Annual Report 2017–18

Overview

This report covers the activities of VAGO for the period 1 July 2017 to 30 June 2018. It is prepared in accordance with the Audit Act 1994 and the Financial Management Act 1994, and complies with the requirements of relevant Australian Accounting Standards and Interpretations, Standing Directions and Financial Reporting Directions.

This year we have once again considered integrated reporting principles, such as materiality and value creation, when preparing this report. We also have introduced elements of transparency reporting used widely by the audit profession, to better inform Parliament and Victorians about our operations. Following the development of our new strategic plan, we have also considered our own strategic objectives when determining what is most important to include.

This report cost $70 000 to produce.

|

Transparency reporting has its origins in the private sector and encourages disclosing more information about how an organisation operates and how this affects its performance. |

|

Integrated reporting is strategic, future-focused reporting that explains how an organisation draws on the resources and relationships available to it, to create value over time. |

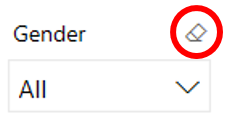

This year for the first time we have developed a dashboard of our workforce data. A profile of all VAGO employees is included in Appendix A of the report, but this dashboard allows that data to be filtered and manipulated.

| The dashboard is easiest to navigate in the full screen view. Click the button at the bottom right of the window. |  |

|

You can use the drop down menus to filter the data. You can select a single segment of data by clicking the relevant box, or can compare various segments by holding the Ctrl button and selecting multiple boxes. To clear your selection, click the ‘clear selections’ button at the top right of the pane (circled in red in the picture) which will appear when you hover over that area. |

|

| You can also access a detailed view for each indicator. Hover over the chart and click the ‘focus mode’ button at the top right of the window. |

|

| To return to the dashboard from ‘focus mode’, click ‘Back to report’ at the top left of the window. |

|

| To share the dashboard via email, LinkedIn, Facebook or Twitter, click the ‘Share’ button at the bottom left of the window. |

Transmittal Letter

President

Legislative Council

Parliament House

Melbourne

Speaker

Legislative Assembly

Parliament House

Melbourne

Dear Presiding Officers

I am pleased to transmit, in accordance with section 7B of the Audit Act 1994, the annual report of the Victorian Auditor-General’s Office for the year ended 30 June 2018 for presentation to Parliament.

Yours faithfully

Andrew Greaves

Auditor-General

20 September 2018

Accountable officer’s declaration

In accordance with the Financial Management Act 1994, I am pleased to present the Report of Operations for the Victorian Auditor-General’s Office for the year ended 30 June 2018.

Andrew Greaves

Auditor-General

20 September 2018

Foreword

Last year we focused on building VAGO's leadership team, getting the right structure in place and improving our external relationships. This year we have turned the lens inwards and assessed VAGO's own practices, particularly our use of technology and the way we spend our resources. We have also been quite deliberate in applying our audit findings to ourselves, leading to several important adjustments to our practices.

I am pleased with the considerable savings we've made by reducing internal red tape and reviewing our ICT systems—savings we then redirected to our audit work, providing more value to Victorians. We have adopted new technologies as we aim to be at the forefront of audit technology and methodology.

One major achievement this year has been the creation of a new vision and strategic plan—a clear direction and a map for how we will meet future challenges. This plan outlines our hopes and aspirations for VAGO. We have begun to better explore our full mandate, are trying to better measure our impact and are leading the way by becoming a more effective and efficient organisation. But as we've expanded our focus on using and sharing data, we are encountering emerging issues around data security and privacy. We are working with our stakeholders closely on this and taking a collaborative approach to resolving these matters.

I am most proud this year of the work, led by our staff, to develop and commit to a new set of organisational values, which reflect how we want to work with each other and our stakeholders.

Another important step that will improve our work is updating the Audit Act 1994. I was disappointed that the proposed Bill was not passed this year as the new powers and clarifications it contained would go a long way to modernising our practices. I'm optimistic that the new Parliament will see merit in the proposed legislative changes reflecting the considerable effort that my office and others put into its development. If these proposed changes are passed by the new Parliament, VAGO will be able to be more responsive and accountable, and ultimately provide a better service to Victorians.

Andrew Greaves

Auditor-General

20 September 2018

1 Our organisation: About VAGO

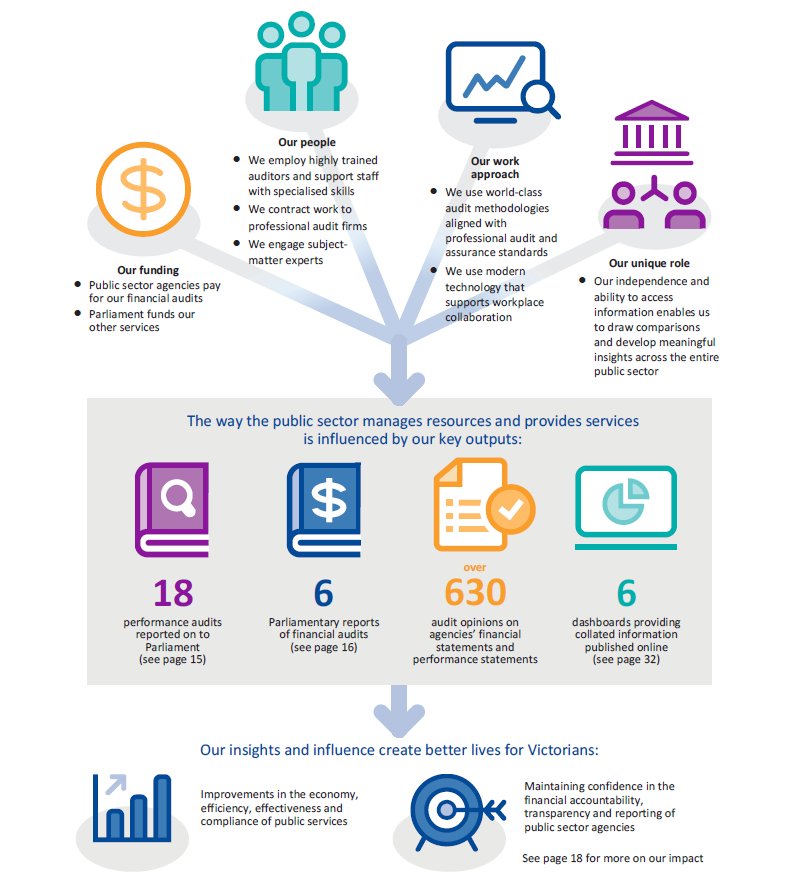

The Auditor-General is an Independent Officer of the Victorian Parliament, appointed on behalf of Victorians to scrutinise how well government spends public money. VAGO helps hold the government to account through our financial and performance audits of public sector agencies and our resulting reports to Parliament.

Along with the Independent Broad-based Anti‑corruption Commission, the Victorian Ombudsman and the Victorian Inspectorate, we are part of Victoria's modern integrity system, and we work to protect the public interest.

Two principal pieces of legislation govern what we do:

- The Constitution Act 1975 establishes the role of the Auditor-General and gives the Auditor-General complete discretion in how the functions and powers of the role are performed and exercised.

- The Audit Act 1994 establishes the Auditor-General's mandate and VAGO. It provides the legal basis for our powers and identifies the responsibilities of our role. In Section 1.4 we discuss the proposed changes to this Act.

We audit the financial reports of over 500 agencies each year, including government departments, statutory bodies, educational institutions, public hospitals, water corporations, insurers and local government councils. We also conduct performance audits that assess the effectiveness, efficiency, economy and compliance of government agencies, programs and services.

With our new follow-the-dollar powers, we are also able to audit non‑government organisations that provide government services under contract. Our first follow-the-dollar audit, Safety and Cost Effectiveness of Private Prisons, was completed this year.

Our unique position and access to information across the entire public sector gives us insights into common issues and allows us to create more value for the agencies we audit. We not only provide recommendations on how to improve services and function more efficiently and effectively, we are now also providing useful information back to agencies through our data analytics dashboards.

