

||||

|

City of Stonnington |

✔ |

9 Sep 2019 |

✔ |

9 Sep 2019 |

|

✔ |

28 Aug 2019 |

n/a |

n/a |

|

Whitehorse City Council |

✔ |

11 Sep 2019 |

✔ |

11 Sep 2019 |

|

Yarra City Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

|

Interface |

||||

|

Cardinia Shire Council |

✔ |

18 Sep 2019 |

✔ |

18 Sep 2019 |

|

Casey City Council |

✔ |

12 Sep 2019 |

✔ |

12 Sep 2019 |

|

City of Whittlesea |

✔ |

17 Sep 2019 |

✔ |

17 Sep 2019 |

|

Hume City Council |

✔ |

12 Sep 2019 |

✔ |

12 Sep 2019 |

|

Melton City Council |

✔ |

19 Sep 2019 |

✔ |

19 Sep 2019 |

|

Mornington Peninsula Shire Council |

✔ |

25 Sep 2019 |

✔ |

25 Sep 2019 |

|

Nillumbik Shire Council |

✔ |

10 Sep 2019 |

✔ |

10 Sep 2019 |

|

Wyndham City Council |

✔ |

30 Sep 2019 |

✔ |

30 Sep 2019 |

|

✔ |

15 Nov 2019 |

n/a |

n/a |

|

Yarra Ranges Shire Council |

✔ |

12 Sep 2019 |

✔ |

12 Sep 2019 |

|

Regional |

||||

|

Ballarat City Council |

✔ |

24 Sep 2019 |

✔ |

24 Sep 2019 |

|

Greater Bendigo City Council |

✔ |

26 Sep 2019 |

✔ |

26 Sep 2019 |

|

Greater Geelong City Council |

✔ |

17 Sep 2019 |

✔ |

17 Sep 2019 |

|

Greater Shepparton City Council |

✔ |

26 Sep 2019 |

✔ |

26 Sep 2019 |

|

Horsham Rural City Council |

✔ |

27 Sep 2019 |

✔ |

27 Sep 2019 |

|

Latrobe City Council |

✔ |

18 Sep 2019 |

✔ |

18 Sep 2019 |

|

Mildura Rural City Council |

✔ |

30 Sep 2019 |

✔ |

30 Sep 2019 |

|

✔ |

2 Oct 2019 |

n/a |

n/a |

|

✔ |

2 Oct 2019 |

n/a |

n/a |

|

Wangaratta Rural City Council |

✔ |

30 Sep 2019 |

✔ |

30 Sep 2019 |

|

Warrnambool City Council |

✔ |

26 Sep 2019 |

✔ |

26 Sep 2019 |

|

Wodonga City Council |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

Large shire |

||||

|

Bass Coast Shire Council |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

Baw Shire Council |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

Campaspe Shire Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

|

Colac-Otway Shire Council |

✔ |

27 Sep 2019 |

✔ |

27 Sep 2019 |

|

Corangamite Shire Council |

✔ |

30 Sep 2019 |

✔ |

30 Sep 2019 |

|

East Gippsland Shire Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

Figure B1

Audit opinions issued for the local government sector for the year ended 30 June 2019—continued

|

Entity |

Financial report |

Performance statement |

||

|---|---|---|---|---|

|

Clear audit opinion issued |

Audit opinion signed date |

Clear audit opinion issued |

Audit opinion signed date |

|

|

Large shire—continued |

||||

|

Glenelg Shire Council |

✔ |

30 Sep 2019 |

✔ |

30 Sep 2019 |

|

Golden Plains Shire Council |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

Macedon Ranges Shire Council |

✔ |

27 Sep 2019 |

✔ |

27 Sep 2019 |

|

Mitchell Shire Council |

✔ |

18 Sep 2019 |

✔ |

18 Sep 2019 |

|

Moira Shire Council |

✔ |

16 Sep 2019 |

✔ |

16 Sep 2019 |

|

Moorabool Shire Council |

✔ |

9 Sep 2019 |

✔ |

9 Sep 2019 |

|

Mount Alexander Shire Council |

✔ |

30 Sep 2019 |

✔ |

30 Sep 2019 |

|

Moyne Shire Council |

✔ |

25 Sep 2019 |

✔ |

25 Sep 2019 |

|

South Gippsland Shire Council |

✔ |

26 Sep 2019 |

✔ |

26 Sep 2019 |

|

Southern Grampians Shire Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

|

Surf Coast Shire Council |

✔ |

19 Sep 2019 |

✔ |

19 Sep 2019 |

|

Swan Hill Rural City Council |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