1.1 Our new strategic plan

In late 2017, we launched our new strategic plan which articulates our intentions for VAGO's future. It maps out where we are heading, how we will work together to get there, and what success looks like. Our strategic plan, combined with our new values, detailed in Section 1.2, provides a solid foundation for change and will help us achieve our vision of creating better lives for Victorians through our insights and influence.

|

Our objectives |

Our directions |

What success looks like |

Our progress towards success |

|---|---|---|---|

|

Be more relevant by delivering credible and authoritative reports and advice about things that matter and will make a difference |

Modernise our auditing methods Explore our full mandate Take a longer-term perspective |

Our audit program effort is targeted across efficiency, effectiveness, economy and compliance |

As part of our Annual Plan 2018–19, we have better balanced our performance audit program across efficiency, effectiveness, economy and compliance to ensure we explore our full mandate. We have included targeted reviews on efficiency, audits that analyse a thematic audit area over time and matters of good housekeeping and financial regularity that underpin service delivery. |

|

The benefits realised by the public sector show an increased return on investment from our audit work |

We have started foundational work to help us understand our influence, the impact we have through our audit work, and the benefits realised for audited agencies. |

||

|

Be valued for our independence and more influential because of the unique perspectives we provide |

Strengthen our engagement Better leverage our access Increase accessibility to our work |

More of our performance audits originate from requests from Parliament, the public sector and the public |

We have started to review the source of our audit topics over the past year to establish a baseline against which we can measure our performance in the future. |

|

Use of our reports and associated datasets in government service delivery and for parliamentary purposes has increased |

We have started foundational work to help us understand our influence, the impact we have through our audit work, and the benefits realised for audited agencies. |

||

|

Enable high performance by our people through a supportive culture, professional development and collaboration |

Be clear about what we stand for Invest in excellence Get the mix right |

Employee engagement has increased |

Employee engagement is measured by the People Matter Survey run by the Victorian Public Sector Commission. In 2018 our score on the Employee Engagement Index was 66. |

|

We develop, attract, and retain the talent we need |

In 2017–18, our staff attended around 25 hours of training on average, covering technical audit topics, professional requirements, management training and a range of other topics. |

||

|

Model exemplary performance in everything we do |

Simplify our business Embrace new technology Better intelligence to drive decisions |

Workforce productivity has increased |

From 2016–17 to 2017–18, we have increased the overall VAGO productivity rate (the per cent of available hours dedicated to audit work) from 55 per cent to 60 per cent. |

|

Our internal practices set the benchmark for public sector entities and other audit offices |

In 2017–18, we have started to apply the same lens that we apply to audited agencies to ourselves to ensure that we meet the same standard. Notable areas in which we have been forging the way include digital records and our move to cloud-based services and integrated applications. |

Note: Next year, as our first full year operating with the new strategic plan, we will report our progress more completely.

1.2 Our values

We launched our new values in May 2018. They were developed using a staff‑led process, through focus groups and a committee. The values guide our behaviours, shape how we interact with our stakeholders and drive a more open and supportive culture.

|

We are an independent integrity organisation. We will stay true to our values and meet the high standards that Victoria's Parliament, public sector and community expect from us. We show respect

We collaborate

We are innovative

We are accountable

|

1.3 Our operating model

Our operating model underpins how we create value for Parliament and the Victorian community.

1.4 Proposed changes to our legislation

The Audit Amendment Bill 2017 was introduced into Parliament late in 2017 and proposed a substantial modernisation of the current Audit Act 1994. The changes, if they had passed, would have clarified how some of our existing powers operate and introduced some new powers.

One key amendment would have allowed us to conduct assurance reviews: short, focused reviews of a matter or issue. We would have been able to form a limited assurance opinion on whether the subject of the audit met the particular aspect of efficiency, economy or effectiveness we examined. These reviews would allow us to be more responsive to Parliamentarians as they would not be as time consuming as traditional performance audits. This amendment would also allow us to provide positive feedback about what agencies are doing, highlighting where they are performing well.

Another major new addition would have been the power to enter the premises of public bodies or associated entities to inspect the premises and any document or other thing. These access powers could be used only if the required information is not provided voluntarily and after we have issued an information‑gathering notice to an agency.

More broadly, the changes proposed in the Bill would have clarified our powers to access privileged and other protected information, without the need to issue a coercive notice under section 11.

This is significant because our current legislation modifies our unrestricted access to such information by linking it to our coercive powers to obtain information under section 11 of the Act. We have always treated our coercive powers as a measure of last resort, as evidenced by the fact that they have rarely been used. Without the new provisions, we are concerned that the use of section 11 will need to become routine, especially as we roll out our data analytics strategy. This will place extra administrative burdens on us, the audited agencies and the Victorian Inspectorate, which monitors our use of our coercive powers.

The proposed amendments would also have provided us with the ability to better share the information we gather through our audit process with public bodies. This means, for example, we could share our data analytic dashboards more broadly.

At the time of publishing this annual report, the Bill had not been passed.

2 Our work: Relevance, influence and impact

We have been performing our key functions for many years—financial audits since 1851 and performance audits since the 1980s. The challenge for us is to remain relevant and current.

One new endeavour is making the most of the broad and deep access we have to public sector information as part of our function and powers. At the same time we've maintained our ongoing focus on building productive relationships with our stakeholders. To have real influence on public sector performance, and ultimately impact the lives of Victorians, we must make sure our work is targeted in the right areas.

2.1 Our 2017–18 work program

This year we tabled 18 performance audits. Twelve of these were listed in our Annual Plan 2017–18, two were follow-up audits, and four were from our Annual Plan 2016–17. We deferred one audit to 2018–19 and cancelled one audit.

Figure 2A

2017–18 performance audit reports tabled by sector

|

Central Agencies and Whole of Government |

|---|

|

Effectively Planning for Population Growth* Fraud and Corruption Control ICT Disaster Recovery Planning* Internal Audit Performance* The Victorian Government ICT Dashboard |

|

Environment and Primary Industries |

|

Improving Victoria's Air Quality Follow Up of Selected 2012–13 and 2013–14 Performance Audits:

Protecting Victoria's Coastal Assets |

|

Health and Human Services |

|

Community Health Program ($) Victorian Public Hospital Operating Theatre Efficiency |

|

Infrastructure and Transport |

|

Assessing Benefits from the Regional Rail Link Project Managing the Level Crossing Removal Program V/Line Passenger Services* |

|

Justice and Community Safety |

|

Maintaining the Mental Health of Child Protection Practitioners Safety and Cost Effectiveness of Private Prisons ($) |

|

Local Government |

|

Local Government and Economic Development Managing Surplus Government Land |

Key: * indicates audits from our Annual Plan 2016–17.

($) indicates follow-the-dollar audits.

Of the remaining nine audits that were not tabled during the year as planned, three were delayed due to significant challenges we faced in accessing essential data, three due to the complexity and sensitivity of the subject matter, and three due to internal resourcing challenges. Seven of these nine audits are scheduled to table in the first quarter of 2018–19.

We are actively reviewing our performance audit resourcing strategy and project management approaches, to improve the timeliness of reporting.

In 2017–18, we tabled six reports on the results of our financial audits as detailed in our Annual Plan 2017–18.

Figure 2B

2017–18 reports tabled on the results of financial audits

|

Auditor-General's Report on the Annual Financial Report of the State of Victoria: 2016–17 Results of 2016–17 Audits: Local Government Results of 2016–17 Audits: Public Hospitals Results of 2016–17 Audits: Water Entities Results of 2017 Audits: Technical and Further Education Institutes Results of 2017 Audits: Universities |

2.2 Our stakeholders

At VAGO, we rely on our reputation to influence the public sector to improve its administration and performance. As we have no executive powers to implement or require action on our recommendations, it is vital that we have relevant, high‑quality, evidence-based products and productive relationships with all our stakeholders. Our primary stakeholders are the Victorian Parliament and the public sector agencies we audit.

This year we reviewed our stakeholder engagement framework and developed a strategy to complement our new strategic plan. Our focus is on improving the consistency of the experience of our stakeholders, and being clear about what we offer them. In the future, we'll be developing new approaches to working with our stakeholders to meet our common goal of continuously improving public services and programs.

We know that our work is valued when we see our reports being used by our Parliamentary stakeholders.

Figure 2C

Parliamentary committees using our reports

|

In February 2018, the Economy and Infrastructure Committee's Fourth report into infrastructure projects referenced High Value High Risk 2016–17: Delivering HVHR Projects (2016), Managing the Level Crossing Removal Program (2017) and Public Participation in Government Decision-Making (2015). In March 2018, the Environment, Natural Resources and Regional Development Committee's report Inquiry into the sustainability and operational challenges of Victoria's rural and regional councils echoed our concerns about many regional councils' financial positions. The report heavily referenced our financial audits in the sector, as well as our 2014 reports Asset Management and Maintenance by Councils and Shared Services in Local Government. Also in March 2018, the Law Reform, Road and Community Safety Committee's report Inquiry into drug law reform referred to Prevention and Management of Drug Use in Prisons (2013) and a specific recommendation we made to the Department of Justice and Regulation. In May 2018, the Economy and Infrastructure Committee's Inquiry into electric vehicles referenced a figure from our report Managing the Environmental Impacts of Transport (2014) about passenger vehicles and greenhouse gas emissions. In June 2018, the Legal and Social Issues Committee released its Inquiry into the Public Housing Renewal Program. The report echoed the findings and concerns of our audits on public housing, particularly 2017's Managing Victoria's Public Housing. The committee noted that 'many of the issues raised in the 2012 and 2017 audits were consistent with the evidence provided to this Inquiry. The Committee reiterates the need for the Victorian Government to implement these recommendations to improve the strategic direction of public housing in Victoria.' |

To ensure we are sharing knowledge and can be at the forefront of developments in our profession, we maintain strong working relationships with educational and professional organisations, and with our audit, integrity and public sector peers—both domestic and overseas.

In addition to working directly with our stakeholders on specific audit topics, our staff also take the results of our audits to audiences that have a role in influencing or implementing change.

This year the Auditor-General presented to a range of peer and public sector forums on:

- the pillars of integrity and our role in Victoria's integrity system

- how the public service can govern well by implementing key measures to ensure efficient and effective operations, reliable financial reporting and compliance—the so-called 'three lines of defence'

- the relevance of General Purpose Financial Reporting statements to not‑for‑profit public sector entities—or public-benefit entities

- specific observations about particular sectors.

Section 4.2 details the stakeholder feedback we seek to improve our work.

2.3 Our influence and impact

The work we do at VAGO has the potential to make a real difference to the lives of Victorians. Each of our reports to Parliament, and particularly our recommendations, influence the public sector to improve the way it delivers services and programs. We strive for this influence to lead to a lasting positive impact on the Victorian community.

Some audits have an immediate effect, but sometimes it takes longer for our recommendations to result in meaningful improvement. Some of the ways in which our audits have influenced change this year are listed here.

|

Occupational Violence Against Healthcare Workers |

|

|

May 2015 |

Occupational Violence Against Healthcare Workers tables in Parliament. |

|

September 2017 |

Making emergency departments safer The government announced the roll out of behavioural assessment rooms in emergency departments in 16 Victorian hospitals. This is a better practice example of an environmental design control, highlighted in our report. |

|

Community Health Program |

|

|

June 2018 |

Community Health Program tables in Parliament. |

|

June 2018 |

Community health taskforce announced Two days before our report Community Health Program tabled in Parliament, the government announced a new expert taskforce aimed at identifying ways to strengthen Victoria's community health sector. There was also $292 million allocated to community health care in the 2018–19 Budget. Our audit found that the Department of Health and Human Services was missing an important opportunity to take a more strategic approach to providing primary care services to disadvantaged Victorians through the Community Health Program. We made seven recommendations to the department, focused on reviewing the funding amount and allocation, and improving the program's performance framework. The taskforce will include members from community health services, as well as representatives from the Victorian Healthcare Association, other key organisations and service users. |

|

Management and Oversight of the Caulfield Racecourse Reserve |

|

|

September 2014 |

Management and Oversight of the Caulfield Racecourse Reserve tables, recommending that alternative management arrangements are explored for the Caulfield Racecourse Reserve so that it can better meet the racing and community purposes of the Crown grant. |

|

November 2017 |

Better management of Caulfield Racecourse Parliament passed the Caulfield Racecourse Reserve Act 2017 that established a new governing body to manage the Caulfield Racecourse Reserve. |

|

Prison Capacity Planning |

|

|

November 2012 |

Prison Capacity Planning tables and identifies that a lack of accommodation and increasing number of prisoners contributed to the very high number of prisoners in police cells. |

|

March 2018 |

Increased capacity at police stations Victoria Police conducted a statewide audit to ensure police gaol and court cells were operating at the correct capacity. This resulted in Bendigo Police Station increasing its capacity by more than 30 per cent, and other stations in Geelong, Heidelberg, Mill Park, Moorabbin, Broadmeadows and Sunshine also increasing their capacity. |

|

Emergency Response ICT Systems |

|

|

October 2014 |

Emergency Response ICT Systems tables in Parliament. |

|

August 2017 |

Improving emergency response ICT systems It is announced that police and emergency services in regional Victoria will have access to the state's digital radio network from 2018, eliminating key black spots and increasing security and audio clarity. |

|

Early Childhood Development Services: Access and Quality |

|

|

May 2011 |

Early Childhood Development Services: Access and Quality tables in Parliament. |

|

April 2018 |

A new framework for protecting vulnerable children Parliament passed the Children Legislation Amendment (Information Sharing) Act 2018 which aims to protect vulnerable children by simplifying and improving information sharing arrangements between trusted professional entities, such as maternal and child health, hospitals and schools. The Child Link register will enable services to identify and respond to any risk factors early and collaborate to provide integrated services to a child. The Minister for Families and Children said Child Link responded directly to our 2011 report as well as findings from three other VAGO reports from the past decade. |

|

Maintaining State-Controlled Roadways |

|

|

June 2017 |

Maintaining State-Controlled Roadways tables in Parliament. |

|

October 2017 |

Funding for regional roads The 2017–18 Budget contained $305.5 million for regional road upgrades in 2017–18, and a further $147.9 million in following years. The Public Accounts and Estimates Committee's Report on the 2017–18 Budget Estimates has a direct reference to the funding allocation being linked to our report. The committee also recommended to the Department of Economic Development, Jobs, Transport and Resources, and VicRoads that they develop road maintenance performance measures that fully respond to the recommendations made in our report. |

|

December 2017 |

VicRoads' digital dashboard VicRoads unveiled a new safety tool for the state's 20 most dangerous country roads, with a digital dashboard tracking progress on road upgrades, pothole repairs and reporting on local accidents. It also announced a pilot program on high-speed intersections in the north-east, where new electronic speed signs will reduce the speed limit by 30 km/hr when a car is approaching on the side road. |

|

May 2018 |

Regional Roads Victoria The 2018–19 Budget allocated $941 million to fix hundreds of regional roads. Regional Roads Victoria, a new division of VicRoads, will oversee a $333 million boost to road maintenance. A $100 million Fixing Country Roads fund will pay councils to fix their roads. Our report found that years of declining spending had let country roads become a growing risk to public safety. |

|

Managing Victoria's Planning System for Land Use and Development |

|

|

March 2017 |

Managing Victoria's Planning System for Land Use and Development tables in Parliament. |

|

October 2017 |

Discussion paper released The Department of Environment, Land, Water and Planning's discussion paper on reforming the Victoria Planning Provisions proposed changes that would address recommendations and issues identified in our report, including:

|

|

January 2018 |

Reforms implemented The first tranche of these reforms aim to simplify, clarify and update the planning provisions and definitions, and introduce ongoing monitoring of the provisions. |

|

Regulating Gambling and Liquor |

|

|

February 2017 |

Regulating Gambling and Liquor tables. It highlights that decisions on inspections in regional areas are not based on evidence and are influenced by budget concerns. It also mentions that the Victorian Commission for Gaming and Liquor Regulation was seeking funding to fulfil the expectation to develop regional hubs. |

|

September 2017 |

Bigger Victorian Commission for Gaming and Liquor Regulation presence in regional Victoria The government announced additional funding of $11.3 million over four years for the Victorian Commission for Gaming and Liquor Regulation in the 2017–18 State Budget to increase its presence in regional Victoria. |

3 Our performance: Keeping VAGO accountable

3.1 Reporting on our performance

The products and services we deliver are organised into two Parliamentary output groups in Budget Paper 3. Output Group 1 covers Parliamentary reports and services, and Output Group 2 covers audit reports on financial and performance statements. We have performance measures and targets for quantity, quality, timeliness and cost, across both our audit output groups.

Last year we revised our Budget Paper 3 measures to better reflect our performance, showing whether we are meeting our objectives, not just counting our outputs. These changes are reflected in this year's report.

Figure 3A

Performance against targets for Output Group 1—Parliamentary reports and services

|

Performance measures |

Unit of measure |

Target |

Actual |

Per cent variation |

Result |

|---|---|---|---|---|---|

|

Quantity |

|||||

|

Average cost of Parliamentary reports |

($ thousand) |

499 |

484 |

-3 |

✔ |

|

Quality |

|||||

|

Percentage of performance audit recommendations accepted which are reported as implemented by audited agencies |

(per cent) |

80 |

80 |

0 |

✔ |

|

Overall level of external satisfaction with audit reports and services—Parliamentarians |

(per cent) |

85 |

88 |

4 |

✔ |

|

Timeliness |

|||||

|

Average duration taken to finalise responses to inquiries from Members of Parliament |

(days) |

20 |

15 |

-25 |

✔ |

|

Average duration taken to produce performance audit Parliamentary reports |

(months) |

≤8 |

10.5 |

31 |

□ |

|

Average duration taken to produce financial audit Parliamentary reports after balance date |

(months) |

≤5 |

4.8 |

– |

✔ |

|

Cost |

|||||

|

Total output cost |

($ million) |

15.5 |

15.5 |

0 |

✔ |

Key: ✔ Target achieved or exceeded. ◯ Target not achieved—within 5 per cent variation. □ Target not achieved—exceeds 5 per cent variation.