Wellington Shire Council |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

Small shire |

||||

|

Alpine Shire Council |

✔ |

26 Sep 2019 |

✔ |

26 Sep 2019 |

|

Ararat Rural City Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

|

Benalla Rural City Council |

✔ |

30 Sep 2019 |

✔ |

30 Sep 2019 |

|

Borough of Queenscliffe |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

Buloke Shire Council |

✔ |

26 Sep 2019 |

✔ |

26 Sep 2019 |

|

Central Goldfields Shire Council |

✔ |

30 Sep 2019 |

✔ |

30 Sep 2019 |

|

Gannawarra Shire Council |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

Hepburn Shire Council |

✔ |

25 Sep 2019 |

✔ |

25 Sep 2019 |

|

Hindmarsh Shire Council |

✔ |

23 Sep 2019 |

✔ |

23 Sep 2019 |

|

Indigo Shire Council |

✔ |

26 Sep 2019 |

✔ |

26 Sep 2019 |

|

Loddon Shire Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

|

Mansfield Shire Council |

✔ |

19 Sep 2019 |

✔ |

19 Sep 2019 |

|

Murrindindi Shire Council |

✔ |

27 Sep 2019 |

✔ |

27 Sep 2019 |

|

Northern Grampians Shire Council |

✔ |

18 Nov 2019 |

✔ |

18 Nov 2019 |

|

Pyrenees Shire Council |

✔ |

20 Sep 2019 |

✔ |

20 Sep 2019 |

|

Strathbogie Shire Council |

✔ |

25 Sep 2019 |

✔ |

25 Sep 2019 |

|

Towong Shire Council |

✔ |

25 Sep 2019 |

✔ |

25 Sep 2019 |

|

West Wimmera Shire Council |

n/a |

Outstanding |

n/a |

Outstanding |

|

Yarriambiack Shire Council |

✔ |

21 Oct 2019 |

✔ |

21 Oct 2019 |

Figure B1

Audit opinions issued for the local government sector for the year ended 30 June 2019—continued

|

Entity |

Financial report |

Performance statement |

||

|---|---|---|---|---|

|

Clear audit opinion issued |

Audit opinion signed date |

Clear audit opinion issued |

Audit opinion signed date |

|

|

Regional library corporations |

||||

|

Casey-Cardinia Regional Library Corporation |

✔ |

30 Sep 2019 |

n/a |

n/a |

|

Corangamite Regional Library Corporation |

✔ |

2 Sep 2019 |

n/a |

n/a |

|

Eastern Regional Library Corporation |

✔ |

25 Sep 2019 |

n/a |

n/a |

|

Geelong Regional Library Corporation |

✔ |

23 Aug 2019 |

n/a |

n/a |

|

Goulburn Valley Regional Library Corporation |

✔ |

30 Sep 2019 |

n/a |

n/a |

|

North Central Goldfields Regional Library Corporation |

✔ |

26 Sep 2019 |

n/a |

n/a |

|

West Gippsland Regional Library Corporation |

✔ |

25 Sep 2019 |

n/a |

n/a |

|

Whitehorse-Manningham Regional Library Corporation |

✔ |

18 Sep 2019 |

n/a |

n/a |

|

Wimmera Regional Library Corporation |

✔ |

26 Sep 2019 |

n/a |

n/a |

|

Yarra Plenty Regional Library Corporation |

✔ |

30 Sep 2019 |

n/a |

n/a |

|

Associated entities |

||||

|

Regional Landfill Clayton South Joint Venture |

n/a |

Outstanding |

n/a |

n/a |

|

MomentumOne Shared Services Pty Ltd |

✔ |

2 Oct 2019 |

n/a |

n/a |

|

Municipal Association of Victoria |

✔ |

12 Nov 2019 |

n/a |

n/a |

|

Procurement Australia(a) |

n/a |

Outstanding |

n/a |

n/a |

|

RFK Pty Ltd (trading as Community Chef) |

✔ |

15 Oct 2019 |

n/a |

n/a |

|

Regional Kitchen Pty Ltd |

✔ |

15 Oct 2019 |

n/a |

n/a |

|

Wangaratta Livestock Exchange Pty Ltd |

✔ |

28 Oct 2019 |

n/a |

n/a |

|

Wimmera Development Association |

✔ |

27 Sep 2019 |

n/a |

n/a |

(a) Procurement Australia has a 30 September balance date—no audit opinion had been issued at the date of this report for the year ending 30 September 2019. A clear audit opinion for the 30 September 2018 financial report was issued on 19 December 2018.

Note: n/a = not applicable.

Source: VAGO.

Appendix C. Control issues risk ratings

Figure C1 shows the risk ratings applied to issues raised in management letters. It also details what they represent and the expected timeline for the issue to be resolved.

Figure C1

Risk definitions applied to issues reported in audit management letters

|

Rating |

Definition |

Management action required |

|---|---|---|

|

High |

The issue represents:

|

Requires executive management to correct the misstatement in the financial report, or address the issue, as a matter of urgency to avoid a modified audit opinion. Requires immediate management intervention with a detailed action plan to be implemented within one month. |

|

Medium |

The issue represents:

|

Requires management intervention with a detailed action plan implemented within three to six months. |

|

Low |

The issue represents:

|

Requires management intervention with a detailed action plan implemented within six to 12 months. |

Source: VAGO.