Quantity

Average cost of Parliamentary reports

|

Every year we prepare a range of performance data for a benchmarking exercise run by the Australasian Council of Auditors-General (ACAG), which is discussed on page 27. Our 2017–18 benchmarking data shows that 44 per cent of all paid hours worked by all VAGO staff were charged to audit work. This proportion increases to 48 per cent when we include the hours spent developing our Annual Plan, which is required to be tabled in Parliament. This is also the average result for all states and territories. |

This year we began reporting on the average cost of our Parliamentary reports, and we met our target for the reports tabled this year. We have increased our target for 2018–19 to cover salary and Consumer Price Index increases, new accounting standards coming into effect in 2018–19 and improved data analytics.

Quality

Performance audit recommendations which are reported as implemented by audited agencies

This is a new performance measure to track whether agencies are implementing the recommendations we've made and they accepted. This year we followed up with the agencies that were the subject of performance audits tabled in 2014–15 and 2015–16. Our surveys show that 80 per cent of the accepted recommendations have been implemented, which is in line with our target.

Overall level of satisfaction

We survey Parliamentarians each year to find out how satisfied they are with our reports and services. This year 88 per cent of Parliamentarians were satisfied or very satisfied with our work. This was down from 93 per cent last year, but is broadly consistent with the 2016 result of 86 per cent.

Timeliness

Responses to inquiries

We receive inquiries from Members of Parliament on a range of issues. For 2017–18, we have a new measure on responding to inquiries from Members of Parliament, and we achieved an average response time of 15 days which exceeds our target of 20 days. This is due to the relatively small number of straightforward inquiries received.

For 2018–19, we have changed the target to be 20 days or less.

Time to produce performance audit reports

This is another new measure for 2017–18. We took longer on average than our target of 8.5 months to produce performance audit reports. We exceeded this target because it took longer than expected to receive data from agencies, and there were technical delays in extracting and cleaning data for analysis. Our focus on audit quality also meant we gathered more audit evidence when we found issues, and we spent more time reviewing draft reports with agencies. For 2018–19, we have increased the target to 9 months to reflect the audits in our Annual Plan 2018–19.

Time to produce financial audit Parliamentary reports after balance date

The time taken to produce financial audit Parliamentary reports is on target.

Cost

We met our cost target this year, spending $15.5 million to deliver our Parliamentary reports and services.

Figure 3B

Performance against targets for Output Group 2—Audit reports on financial and performance statements

|

Performance measures |

Unit of measure |

Target |

Actual |

Per cent variation |

Result |

|---|---|---|---|---|---|

|

Quantity |

|||||

|

Average cost of audit opinions issued on performance statements |

($ thousand) |

5 |

5 |

0 |

✔ |

|

Average cost of audit opinions issued on the financial statements of agencies |

($ thousand) |

50.0 |

48.2 |

-4 |

✔ |

|

Quality |

|||||

|

External/peer reviews finding no material departures from professional and regulatory standards |

(per cent) |

100 |

59 |

-41 |

□ |

|

Proportion of agencies disclosing prior period material errors in financial statements |

(per cent) |

≤5 |

1 |

– |

✔ |

|

Timeliness |

|||||

|

Audit opinions issued within statutory deadlines |

(per cent) |

98 |

98 |

0 |

✔ |

|

Management letters to agencies issued within established time frames |

(per cent) |

90 |

81 |

-10 |

□ |

|

Cost |

|||||

|

Total output cost |

($ million) |

28.4 |

27.6 |

-3 |

✔ |

Key: ✔ Target achieved or exceeded. ◯ Target not achieved—within 5 per cent variation. □ Target not achieved—exceeds 5 per cent variation.

|

ACAG benchmarking data shows that in 2017–18 our audits cost 27 cents for every $1 000 in public sector transactions, down from 30 cents in 2016–17. The average cost for all states and territories was 35 cents. |

Quantity

Cost of audit opinions—performance and financial

This year, for the first time, we have reported on the average cost of the audit opinions issued on the performance and financial statements of agencies. This is a direct measure of our efficiency measure because it relates the number of opinions issued to their cost. We met both these targets in 2017–18. The targets for both measures for 2018–19 have increased to cover salary and Consumer Price Index increases, new accounting standards coming into effect in 2018–19 and improved data analytics.

Quality

External/peer reviews finding no material departures from professional and regulatory standards

This audit quality measure is obtained through post audit quality reviews of a targeted selection of our financial audits in accordance with our three-year rolling review program. The measure is intended to reflect our level of compliance with the requirements of the applicable Australian Auditing Standards, Australian Accounting Standards and Accounting Professional and Ethical Standards.

While our target is 100 per cent compliance, this is rarely achieved in practice, either in the public or the private sector. One reason for this is that we adopt a conservative approach to our assessments.

For example, if a part of our audit work is not documented, our presumption is that the work has not been performed (in the absence of evidence to the contrary). This is the same approach applied by other audit regulators and by most firms in their internal quality review programs.

But more importantly, while we examine a number of key audit areas in each file reviewed, if we find issues in any one area we rate that entire file as having not met standards. In comparison, the Australian Securities and Investments Commission (ASIC) measures just the percentage of key audit areas within inspected files that are noncompliant, as opposed to complete audit files, and reports noncompliance in the range of 19–25 per cent.

We did not meet our target: 41 per cent of our targeted sample of reviewed audit files were found to have material departures. Our findings do not necessarily mean there are material misstatements in the overall financial reports of these entities. Rather, in our view, we did not demonstrate a sufficient basis to form and issue our opinions.

This result is not necessarily representative of the quality of all financial audit engagements conducted, as the selection of audit files was not statistically random. Factors such as prior quality findings, coverage across sectors and our contracted audit service provider firms influenced the file selection process.

We will look to amend the measure and target in 2019–20 to align with the more relevant ASIC measure and industry benchmarks.

Proportion of agencies disclosing prior period material errors in financial statements

This new quality measure is the proportion of agencies disclosing prior period material errors in financial statements. This means that a significant financial statement error was identified, rectified and disclosed in the current-year financial statements by the agency which had not been previously identified by us. We are pleased to have met this new target.

Timeliness

Audit opinions issued within statutory deadlines

This year, we met our target for issuing audit opinions within statutory deadlines.

Management letters issued within established time frames

We did not meet our target for issuing management letters within the established time frame with 81 per cent issued in 2017–18, short of our target of 90 per cent. Last year, government entities and VAGO received very late notice from government of new shortened time lines required for completing audits and tabling annual reports across the public sector. Other audit matters, such as responding in a timely way to our draft management letters, became a secondary priority for agencies in some cases. We also lacked sufficient resources during the compressed time frame to chase down late responders.

Almost all the control gaps identified in the draft letters were still discussed during the audit close-out process with management and audit committees.

Cost

The total cost for this output group was within budget, at $27.6 million.

4 Our audit quality: Improving performance

4.1 Audit quality outside VAGO

We aim to be a leader in public sector auditing, working also to improve the practice of our profession.

Engagement with the Australian Accounting Standards Board

This year, we increased our engagement with the Australian Accounting Standards Board (AASB), with the aim of ensuring that public sector reporting is considered more consciously in their deliberations and decisions.

VAGO staff were on the AASB Insurance Project Advisory Panel and the AASB Fair Value Project Advisory Panel. We also attended and contributed to the AASB Roundtable: Options for replacing Special Purpose Financial Statements.

Engagement with the Australasian Council of Auditors-General

ACAG is an association established by Auditors-General from around Australia, New Zealand and the Pacific nations, to share information about our unique public auditing role. Our participation in ACAG ensures that Victorians benefit from the most up-to-date public auditing approaches and knowledge.

Currently the Auditor-General is the chair of ACAG's Financial Reporting and Accounting Committee. During the year we streamlined ACAG's process for making submissions to accounting standard regulatory bodies.

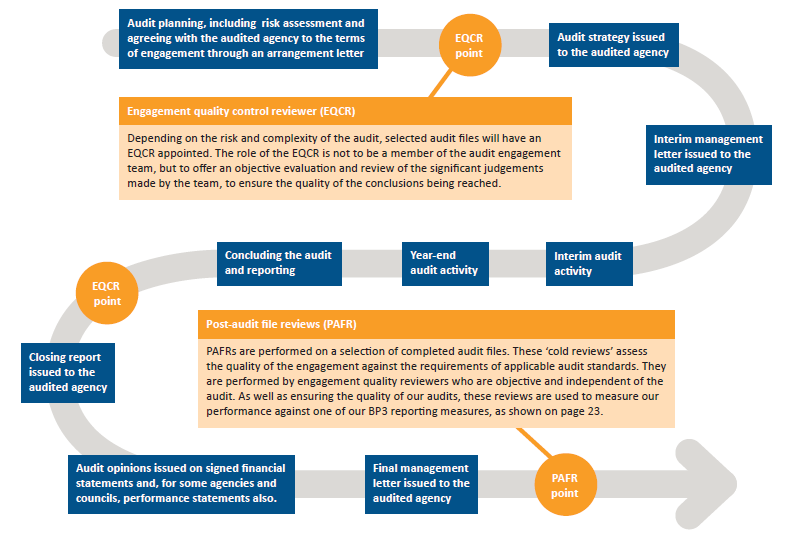

4.2 Audit quality at VAGO

To continue providing value to the Victorian public through our insights we must maintain our high standards. This diagram illustrates our financial audit quality assurance and continuous improvement processes.

Note: An accessible version of this diagram is available at the end of this page.

Some financial audit quality assurance processes do not occur at specific times during an audit, and may not occur for all audits:

Note: An accessible version of this diagram is available at the end of this page.

This diagram illustrates our rigorous framework of similar processes for our performance audits.

Note: An accessible version of this diagram is available at the end of this page.

Results of our recent quality surveys

Parliamentarians survey

We survey Parliamentarians every year. This year's results were positive overall, and broadly similar to our results over the past few years. Parliamentarians assessed the Auditor-General's reports and services as follows:

|

Provide valuable information on public sector performance 93%down from 98% |

Help improve public sector administration 93%up from 89% |

Performance audits address key areas of interest 62%up from 54% |

Performance audits address issues of significance 68%up from 66% |

Audit committee chair survey

We last surveyed the chairs of audit committees in 2014–15. This year, 75 per cent of chairs believed that VAGO adds value by helping public sector entities improve their performance (slightly up from 70 per cent).

A number of chairs made positive comments about improvements such as visibility, access and communication, and a stronger strategic focus. The changes were considered to be 'welcome', 'refreshing' and 'encouraged'.

Ninety per cent of chairs agreed that we are targeting the right audit topics (up from 64 per cent) and 85 per cent thought that we are addressing topics at the right time (up from 54 per cent). Some chairs commented that they are looking forward to seeing the impacts of our data analytics activities.

Chief financial officer survey

We conduct surveys of chief financial officers every two years, in two rounds, based on their organisation's financial year end. This year's results generally show a marked improvement on those from 2015–16.

|

Professional 98%up from 93% |

Professional skills and knowledge 96%up from 91% |

Understanding of the organisation 90%up from 84% |

Effective 89%up from 80% |

Despite the improved results, there were some concerns about staff continuity, inadequate staffing, not enough time being allocated for audits, audit fees and excessive requests for information.

Chief financial officers valued the assurance provided by our financial statement audits (94 per cent, up from 91 per cent) and valued our recommendations for improvements (90 per cent, up from 87 per cent).

Performance audit surveys

Every year we survey the agencies involved in our performance audits about our process, reporting and value.

|

Process |

Reporting |

Value |

||

|---|---|---|---|---|

|

Positives: the quality of the audit process, the professionalism and engagement of audit teams, sufficient opportunity to comment on issues prior to receiving a draft report. For improvement: continuity of audit staff. |

Positives: there were adequate opportunities to make comments, tabled reports were accurate and clearly communicated the issues. For improvement: the relevance and practicality of our recommendations, the timing allowed to respond to report drafts. |

Positives: audits were generally focused on the right areas. For improvement: the depth and scope of audit recommendations, being clearer about the risk or issue driving the audit, providing best practice standards and benchmarks. |

4.3 Improving our performance

Data analytics

This year, we have significantly expanded our data analytics capability. We developed a strategy for integrating data analytics into our audit work to support traditional auditing methods. To help public sector agencies see the power of the data that they hold, we have begun creating and providing dashboards to agencies.

One advantage of our dashboards is the ability to add data year on year and build up a complete picture of how a program or agency is performing. This will allow us, and agencies, to return to the data we've collated over time which will reveal long-term trends and better inform their planning and decision making.

The first phase of our strategy focuses on our data analytics staff building dashboards and other analyses and helping source the most appropriate datasets for our performance audits. Staff in our performance audit areas are being trained in how to use data analytics tools, which increases their skills and lifts the capability of the whole organisation.

We have begun accessing datasets from non-government sources to complement our own work, and have been piloting the use of basic text mining tools to assist with annual planning.

For our financial audits, we are streamlining the collection of data and building standardised dashboards that our financial audit teams can use and build on each year.

In the future, our staff will be skilled enough to build their own dashboards. We will expand our use of external datasets and introduce predictive modelling methods. We will also progress to using more sophisticated text mining tools for analysing unstructured data.

Financial audit

During the year, we developed a multi-year strategy to embed data analytics into our financial audit practices. We will be applying data analytic tools and techniques across many financial audits in the future, which will improve our audit quality and efficiency. We have been working to streamline the collection of financial data. We use this data to improve our understanding of our financial audit clients' business risks, to assess their internal controls, and to improve the focus of our audit testing.

Although we are still early in our journey, we have engaged with most of the entities identified for phase 1 of the strategy. We've gathered expenditure and payroll data from several of our larger audit clients and have begun building a customised analytics solution that will standardise their data into a uniform format for analysis. This will allow us to:

- identify key audit risks and tailor our approaches to address them

- effectively sample and select data

- gain better insights and provide better business intelligence back to our financial audit clients.

Our first four dashboards were published in November 2017, along with our report Results of 2016–17 Audits: Public Hospitals. These dashboards are interactive visualisation tools that summarise the financial statement data of all Victorian hospitals. They allow stakeholders and the general public to refine and compare a huge range of financial information.

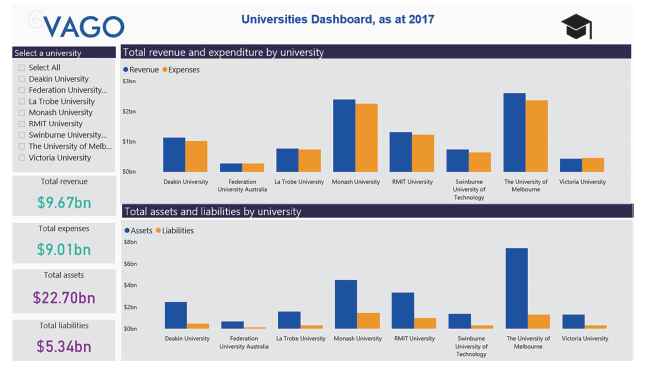

In May 2018, we published similar dashboards to accompany our reports on Technical and Further Education (TAFE) institutes and universities.

These are examples of ways we are increasing the accessibility of our work through new interactive channels. Over time, we will add new content and insights, and will improve the usability of our dashboards by seeking feedback from our stakeholders.

Performance audit

We have been working to create a strategic three-year plan to successfully execute data-driven audits—an innovative way of ensuring our audits are based on persuasive, objective evidence. Some of the key steps we are taking to bring together our data analytics and performance audit capabilities include:

- collaborating up to six months before an audit begins, to kick-start the audit's data strategy

- planning together to more effectively use data analytics

- co-sourcing rather than outsourcing when using external analytics services to ensure the skills and knowledge are transferred to VAGO.

Fifteen performance audit projects have been supported by data analytics in various ways, from assuring the quality of the data used for analytic work to creating interactive dashboards.

One dashboard that has been particularly valuable was created as part of our audit of Victorian Public Hospital Operating Theatre Efficiency. For this audit, we compiled a dataset using data from 23 health services. We created a dashboard to analyse health system performance and benchmark data in multiple ways not previously done in Victoria. The dashboard can be used to analyse the efficiency of operating theatres within and between health services and hospitals.

Creating dashboards and datasets not previously compiled and providing these back to agencies is an area of future growth for us. This will be a key way to help agencies make the most of their own information, and to achieve our strategic objective of being more influential by providing our clients with new insights they can use.

Audit mandate and process

Performance audit

This year, we tabled our first audit using our new follow-the-dollar powers, Safety and Cost Effectiveness of Private Prisons. These powers allow us to audit private and non-government organisations that are contracted to provide public services. This audit published our analysis of a large amount of data about how private prisons operate that was not previously available to the public. We found that private prisons are cheaper to run than publicly operated prisons, and that they largely meet their contract service and performance requirements.