Appendix D. Financial sustainability indicators

Figure D1 shows financial and non-financial sustainability indicators used to assess the financial sustainability risks of councils. These indicators should be considered collectively and are more useful when assessed over time as part of a trend analysis.

Our analysis of financial sustainability risk in this report reflects on the position of each council.

Figure D1

Financial sustainability indicators, formulas and descriptions

|

Indicator |

Formula |

Description |

|---|---|---|

|

Net result margin (%) |

Net result/Total revenue |

A positive result indicates a surplus, and the larger the percentage, the stronger the result. A negative result indicates a deficit. Operating deficits cannot be sustained in the long term. The net result and total revenue are obtained from the comprehensive operating statement. |

|

Adjusted underlying result (%) |

Adjusted underlying surplus (or deficit)/ Adjusted underlying revenue |

This measures an entity's ability to generate surplus in the ordinary course of business—excluding non-recurrent capital grants, non-monetary asset contributions, and other contributions to fund capital expenditure from net result. A surplus or increasing surplus suggests an improvement in the operating position. |

|

Liquidity (ratio) |

Current assets/ Current liabilities |

This measures the ability to pay existing liabilities in the next 12 months. A ratio of one or more means that there are more cash and liquid assets than short-term liabilities. |

|

Internal financing (%) |

Net operating cashflow/Net capital expenditure |

This measures the ability of an entity to finance capital works from generated cashflow. The higher the percentage, the greater the ability for the entity to finance capital works from their own funds. Net operating cashflows and net capital expenditure are obtained from the cashflow statement. Note: The internal financing ratio cannot be less than zero. Where a calculation has produced a negative result, this has been rounded up to 0 per cent. |

|

Indebtedness (%) |

Non-current liabilities/Own-sourced revenue |

This assesses an entity's ability to pay the principal and interest on borrowings, as and when they fall due, from the funds it generates. The lower the ratio, the less revenue the entity is required to use to repay its total debt. Own-sourced revenue is used, rather than total revenue, because it does not include grants or contributions. |

|

Capital replacement (ratio) |

Cash outflows for the addition of new infrastructure, property, plant and equipment/ Depreciation |

Comparison of the rate of spending on new infrastructure, property, plant and equipment with its depreciation. Ratios higher than 1:1 indicate that spending is faster than the depreciating rate. This is a long-term indicator, as capital expenditure can be deferred in the short term if there are insufficient funds available from operations and borrowing is not an option. Cash outflows for infrastructure are taken from the cashflow statement. Depreciation is taken from the comprehensive operating statement. |

|

Renewal gap (ratio) |

Renewal and upgrade expenditure/Depreciation |

This compares the rate of spending on existing assets through renewing, restoring, and replacing existing assets with depreciation. Ratios higher than 1.0 indicate that spending on existing assets is faster than the depreciation rate. |

Source: VAGO.

Financial sustainability risk assessment criteria

The financial sustainability risk of each local council has been assessed using the criteria outlined in Figure D2.

Detailed benchmarking, the underlying raw data, and the results of each indicator for each of the councils from 2014–15 to 2018–19 is published on our website as part of our interactive data dashboard.

Figure D2

Financial sustainability risk indicators—risk assessment criteria

|

Risk |

Net result |

Adjusted underlying result |

Liquidity |

Internal financing |

Indebtedness |

Capital replacement |

Renewal gap |

|---|---|---|---|---|---|---|---|

|

High |

Less than negative 10% Insufficient revenue is being generated to fund operations and asset renewal. |

Less than 0% Insufficient surplus being generated to fund operations |

Less than 0.75 Immediate sustainability issues with insufficient current assets to cover liabilities. |

Less than 75% Limited cash generated from operations to fund new assets and asset renewal. |

More than 60% Potentially long-term concern over ability to repay debt levels from own‑source revenue. |

Less than 1.0 Spending on capital works has not kept pace with consumption of assets. |

Less than 0.5 Spending on existing assets has not kept pace with consumption of these assets. |

|

Medium |

Negative A risk of long-term run down to cash reserves and inability to fund asset renewals. |

0%–5% Surplus being generated to fund operations |

0.75–1.0 Need for caution with cashflow, as issues could arise with meeting obligations as they fall due. |

75–100% May not be generating sufficient cash from operations to fund new assets. |

40–60% Some concern over the ability to repay debt from own‑source revenue. |

1.0–1.5 May indicate spending on asset renewal is insufficient. |

0.5–1.0 May indicate insufficient spending on renewal of existing assets. |

|

Low |

More than 0% Generating surpluses consistently. |

More than 5% Generating strong surpluses to fund operations |