We established a new Performance Audit Practice Governance Committee this year to ensure that performance audit practices are up to date, streamlined and consistent. The committee, made up of staff from across VAGO, aims to implement improvements and changes arising from audit debriefs, stakeholder feedback and internal staff suggestions. It considers technology tools, policy, guidance and manuals, training materials, templates and practice statements.

We have improved the quality of our planning by adopting a more risk-based approach. We have improved our understanding of agencies and audit subject matter to identify any risks and better tailor our audits. This approach is reflected in our updated methodology and our recent training.

Part of improving our understanding of agencies is working with them earlier in the audit process. On two recent audits, Effectively Planning for Population Growth and Community Health Program, we brought agencies together to discuss our recommendations jointly and earlier than usual. This has resulted in recommendations that are more useful and practical for agencies.

This has also led to better working relationships with departments. In our recent surveys, agencies rated the quality of our audit process highly, particularly the professionalism, skills and knowledge of our staff, and their ability to communicate effectively.

Financial audit

It has been 12 months since the new standard, ASA 701 Communicating Key Audit Matters in the Independent Auditor's Report, became effective. It requires us to include a description of key audit matters in our reports. These are matters that we determine to be the most significant. We must include a brief description, an explanation of why we consider them to be key audit matters and details of what we did to address them.

We have voluntarily adopted this new standard as we believe it will enhance the value of our auditor's report by providing greater transparency and insight to our audit process. In the Auditor-General's Report on the Annual Financial Report of the State of Victoria: 2016–17, tabled in November 2017, we disclosed key audit matters for the first time. We continued a staged implementation of this standard for other entities during 2017–18.

We have been working with entities to help them adopt streamlined reporting. The purpose of streamlined reporting is to make reports easier to understand. These reports still comply with all relevant standards and legislation, but remove any information that is immaterial. They are easier to read and more user‑friendly than traditional financial reports. Both the local government and university sectors have adopted streamlined reporting, with positive results.

We dedicated sustained effort at all levels to working with audit clients and other key stakeholders to improve the level of service we provide, including in our written communications. For example, we changed the look, feel and structure of key documents provided to stakeholders like audit committees to help them to focus on the most important insights we have to offer.

The below tables provide an accessible version of the images in Section 4.2.

To continue providing value to the Victorian public through our insights we must maintain our high standards. This diagram illustrates our financial audit quality assurance and continuous improvement processes.

|

|

Audit planning, including risk assessment and agreeing with the audited agency to the terms of engagement through an arrangement letter |

|

● EQCR point |

|

|

Audit strategy issued to the audited agency |

|

|

Interim management letter issued to the audited agency |

|

|

Interim audit activity |

|

|

Year-end audit activity |

|

|

Concluding the audit and reporting |

|

|

● EQCR point |

|

|

Closing report issued to the audited agency |

|

|

Audit opinions issued on signed financial statements and, for some agencies and councils, performance statements also. |

|

|

Final management letter issued to the audited agency |

|

|

● PAFR point |

Note:

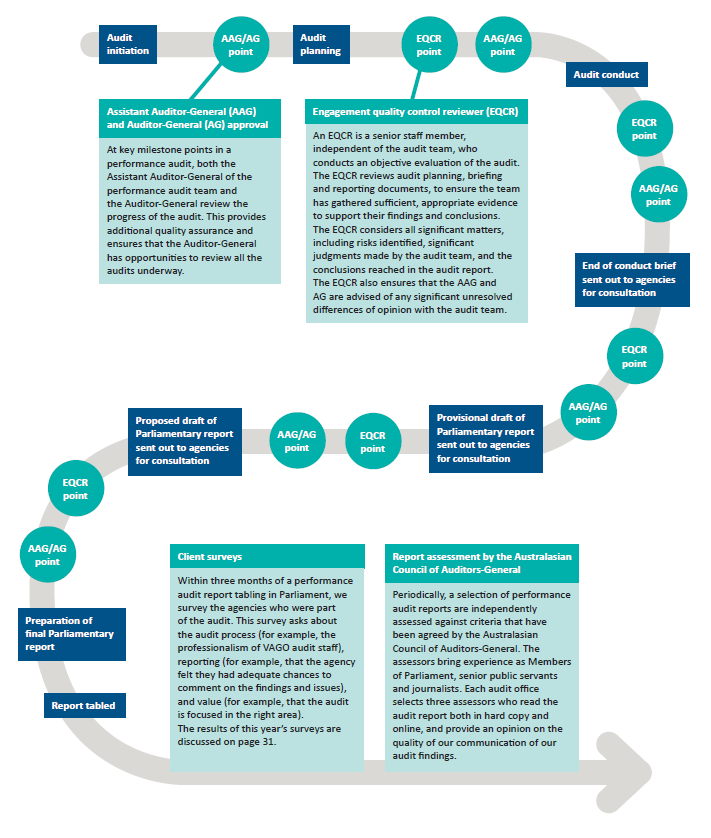

Engagement quality control reviewer (EQCR)—Depending on the risk and complexity of the audit, selected audit files will have an EQCR appointed. The role of the EQCR is not to be a member of the audit engagement team, but to offer an objective evaluation and review of the significant judgements made by the team, to ensure the quality of the conclusions being reached.

Post-audit file reviews (PAFR)—PAFRs are performed on a selection of completed audit files. These 'cold reviews' assess the quality of the engagement against the requirements of applicable audit standards. They are performed by engagement quality reviewers who are objective and independent of the audit. As well as ensuring the quality of our audits, these reviews are used to measure our performance against one of our BP3 reporting measures, as shown on page 23.

Some financial audit quality assurance processes do not occur at specific times during an audit, and may not occur for all audits:

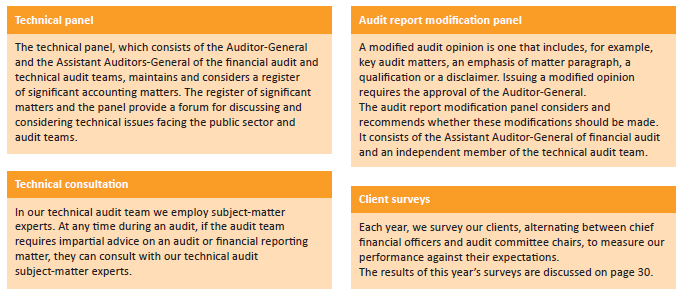

|

Technical panel |

Audit report modification panel |

|---|---|

|

The technical panel, which consists of the Auditor-General and the Assistant Auditors-General of the financial audit and technical audit teams, maintains and considers a register of significant accounting matters. The register of significant matters and the panel provide a forum for discussing and considering technical issues facing the public sector and audit teams. |

A modified audit opinion is one that includes, for example, key audit matters, an emphasis of matter paragraph, a qualification or a disclaimer. Issuing a modified opinion requires the approval of the Auditor-General. The audit report modification panel considers and recommends whether these modifications should be made. It consists of the Assistant Auditor-General of financial audit and an independent member of the technical audit team. |

|

Technical consultation |

Client surveys |

|

In our technical audit team we employ subject-matter experts. At any time during an audit, if the audit team requires impartial advice on an audit or financial reporting matter, they can consult with our technical audit subject-matter experts. |

Each year, we survey our clients, alternating between chief financial officers and audit committee chairs, to measure our performance against their expectations. The results of this year’s surveys are discussed on page 30. |

This diagram illustrates our rigorous framework of similar processes for our performance audits.

|

|

Audit initiation |

|

●AAG/AG point |

|

|

Audit planning |

|

|

●EQCR point |

|

|

●AAG/AG point |

|

|

Audit conduct |

|

|

●EQCR point |

|

|

●AAG/AG point |

|

|

End of conduct brief sent out to agencies for consultation |

|

|

●EQCR point |

|

|

●AAG/AG point |

|

|

Provisional draft of Parliamentary report sent out to agencies for consultation |

|

|

●EQCR point |

|

|

●AAG/AG point |

|

|

Proposed draft of Parliamentary report sent out to agencies for consultation |

|

|

●EQCR point |

|

|

●AAG/AG point |

|

|

Preparation of final Parliamentary report |

|

|

Report tabled |

5 Our people: Investing in the future

This year, we have focused on modernising our work and building a new culture that supports our strategic objectives, following a time of significant structural and physical change.

One of our new strategic objectives is to invest in our people. We want to enable high performance by providing a supportive culture, encouraging professional development and collaborating. We have invested heavily in the core skills of our people, most notably focusing on our managers.

This year, we launched our new values, developed through a staff-led process that empowered our people to shape what values we should embody to meet our vision. This is a critical first step towards changing our culture for the long term.

In addition, we have enabled our staff to work more efficiently by reviewing several systems and processes, including our human resources practices.

We have also instituted a new streamlined governance structure to strengthen and provide clarity on the way we monitor and improve our organisational strategy and performance. We have established a Strategic Management Group, which is responsible for setting and monitoring the implementation of VAGO's strategic plan, and an Operational Management Group, which is responsible for overseeing our operations and our business plans.

5.1 Our staff

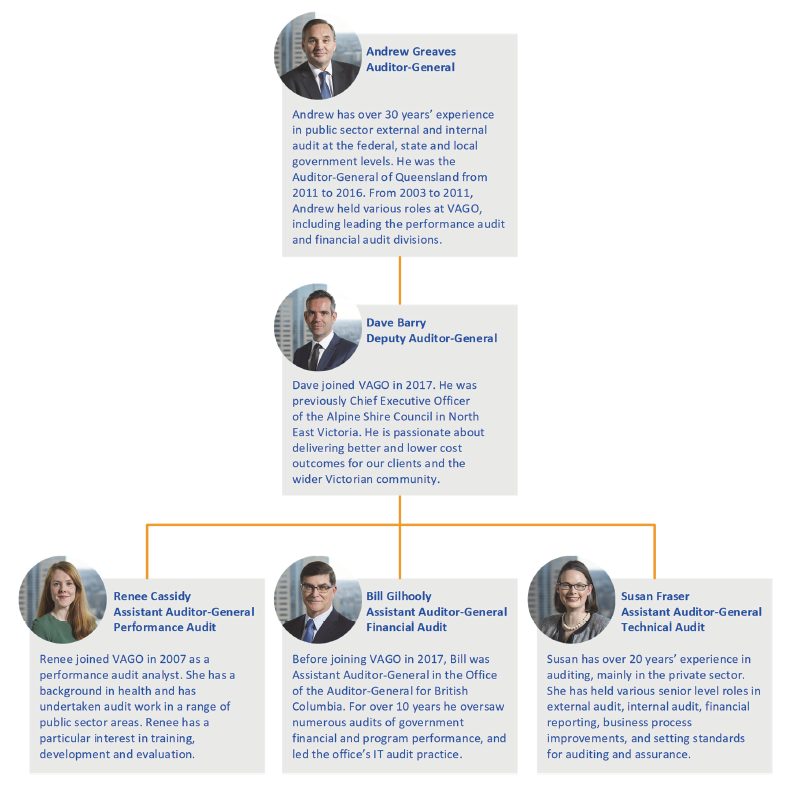

Figure 5A

Organisational structure

Note: An accessible version of this diagram is available at the end of this page.

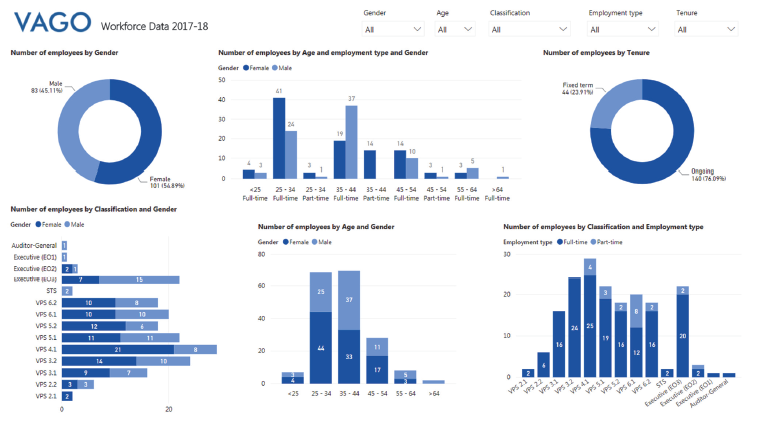

A profile of all VAGO employees is included in Appendix A. This year for the first time we have also created an online dashboard which allows the public to filter our workforce data. The dashboard, pictured below, is available at www.audit.vic.gov.au/report/annual-report-2017–18.

The dashboard shows our employees by age, seniority, whether they are part‑time or full-time, on fixed-term or ongoing contracts, and by gender. VAGO employed 101 women in 2017–18, making up 55 per cent of our workforce. However, women made up 90 per cent of our part-time workers and 76 per cent of our fixed-term employees. Our gender pay gap is 14 per cent or around $16 000.

In 2018–19 we are developing a Diversity Plan to help us become a more respectful, diverse and equitable organisation, including focusing on supporting women at work.

5.2 Human resources improvements

Over the past year, we have reviewed and modernised many of our human resources processes and considered every stage of an employee's time at VAGO.

Recruitment

To make our recruitment more effective, we have simplified our job advertisements. Using plain English, we are providing better information about what working for VAGO is like, including an infographic outlining the benefits of working at VAGO.

We are advertising in a wider range of places, including through professional associations, like Chartered Accountants Australia & New Zealand and CPA Australia, and overseas in Hong Kong, New Zealand and the United Kingdom. We are also using technology to better target our advertising.

To ensure we get the right mix of people, we have introduced psychometric evaluations, video interviewing and online competency testing. Potential staff are assessed on their ability to write reports and use specialised software.

We are also trialling an 'order of merit' process for the financial audit positions and are now recruiting financial auditors just twice a year. All applicants are ranked holistically and we call the next most suitable applicant when a vacancy arises. This new process, in addition to our updated graduate program, will go some way to addressing challenges in filling our financial audit vacancies.

All our internal recruitment processes are moving online, including candidate selection and sending letters offering jobs. The whole process will be conducted without any documentation being printed.

Induction

Once recruited, new VAGO staff now enjoy a comprehensive and effective induction process. In the past, our inductions have been inconsistent across different business units. New staff were sometimes left with gaps in their knowledge and uncertainty about whom to approach with questions.

Our new process clarifies the roles of the different business units and identifies the training needs of each new starter. Team managers now take a more active role in induction, guided by a 100-day checklist to ensure everything new employees need to know is covered.

New employees also get ongoing support from an allocated buddy who helps them settle into VAGO and provides an alternative source of advice from the employee's manager. We also have a comprehensive new starters' intranet page.

This revised induction process is still new but early feedback from across VAGO has been very positive, with staff finding recent inductions very effective.

Learning and development

|

ACAG benchmarking data shows that in 2017–18:

We continually balance the need to ensure the skills of our staff are kept up to date, while ensuring that their efforts create valuable audit outcomes. |

This year, there has been a great investment in learning and development, with an emphasis on behavioural skills and technical training.

One of our skills initiatives was the mandatory Manager Foundations program— five modules to equip managers with effective leadership skills. This program was developed in response to staff surveys and in consultation with senior executives. For other staff, we delivered courses in response to the needs identified through performance development plans. We also continue to support individual developmental needs by providing external coaching.

Technical audit training has continued to be a focus, ensuring all our staff are up to date with the latest regulatory standards as well as our audit methodology. We have run technical courses on data analytics tools, the impact of changes to technical accounting standards, and VAGO's audit methodology.

During the year, our staff have been keynote speakers and panel members at a variety of events, such as the Impact 2018 performance audit conference in Sydney, hosted by ACAG, and the Australian Government Data Summit held in Canberra. The staff who attended external events share their knowledge across the organisation though written articles and 'lunch 'n' learn' sessions. We are also building our internal capacity by offering an in-house 'Train the Trainer' course so that we can leverage and share information in formal and informal ways.

5.3 Developing our new values

VAGO has been going through a period of significant change and transformation, not only in our structure but also in the way we work. Our previous set of internal values no longer reflected the type of workplace VAGO was becoming, or the priorities of our staff. Choosing new values was an opportunity for staff to have their say, and make a commitment to the way we will work together to achieve our objectives.

We empowered our staff to lead the change and take control of setting the organisational values, supported by independent consultant facilitators. Firstly, focus groups brainstormed various values, discussed what they meant and which were most important. Then the Values Consultative Committee was established to refine these ideas and draft a new set of values. The committee was made up of staff from all levels and areas of VAGO.

There was an official launch of the new values on 15 May and there have been several subsequent events to support all VAGO staff to embed the values in our everyday work. These events have been led by interested staff, with support from the human resources team and the leadership group.

Activities to embed the values will continue and we will review our progress through the People Matter Survey next year.

Below is an accessible version of Figure 5A—Organisational structure.

|

Andrew Greaves |

Andrew has over 30 years' experience in public sector external and internal audit at the federal, state and local government levels. He was the Auditor-General of Queensland from 2011 to 2016. From 2003 to 2011, Andrew held various roles at VAGO, including leading the performance audit and financial audit divisions. |

|

Dave Barry |

Dave joined VAGO in 2017. He was previously Chief Executive Officer of the Alpine Shire Council in North East Victoria. He is passionate about delivering better and lower cost outcomes for our clients and the wider Victorian community. |

|

Renee Cassidy |

Renee joined VAGO in 2007 as a performance audit analyst. She has a background in health and has undertaken audit work in a range of public sector areas. Renee has a particular interest in training, development and evaluation. |

|

Bill Gilhooly |

Before joining VAGO in 2017, Bill was Assistant Auditor-General in the Office of the Auditor-General for British Columbia. For over 10 years he oversaw numerous audits of government financial and program performance, and led the office's IT audit practice. |

|

Susan Fraser |

Susan has over 20 years' experience in auditing, mainly in the private sector. She has held various senior level roles in external audit, internal audit, financial reporting, business process improvements, and setting standards for auditing and assurance. |

6 Our internal operations: Leading the public sector

|

Benchmarking by ACAG in 2016–17 showed that we spent 24 per cent of our total office expenditure on corporate support functions, which was around 8 per cent more than the state and territory average. This was a strong driver for reducing our corporate costs, so that Victorians get better value for money from our work. Our efforts to reduce costs resulted in our corporate support spend decreasing significantly to just 17 per cent this year, now just 4 per cent behind this year's state and territory average. |

One of our new strategic objectives is to lead the public sector by example, and a key part of that is making VAGO an exemplary audit office. We are in the process of modernising several aspects of our work.

There are many processes we have used for a long time without critically assessing whether they are the best way of doing things. To become more efficient we have reviewed our practices and are improving our systems to make things easier for auditors and our other staff. We are eliminating unnecessary processes and purchases.

Our core work is auditing, but we have always spent a large portion of our time and effort on supporting corporate activities. We are trying to refocus our resources on audit work and creating value through our activities.

We are in transition and are striving to be innovative—this is one of our new values. We hope to become an organisation that can truly challenge the status quo and deliver a better service by doing things differently.

This year, we have taken many steps toward making VAGO a modern and responsive audit office. This section details some of our improvement projects.

6.1 Key developments

This year, we have commenced reviewing and improving our internal controls framework across the 'three lines of defence'. This has involved establishing our new governance forums, revising our risk management approach, and updating our fraud and corruption policy framework in line with the findings of our performance audit Fraud and Corruption Control, tabled in March 2018.

|

Cost savings Several of our improvement projects this year have been aimed at reducing our costs, including:

Through these and other projects VAGO has saved over $183 000 this year, and redirected that money to performing audit work improving our technology and increasing our analytics capability. |

Throughout the year, we have implemented a number of information and communications technology (ICT) changes:

- We have begun 24/7 monitoring of our network and security.

- Staff received new Surface Book 2 laptops.

- We implemented mandatory multi-factor authentication for all staff.

- We updated the resilience of our network.

- We started migrating core services to the Cloud—we plan to have no server infrastructure on our premises by the end of 2019.

VAGO takes information and data security very seriously. We manage the risks associated with holding confidential information, and we accept the responsibilities we have to individuals to protect privacy, in accordance with the Privacy and Data Protection Act 2014. In 2017–18, we improved our security arrangements across the information, ICT, personnel and physical domains to ensure that we exceed the Act's minimum requirements and protect the information we hold.

By applying our data analytics capability to our own work, we are developing a business intelligence dashboard that gives us simple and timely access to performance and management information. The dashboard will readily show, in real time, how efficiently and effectively we are using our resources and over time will steadily be built up to cover a range of productivity and performance measures. We believe that this better business intelligence will drive better decision making.

|

ACAG benchmarking data shows that our financial audit staff spend 67 per cent of their available time directly on financial audits and our performance audit staff spend 70 per cent of their available time directly on performance audits. |

This year, we eliminated unnecessary internal red tape. We streamlined and automated some core administrative business processes to save money and empower staff who previously had to go through needless approval processes. This project was partly driven by staff survey results which highlighted too much bureaucracy and red tape as an issue. Part of the project looked at staff travel, including car hire and taxi use. The other part reviewed our process for publishing financial audit opinions and was conducted in collaboration with our records management team. Information management is an area where VAGO is providing an example to the public sector. Two of our projects were recognised this year at the prestigious Rupert Hamer Records Management Awards.

Figure 6A

From Melbourne to Mornington: The end of the paper trail and the start of the digital journey

|

Every year we issue a financial audit opinion letter to six individuals for each of the 550 public sector entities that we audit. This meant sending 3 300 separate letters by post, a process which took over 100 hours and used approximately 233 000 pieces of A4 paper. If laid end to end, these would reach from our office in the CBD to Mornington. We digitised this whole process, which produced a number of benefits:

This project also challenged the perception, often held by other public sector agencies, that auditors want to see paper copies of documents. This was a pilot project, and we have continued digitising our other paper-based processes. |

Figure 6B

The digital destination: Paving the way using VERS3

|

In 2015, the Public Record Office Victoria (PROV) released the Victorian Electronic Records Standard version 3 (VERS3). However, the process of creating and transferring a record as a VERS3 encapsulated object (VEO) had never been tested and executed by an agency. We undertook a project to transfer our key permanent records, our audit reports, to PROV as VEOs. This was the first transfer of its kind in Victoria. We worked collaboratively with PROV to test processes, tools and guidance material. The project was very successful, with the transfer being executed ahead of time and the VEO creation and transfer meeting all quality standards. The project had several benefits:

|

7 Our financial management

7.1 Current year financial review

Our primary fiscal objective is to minimise our costs to Parliament and our public sector fee-paying clients, while maintaining the effectiveness and quality of our services and their delivery.

Our financial performance and position are, as a rule, predictable year on year, as the nature of our business and its scale does not change substantially. Following the prior year's organisational transformation, this year's results reflect the embedding of our changed practices.

Figure 7A

Financial summary 2017–18 and previous four years

|

Item |

2017–18 |

2016–17 |

2015–16 |

2014–15 |

2013–14 |

Movement |

Change |

|---|---|---|---|---|---|---|---|

|

Total revenue |

45 276 |

43 763 |

41 384 |

39 698 |

38 954 |

1 513 |

3 |

|

Total expenses |

43 263 |

46 907 |

41 301 |

39 161 |

38 994 |

(3 644) |

-8 |

|

Surplus/(deficit) |

2 013 |

(3 144) |

83 |

537 |

(40) |

5 157 |

-164 |

|

Financial assets |

19 955 |

25 619 |

16 962 |

15 019 |

13 965 |

(5 664) |

-22 |

|

Non-financial assets |

5 968 |

6 463 |

1 386 |

1 803 |

2 326 |

(495) |

-8 |

|

Total assets |

25 923 |

32 082 |

18 348 |

16 822 |

16 291 |

(6 159) |

-19 |

|

Total liabilities |

18 360 |

26 532 |

9 654 |

8 211 |

8 217 |

(8 172) |

-31 |

|

Net assets |

7 563 |

5 550 |

8 694 |

8 611 |

8 074 |

2 013 |

36 |

Surplus/deficit

We aim to break even over the medium term, understanding that in some years we need to invest in new technology and update our audit methodologies. This will lead to deficits in those years, which we fund from our working capital reserves. In other years, we will make small surpluses, which will replenish our reserves.

This year we made a surplus to partly offset last year's deficit, indicating that we are operating in a fiscally responsible and sustainable manner.

Figure 7B

Surplus/deficit as percentage of total revenue

|

2017–18 |

2016–17 |

2015–16 |

2014–15 |

2013–14 |

Five-year |

|---|---|---|---|---|---|

|

4.4% |

-7.2% |

0.2% |

1.4% |

-0.1% |

-0.3% |

This year's surplus was due largely to the realisation of cost-savings across all expense categories.

Net assets

We remain in a strong financial position, with an improvement in our financial position driven by the operating surplus. Significantly, our working capital is sufficient to fund our operations over the forward estimates period.

Figure 7C

Net assets as a percentage of total assets

|

2017–18 |

2016–17 |

2015–16 |

2014–15 |

2013–14 |

Five-year |

|---|---|---|---|---|---|

|

29.2% |

17.3% |

47.4% |

51.2% |

49.6% |

35.2% |

The future

We budget for a small surplus in 2018–19, as we continue to implement our organisational transformation activities.

7.2 Financial performance

Operating statement

Our net financial result for the year was a surplus of $2 013 000, compared with a deficit of $3 144 000 in 2016–17.

Figure 7D

Revenues and expenses

|

Item |

2017–18 |

2016–17 |